We are beginning to see some notable changes with this issue of the St. Louis Fed’s Monetary Trends. First I’d like to point out from page 6 that consumer credit is still largely negative on a year over year basis. That’s saying something, as a year ago it was dramatically down from prior levels. The same goes for Nonfinancial Commercial Paper which is trending upwards from its collapse, but is still down in the 30% year over year range.

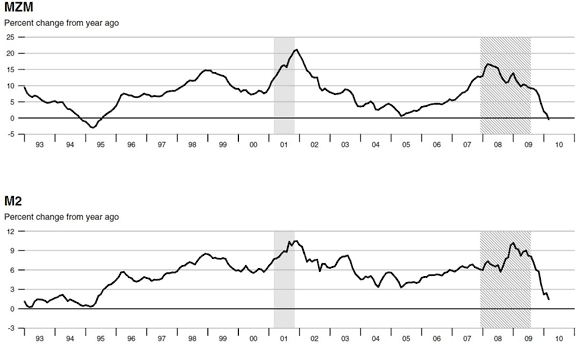

Noteworthy from my perspective is that MZM, the largest measure of money the Fed currently releases, is now negative on a year over year basis, M2 is not far behind and is barely positive:

The spike induced in the money supply was historic, that support is no longer being applied at the same rate. Interest rates hit zero and are still zero, yet the supply of money (as measured by the Fed) is now shrinking from the amount one year ago. As large quantities of money (debt) is forced into the system, the velocity of that money naturally falls. As injections slow, velocity should rise. However, when the system is left in a debt saturated state, velocity cannot return to previous levels as more money is required to service the now larger quantity of debt that each cycle has produced.

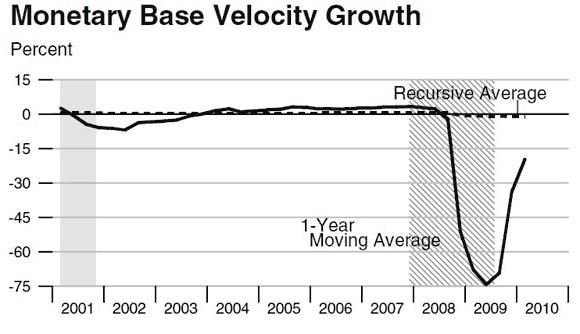

When we look at Base Money Velocity Growth, we see that it is coming up from the cliff dive experienced with massive money injections, yet it is still largely negative year over year.

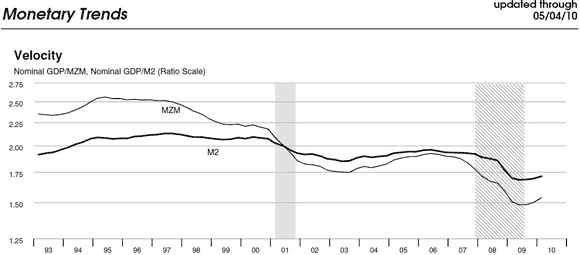

Both MZM and M2 velocities have turned barely upwards but are at extreme low readings. Note that velocity is not responding the way one would expect with the monetary aggregates declining. Also note that with each cycle it attempts to move back higher, but produces a lower low and a lower high.

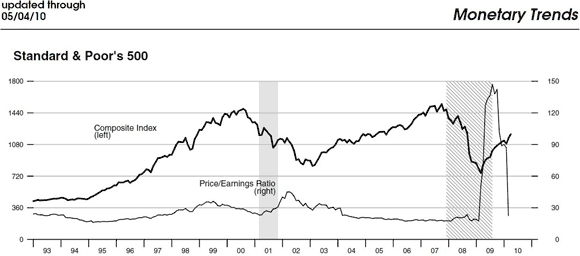

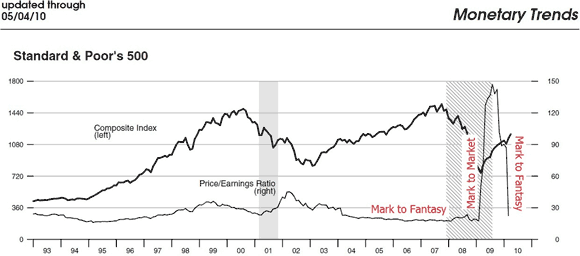

The S&P Price to Earnings ratio (based upon trailing earnings, the only earnings that matter as everything else is just a guess), have fallen dramatically as earnings have come back up.

They are still at the historic upper end, that being in the twenties, an area normally associated with tops. So, what happened to this chart, why the rocket shot in P/E and now sudden drop?

Earnings collapsed as financial firms were forced to mark their earnings to market, a price for which they could actually sell their “assets.” That wiped out earnings and left the price sky high in relation to those reality based asset prices. Then they pressured Congress, who pressured FASB to reinstate mark to fantasy. “Earnings” came back up as “assets” once again were valued to their own models, bonuses flow, and Price to Earnings came back down.

FANTASY. Accounting fraud coupled with massive government stimulus, that’s all, nothing is fixed.

So, what about the future? Most of those “assets” that are marked to fantasy are debt based instruments. Income is required to service debt. Ponzi schemes ALWAYS break down when the cash flow is no longer sufficient to service the Ponzi growth. America and her largest financial institutions are insolvent. Mark their “assets” back to what the market and incomes can bear and the result will be the same.

Leave a Reply