Many governments of advanced economies are struggling with large deficits and increasing debt. When the crisis is over some of these countries will find themselves with levels of government debt that we have not seen since the end of World War II and, in many cases, close to double the amount before the crisis started. Some European countries, Greece in particular, but also Portugal, Spain or Ireland are under enormous pressure to control their deficits as they see their interest rate spreads grow.

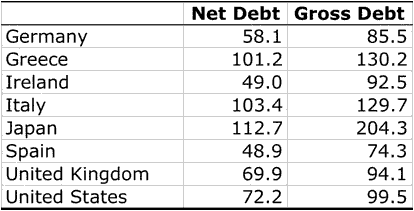

Who is in more trouble? Why is it that some of the countries that were used as models of fiscal discipline (Ireland or Spain) are now under attack? A quick look at government debt (as a % of GDP) reveals very high levels for may advanced economies. The first question is which measure of debt to use: gross or net. Gross debt is simply the stock of outstanding government debt. Net debt is the difference between gross debt and the financial assets that government holds (Note: the definition of net debt is not identical for all countries. Not all governments include the same type of financial assets).

The table below shows gross and debt levels for a group of advanced economies (this is a forecast for 2011 done by the OECD).

Government Debt as % of GDO in 2011

Source: OECD Economic Outlook

It is clear that the difference between gross and net debt is very large for some countries. While Japan looks like an outlier in terms of gross debt, it is close to Italy and Greece when it comes to net debt. In principle, net debt is a more appropriate measure of government indebtedness. If governments have a significant amount of assets, they need to be considered when thinking about the solvency of their accounts. In some cases the government (at large) holds some of its own debt in pension funds for public employees or the social security fund (this is why in the US the most common measure of government debt is “debt held by the public” which is a measure very similar to the concept of net debt), this debt is not a liability for the government.

There are, however, some concerns with the concept of net debt. In addition to some measurement question (which assets to include, at which value), the government needs to refinance all its gross debt and not only the net part, so in terms of flows, it is the gross debt that matters. Also, while it makes sense to exclude government debt held by the government, some of this debt is part of a fund that covers future pension liabilities that are unaccounted for in the budget. And here is where the assessment of government solvency gets more difficult: what you really want to do is not just to look at government debt but also at future revenues and liabilities.

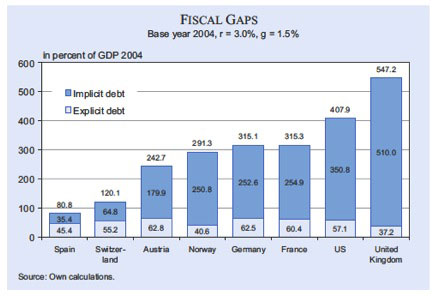

Doing these calculations requires many assumption about the future so there is always uncertainty about these assessments. Below is a chart from an article by C.Hagist, Stefan Moog, Bernd Raffelhuschen and Johannes Vatter that calculates what they call “implicit government debt” as the net present value of future liabilities minus future revenues.

The numbers are dramatic for some countries and there are are large difference between some of them. While Spain or Switzerland have levels of implicit debt that are “low”, the US or the UK have levels of implicit debt that make the total debt four or five times higher than the current level of debt (total indebtedness of the UK government is 547% of GDP). This does not mean that the US and UK government are broke (or more likely to default than Switzerland). What it says is that relative to current policies, the US and the UK require larger increases in taxes or decreases in spending to stabilize their debt.

A similar analysis of the fiscal gap for the US has been done by Auerbach and Gale and they reach similar conclusions. The fiscal gap for the US government today is between 5% and 7% of GDP. Meaning that if the government wants to stabilize the debt at current levels over the next 8 decades, they need to increase taxes or cut spending by five percentage points of GDP (every year for the next eight decades). This is a very large number given that total federal tax revenues stand today at 15% of GDP (so 5 extra points amounts to a 1/3 increase in taxes!).

Given these numbers, why is it that Southern European countries are under more pressure than the US or the UK? It is all a matter of credibility and the trust in the ability of these governments to get their budget under control. It might be that the UK needs a larger effort than Ireland but the question is which one is more likely to deliver on this effort. And the moment credibility is low, interest rate spreads increase and the fiscal gap increases as well as you need to generate more revenues to simply cover the interest payment on the debt.

Credibility will always be a subjective assessment and it is always easy to argue that markets are getting it wrong (or right) for a given country. What is important is to understand the numbers, not just the current ones but the future ones as well, before making that assessment, otherwise we are only seeing the tip of the iceberg and ignoring the true size of the problem.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply