While the entire market (at least in London) appeared to be on Greece death watch yesterday, those pesky Hellenes have thus far lived to fight (or at least to trade) another day. That March 2010 CDS got paid up yesterday is hardly a good sign, though whether the purchaser possesses inside information or simply a desire to push Greece towards the brink is thus far uncertain.

Omitted from yesterday’s post on DC fireworks was, of course, mention of the AIG hearings, for the simple reason that Macro Man could not see much chance of market moving developments. So it turned out, though the entire sordid spectacle does little to cast the American policy-making mechanism in anything but the harshest of lights. Not that the organs of government are any better elsewhere, mind, and perhaps it is a check mark in America’s favour that there is at least the platform to attempt to discover the truth.

While Macro Man is tempted to put Holmes on the case, he fears that even that worthy might taste the bitter sting of defeat; when confronted with an adversary possessing the malice of a Moriarty with the elusiveness of an Irene Adler, victory is far from certain. Suffice to say, however, that Tim Geithner is the man to have if you are participating in an Obama Cabinet dead pool.

As for the Fed, there were some modest changes to the statement which summed to “something for everyone.” While the outlook seemed to be upgraded modestly (the statement forecast a higher level of resource utilization, which is presumably a prerequisite for policy tightening) and Tom Hoenig preferred to eject “the extended period ” language ASAP, the removal of the warm ‘n’ fuzzy vibe on housing suggests that the committee is aware that downside risks still remain. All in, to Macro Man’s reading it meant that we’re a bit closer to the time of the first policy adjustment, and he finds it hard to take issue with the modest uptick in yields observed since 7.15 pm London time- particularly given how strong fixed income had traded over the past week or two.

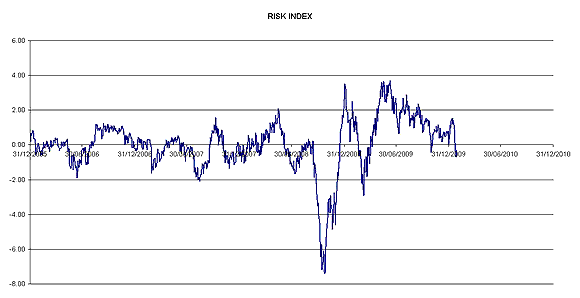

While equities eventually shrugged off the move in yields to put in a strong close for the first time in a week, Macro Man was interested to observe that his proprietary measure of risk appetite has recently moved to its most negative level since last March. What is curious is that the aggregate level of risk appetite has been positive since the beginning of 2008, with an average daily reading of 0.19 on the scale of the chart below. It’s quite extraordinary, really, given the 7.3 standard deviation event observed in late ’08, and it would not appear to be an unreasonable proposition that we are now overdue for at least a modest bound of risk aversion.

As for the State of the Union address, Macro Man has a couple of thoughts. While Obama, true to form, tried to strike a broadly encompassing tone in his remarks (“Democrats and Republicans. Democrats and Republicans.”), the little jabs towards financiers were neither surprising nor particularly potent, and more or less confirmed that the Bush tax cuts would not be renewed. This is an easy win for him; he’ll be able to tighten fiscal policy through inaction, rather than action and be able to claim that he hasn’t actually raised taxes.

While his frequent references to individual success stories of his policies were clearly intended to personalize his appeal, Macro Man couldn’t shake the (admittedly cynical) thought that it instead confirmed that his efficacy was so limited that the few positive results could be identified by name.

In any event, while improving the labour market is of course a worthy goal, Macro Man is let to wonder what increasing employment at all costs will do to productivity, unit labour costs, and, ultimately, competitiveness. While it’s easy to say “we want manufacturing jobs to return to the US”, the fact remains that blue collar workers are facing literally unprecedented competition from much lower-cost alternatives in EM economies. It’s hard to see how that dilemma is resolved without subsidies, tariff barriers, or other forms of protectionism. Yeah, it makes for a nice sound bite to mumble about “green jobs” and the like, but they aren’t going to save the day automatically.

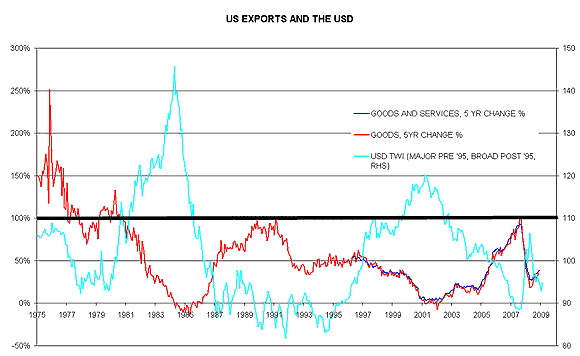

Perhaps the most interesting part of the president’s speech was his stated desire to double exports in the next five years. By this, Macro Man presumes that he means the gross level of exports, rather than net exports (which are currently negative, and the deficit could easily double in 5 years with no help from him.) Talk about “competitiveness” and “fair trade” also set the protectionist alarm bells ringing, particularly when taken in conjunction with his comments on employment.

A 100% rise in exports over a five year period is a challenging but not impossible goal; both Bush I (goods and services) and Bush II (goods) accomplished the feat in the past thirty years. O course, both of these periods had something in common: an extremely weak dollar. Indeed, since 1980 the correlation of the trailing 5 year growth rate in exports and the level of the trade-weighted dollar has been -0.56, which is quite a strong (if unsurprising) relationship between two such simple factors.

What does it mean? Perhaps nothing in the near term. But Macro Man does wonder about the fate of the strong dollar policy, in both its literal and figurative forms. Hmmmm. Competitiveness….bring manufacturing jobs to America….double exports. It all smells like a harder line on China specifically and trade generally from Obama, which shouldn’t come as a total surprise; why should trade be exempted from the increasingly dirigiste policy stance of the Administration? (Unless, of course, Obama expects US manufacturing to conquer the world with this catalogue of useful products.)

So if Macro Man’s Cabinet dead pool tip is correct and Geithner falls on his sword, ’twill be very interesting indeed to see who his replacement might be. A new broom at Treasury may well bring new ideas….bashing mercantilism and weakening the dollar might very well be among them. Stay tuned.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply