It’s a big day in D.C. today, indeed it should prove to be a big couple of days. Tonight we’ve got the FOMC announcement and Obama’s first State of the Union address, followed tomorrow by a Senate vote on cloture in the Bernanke debate and, possibly, on the confirmation itself.

Given the timing of the first and third of those, it would appear unlikely that the Fed will rock the boat too hard at this evening’s announcement. “Extended period” seems likely to remain, and it is likely somewhat premature to expect changes to the discount rate (though a recent hot ‘n’ heavy rumour suggested a rise is possible come March.) While there have been some suggestions that the Fed would change its policy mechanism to target interest paid on reserves rather than the Fed funds rate (given that they have lost effective control of FF given the participation of the GSE’s in that market), such a significant policy shift two days before the possible exodus of the current chairman would appear to be very unlikely indeed.

As for Obama, he’ll naturally touch on both health care and foreign policy, but from a market perspective the most interesting aspects of the speech will be his rhetoric towards the banks and his comments on fiscal policy generally. While the president may not be sporting a hair shirt when he makes his speech, “austerity” may be the new religion- both in terms of banks’ capacity to earn, and the government’s capacity to spend.

How effective such a policy stance ultimately turns out to be remains to be seen, of course, given that passage through Congress remains uncertain. On the face of it, however, less earnings for banks and less spending by the government should generate a widening of swap spreads. 10 year swap spreads are only a few bps from their lows and remain well below levels prevailing before the crisis. While this has been a function of both increased Treasury issuance and the assumption that TBTF banks are ultimately a public sector liability, a general policy move towards weaning banks from public support should re-introduce a credit premium into their liabilities.

Indeed, since Obama’s announcement last week, a basket of CDS spreads of 4 US banks (BAC, C, GS, and MS) has widened modestly, as one might expect, though it remains well higher than levels prevailing at the outset of the crisis. The relationship between banks CDS and swap spreads has been a convoluted one during the crisis; since July 2007, the correlation between the two has been -0.41 (implying that wider bank CDS means tighter swap spreads.) However, since the advent of QE and the “normalization” of markets in March ’09, that correlation has flipped to a more sensible +0.22. Macro Man would expect that relationship to continue, particularly if and as some institutions contemplate withdrawing from bank holding status (and thus the warm embrace of government guarantees.)

Elsewhere, Europe is no less interesting today as the orgy of demand for that Greek 5-year issue has yet to materialize in the secondary market. Amusingly (at least for those who didn’t participate), the bond has sold off back towards its original offering guideline of swaps + 375 (versus an issue price of swaps + 350.) For all the sturm und drang about the leechiness of big global banks, the underwriters did a superb job of drumming up interest in this sucker and saving the Greek government a few euros.

Meanwhile, BBVA’s net Q4 profits fell a cheeky 94% y/y courtesy of a slew of writedowns. Following on from similar disclosures from Soc Gen, it would appear that European financials are finding it increasingly difficult to keep juggling all the balls in the air without letting a few drop to earth.

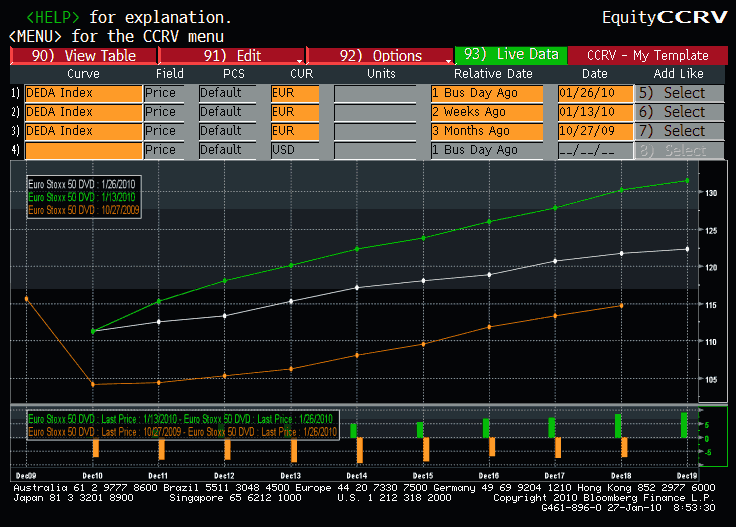

The trend, should it continue, could pose something of a threat to European dividends. Macro Man noted a couple of weeks ago that he had vacated the last of his positions. While the strip is off quite a bit since then, it’s still comfortably higher than the levels prevailing 3 months ago. Given that the market is still quite long of these suckers, particularly relative to the available liquidity in any sort of stressful environment, risks must surely point towards further weakness if and as the European banking distress theme gets legs. This should ultimately provide an excellent opportunity to get back into the trade, hopefully at a more tasty discount to the expected divvy stream. This morning’s focus on the re-emergence of a bearish Roubini does little to suggest that the time to re-enter is nigh.

(click to enlarge)

That Axel Weber has emerged from hibernation and spread his hawkish wings this morning does nothing to make risky assets seem more enticing. Nor indeed does the by now obligatory Chinese rumour du jour, which this morning suggested that some banks have been ordered to withdraw loans that they’d agreed to extend in the first two weeks of the year. Per the usual, there was no confirmation, but the story didn’t stop Asian equities from putting in yet another disappointing day.

It might be a big day in DC, but as noted yesterday it’s a pretty eventful time elsewhere, as well. Whether the stars are aligning for a proper risk asset dump remains to be seen, but thus far Macro Man has seen little to contradict the thesis that the next decent move will be down.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply