A flood of bad news plus Bernanke saying he will keep rates low sparked a mid-morning pop in equities. If you think equities are tracking recovery, think again – they are floating on easy credit going towards speculation, not investment. Consider these news items:

- New home sales drop to record lows

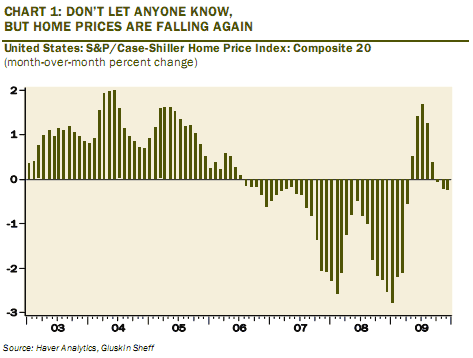

- Home prices fall again

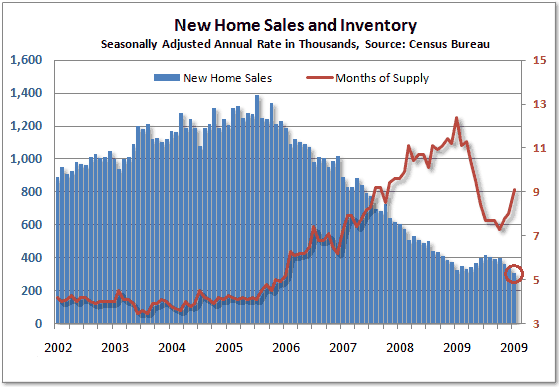

- Housing inventory (months of supply) rises again

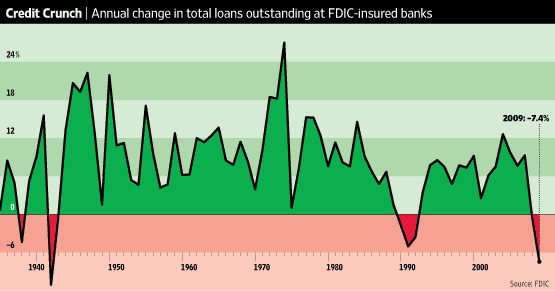

- Bank lending falls in sharpest decline since 1942 (!!)

- Consumer confidence falls after it had been rising (double dip?)

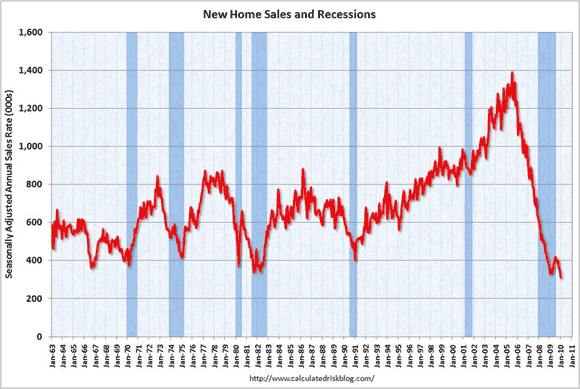

Calculated Risk has a plethora of charts on this morning’s announcement that new home sales (seasonally adjusted) fell to record low levels annualized as well as for a month, even below the prior record low of last January 2009, during the height of fear. You might think this a continued reaction to the end of the first-time homebuyer credit, but that credit was extended. Before the report Bloomberg reported that economists had expected a rise, so this report is unexpectedly bad – as bad as any period back before 1963, when the chart starts. Apparently the tax credit had already pulled forward new home buyers, so the extension has few suckers to pull in anymore. We should see a gap in demand for a while.

Lesson to be learned: gimmicks do create demand, they just pull it forward in time. The implications for recovery are profound, as no real recovery happens without new home sales.

New home sales are far more important for the economy than existing home sales, and new home sales will remain under pressure until the overhang of excess housing inventory declines much further

Housing inventory had been falling as banks worked through the subprime crisis, but are now rising again, indicating the second wave for foreclosure and mortgage defaults is beginning:

David Rosenberg of Gluskin Sheff pointed out this morning that housing prices are falling despite what you may be hearing in the mainstream media (chart courtesy The Pragmatic Capitalist):

The WSJ had a first page prominent article on bank lending falling, the sharpest decline since 1942 at the height of the war economy, which lowered private lending through industrial policy to retool for war. This too is really bad news, as it means banks are not lending but taking all the bailouts and cheap reserves and using it to buy financial assets (Treasuries, stocks).

The rebuttal to those Keynesian cheerleaders is that government stimulus freezes private investment, a phenomenon quite visible in the second half of the the Great Depression. Simple formula:

Banks don’t lend, business doesn’t borrow, people hide their savings in Treasuries = economy is on government life support

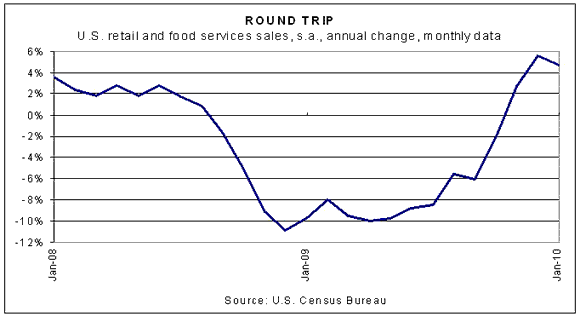

Now we begin to have worries on retail. Retail numbers still seem to be improving, and Wal-Mart (WMT) announced good earnings, but warned about declining store comps and deflation in prices, and now Nordstrom (JWN) is warning about 2H10 results. When January numbers were announced, retail seemed to have normalized (see chart from The Capital Spectator), but we may be seeing a snap-back from distressed circumstances, not a return to recovery:

James Picerno had a sound conclusion to this news:

No matter how you slice it, it’s all about the labor market for the foreseeable future—and how the ongoing struggle to mint new jobs will impact spending. The next clue comes tomorrow, when the Labor Department updates the latest initial jobless claims.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Banks continue to show their disdain for Main Street as they posted their sharpest decline in lending

We know they move money around but they produce nothing. They add nothing to our economy. They are parasites who suck the lifeblood out of our country.

They manage to filter billions if not trillions of dollars away and pay huge bonuses to their executives who created the enormous debt we are all facing.