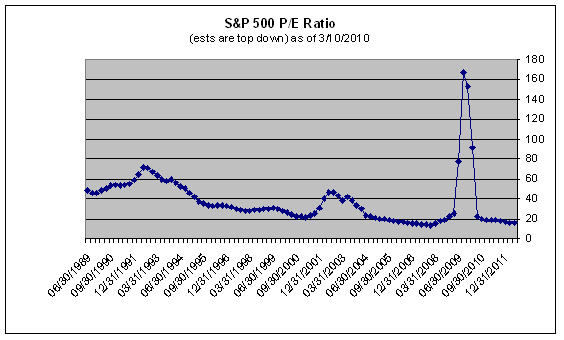

This is an update to a post on PE ratios. Last year we had for the first time the earnings of the S&P go negative, which drove the PE ratio to absurd levels, as you can see from this chart by Hans Wagner.

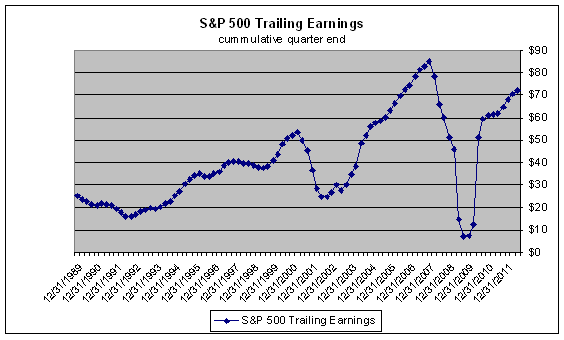

As we got the final results in from Q4, we have an overall $51.15 per share for the trailing twelve months, putting the current PE at 23. Future projected earnings across the S&P are:

2010: $75 (BofA) and $76-79 (GS)

2011: $85 (BofA) and $90-95 (GS)

2012: $90 (BofA)

Hans discusses past behavior after a recession, and finds that PEs tend to drift down towards 15 as an economy normalizes. If the PE drops into a normal range of 15, as is shown in his first chart, the 2010 projections would target a year-end S&P at 1200, essentially flat for the rest of the year. He sees the trailing EPS rising to just under $60 after Q1, putting a fair value at Sp1200 if we drift down to a 20 PE, but at a bullish 1350 if we remain around 22-23 PE. Given the drift downward of PE from 23 to 20 and then to 15, he projects a range of 900-1250 through the end of the year. This is not far off my January predictions for a rolling market in 2010, not a break below the Mar09 lows nor a rise to new highs.

Barron’s roundtable on this topic in January focused on the economy. It is well worth the read. The closest analogy discussed is Japan, which bodes poorly for the US. The biggest wildcard is whether we recover in the 4-4.5% GDP range, which should enable the Fed to completely end QE and other stimulative measures. Overall the group was gloomy, pinning their minimal optimism on a liquidity-driven market, and expecting the Fed to continue easy credit. At best their S&P range was 1250-1300 at the end of the year.

The NYT also ran a piece on fair value, and expressed the concern that interest rates are rising, putting a damper on the Fed’s easy money policy. More on that topic in this post: Did ObamaCare Spook the Bond Market? The WSJ weighed in on this topic, suggesting first that a massive increase incorporate debt offerings may have pushed the swap rates with 10-yr Treasuries to negative, and second that funds were caught off guard by the negative rates, and dumped Treasuries, making last week’s debt offerings unusually weak. In other words, the weakness might be a blip.

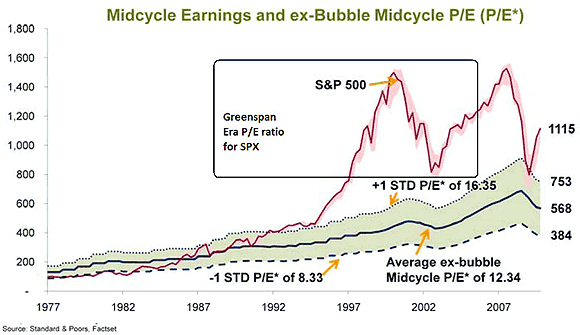

Barry Ritzholz asks rhetorically, when was the market last under-valued? He is of the camp that since the Greenspan Put after the 1987 crash, stocks have floated at much higher PE levels than in the past. We dipped briefly back into an historical level last year at the Ma09 low, then have popped back up to bubblicious levels again.

Barry may not realize he is making the opposite point of his post: that as long as the Fed’s extraordinary easy credit continues, stocks will float at ahistorical PE levels, rather than drift down. Thus the bond market holds the key to stocks: if long rates drift up despite the Fed’s best efforts to hold them do this is the warning signal that the excessive easing is losing its grip.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply