The Bureau of Economic Analysis reported today that the seasonally adjusted real value of the nation’s production of goods and services grew at a 5.7% annual rate during the fourth quarter. That’s great news, but…

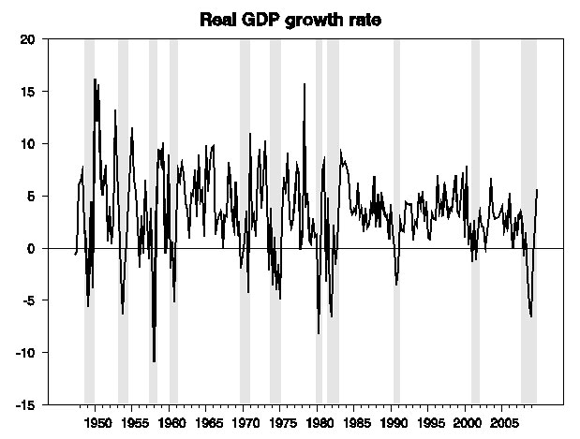

Rate of growth of real GDP (annual rates), 1947:Q2 to 2009:Q4. Shaded regions represent dates of recessions as declared by NBER.

Three-fifths of that Q4 GDP growth came from the fact that businesses were drawing down inventories more slowly than they had the quarter before. Firms sold $8.5 billion more goods (at a quarterly rate) in 2009:Q4 than they produced, and met those sales by drawing down inventories by $8.5 billion. This reduction in inventories counts as negative investment spending of -$8.5 billion at a quarterly rate (or -$34 B at the annual rate these numbers are typically reported) for purposes of calculating fourth-quarter GDP. Firms sold $34.8 billion more than they produced in 2009:Q3, which amounted to negative inventory investment of -$139 B at an annual rate for Q3. Since this component of investment spending went from -139 to -34, it counts as positive growth when you compare Q3 GDP with Q4 GDP. This mechanism alone contributed 3.4 percentage points to the 5.7% growth rate for real GDP reported for Q4.

To put it another way, if consumers, businesses, foreigners, and the government had all purchased exactly the same quantity of real goods and services in 2009:Q4 as they had in 2009:Q3, more of those sales would have come out of inventory drawdown in Q3 than in Q4, so even without any gain in final sales we would have had to produce more stuff in Q4 than Q3, specifically, 3.4% more stuff at an annual rate. In fact real final sales to consumers, businesses, foreigners, and the government were not stagnant, but grew at a 2.3% annual rate during the fourth quarter, and the two effects combined give us the 5.7% reported GDP growth.

Just because the production gains can be accounted for in terms of slower inventory drawdown doesn’t mean they aren’t real, and doesn’t mean they can’t continue. I noted in July that we might expect inventory restocking to add 1.6% to the annual GDP growth rate for each of the first four quarters of the economic recovery, and we haven’t even yet begun that inventory restocking process. The question, though, is what we’ll see for the other components of GDP. Exports grew more than imports in Q4, with the result that net exports contributed 0.5 percentage points to that 2.3% growth in real final sales. That’s certainly a very welcome development and a critical step for correcting the imbalances that have been very troubling over the last decade.

Government spending made no contribution to Q4 growth, which again is a consequence of the algebra of growth rates— since real government purchases in Q4 were about what they had been in Q3, they made zero contribution to the growth rate, which is based on the change between Q4 and Q3. Fixed investment contributed 0.4 percentage points and consumption 1.4 percentage points to the 2.3% growth in real final sales and to the 5.7% growth in real GDP. Those are better numbers for consumption and fixed investment than we’d been seeing in the first half of the year, but not the sort you’d expect if a normal strong recovery was now fully in play.

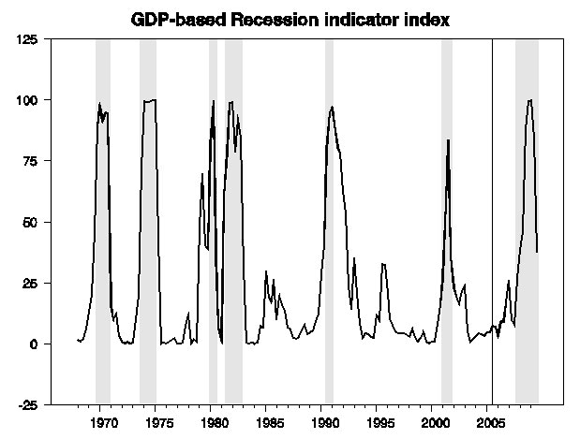

The new GDP numbers allow us to update the Econbrowser Recession Indicator Index for the preceding quarter (2009:Q3), which now stands at 37.6%. This is a pattern recognition algorithm for dating business cycle expansions and contractions that waits one quarter for data revisions and clear trend identification before making an assessment. The value of 37.6 means that the preponderance of evidence favors the inference that the recovery began in 2009:Q3. However, the index has not yet crossed the 33% threshold at which, according to our predetermined rule, we would declare the recession to be over. Once the threshold is crossed, we will use the full set of revised data available at that time to assign a most probable date for the beginning of the expansion. If the currently reported 5.7% growth holds up under data revisions, I would expect the algorithm to generate on April 30 a formal declaration that the recovery began with the weak growth of 2009:Q3.

The plotted value for each date is based solely on information as it would have been publicly available and reported as of one quarter after the indicated date, with 2009:Q3 the last date shown on the graph. Shaded regions represent dates of NBER recessions, which were not used in any way in constructing the index, and which were sometimes not reported until two years after the date.

Strong GDP growth with weak fundamentals

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply