The market can remain irrational longer than you can remain solvent – John Maynard Keynes

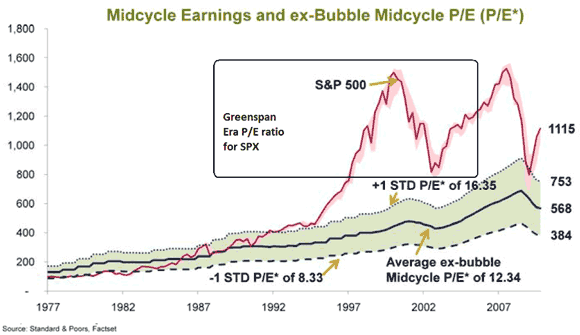

Continuing with the question of could the market have bottomed when we still have nosebleed P/E levels, Barry Ritholtz posted a great chart on how Greenspan/Bernanke bubble policies have elevated P/E ratios well above historical norms:

The dot-com bubble took off in 1994 at the upper level of normal and shot well above. (The envelope is +/- one standard deviation of normal.) We briefly touched the upper envelope in Mar 2009 and then took off again.

Most likely explanation for elevated PEs since 1994 is the excessive credit promoted by Greenspan and continued by Bernanke: elevated stocks are due to easy credit. Credit tightened at the two peaks and then was radically loosened at the two bottoms, in 2002 and 2009.

Normally any bubble returns to its start point, which still points to a true bottom at around Sp400. If earnings generally increase, the bottom should increase with it (ie the envelope is modestly rising), but the recent period of depressed earnings have turned this slow growth back down in 2009.

Implication is: we do not fall to normal until the easy credit abates. Timing looks like 2011, as Bernanke seems likely to exit very slowly this year. Hence:

Paradox of Recovery: when the private economy really shows signs of recovery, not just government life-support, easing will ebb and equities will fall

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply