Another day, another bout of troubling news on Greece – the German business lobby is now calling for Greece to lose all EU voting privileges until they sort themselves out, and Martin Feldstein is calling for a cheeky tactical exit and 30% currency realignment. Dr. Feldstein is almost certainly displaying a bit of naivete in his apparent belief that both the market and the rest of the EU would allow Greece back into the monetary union after a simple step reval.

Really, it’s hard not to have sympathy with the belligerent stance of taxpayers in EMU anchor nations; Greece has pretty clearly abrogated the “social contract” of EMU membership with its cavalier tax collection and lush transfer payment policies; regardless of how this specific episode plays out, the lack of an enforcement mechanism on the fiscal behaviors of member nations represents a significant flaw in the project of monetary union.

Fortunately for the Greeks, at least some of the focus on “sovereign risk” has been diverted to bigger fish, courtesy of yesterday’s TIC data in the US. This data is dangerously opaque and limited at the best of times, capturing as it does only a partial snapshot of capital flows; in a Setser-less world, it has become increasingly difficult to “follow the money.”

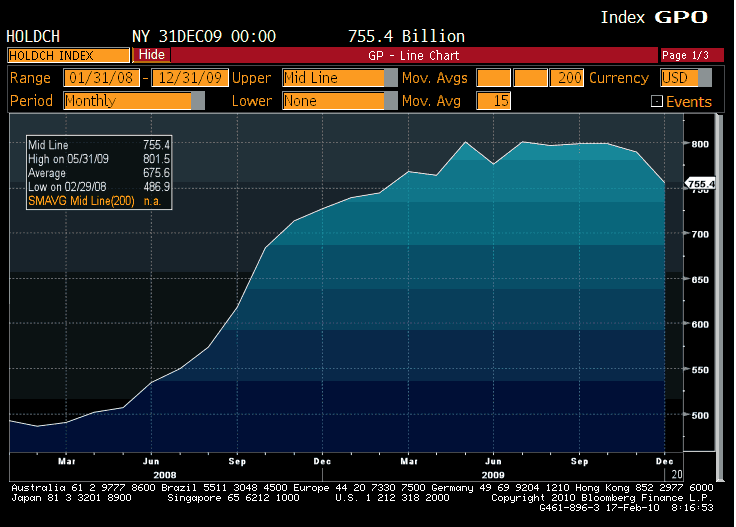

Yesterday’s TIC data was a case in point. China’s holdings of US Treasury securities fell sharply, prompting reports that Voldy and the Death Eaters were dumping US bonds (perhaps as a geopolitical warning shot?) and the usual hand wringing press reports. You can see the decline in China’s UST holdings below. Uh-oh, right?

(click to enlarge)

Not so fast, my friend. That decline in China’s US Treasury holdings wasn’t a sale at all; it was simply the maturation of a slew of bills, many of which were no doubt purchased in the huge run-up of China’s holdings a year earlier. The proceeds from the maturing bills would have been left on deposit, which isn’t captured in the TIC data; as such, that bill roll-off simply represents a change in the assets captured in the data. Looking at the performance of Treasury bills since late November, it certainly doesn’t seem as if the US Treasury has had much trouble flogging paper since China’s “earth-shattering” decision.

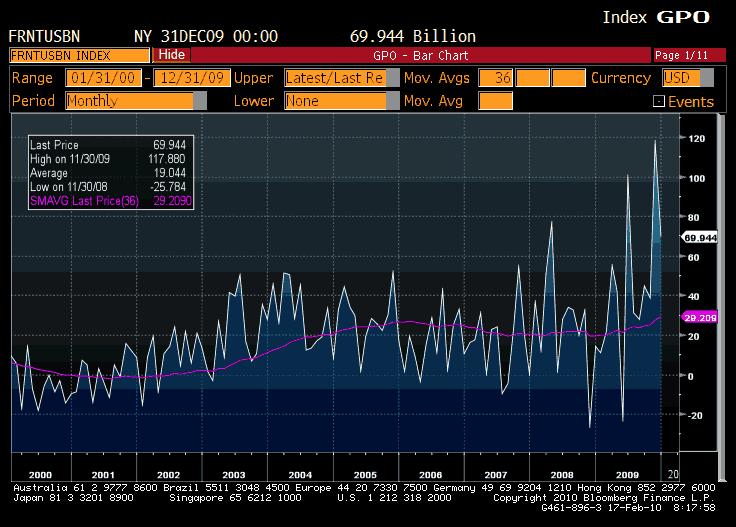

Amusingly, despite the provocative headlines, China was actually a modest net buyer of Treasuries in December…and they had plenty of company. Net foreign purchases of Treasury bonds and notes totaled nearly $70 billion, down: down, in fairness, from November’s $117.88 bio, but still the fourth highest month for foreign Treasury buying on record. Perhaps the financial press should hire Frank Drebben to report on the TIC.

(click to enlarge)

Not that this means that either Treasuries or the dollar are bullet-proof, of course; Macro Man continues to like being short the “QE withdrawal” bonds markets against those that won’t have to experience the dubious pleasures of cold turkey this year.

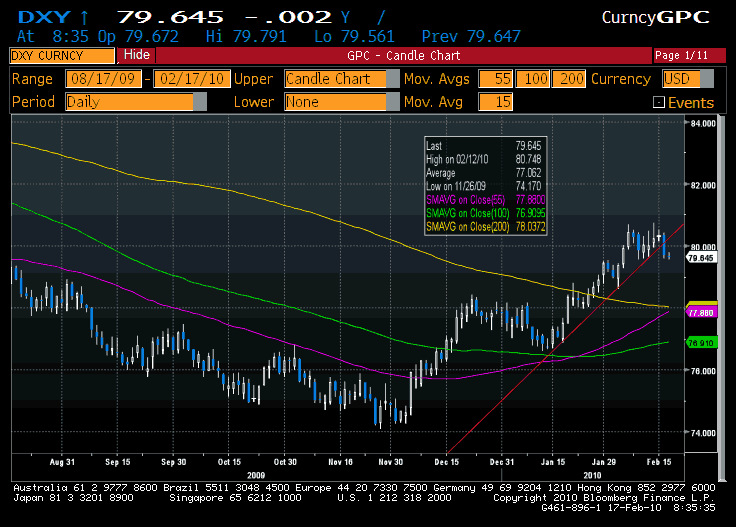

The dollar, meanwhile, has at least temporarily re-asserted its link with equities, as the DXY followed yesterday’s strong “synthetic Monday” showing by breaking its one month trendline.

(click to enlarge)

Insofar as we might reasonably expect a moratorium on real news out of Greece for a bit, it would not be unreasonable to expect a bit more of a bounce in the euro and other “risky” currencies. Until the EU decides what to do about its unrepentant black sheep, however, it would seem that short-covering rallies in the euro might represent little more than a selling opportunity.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply