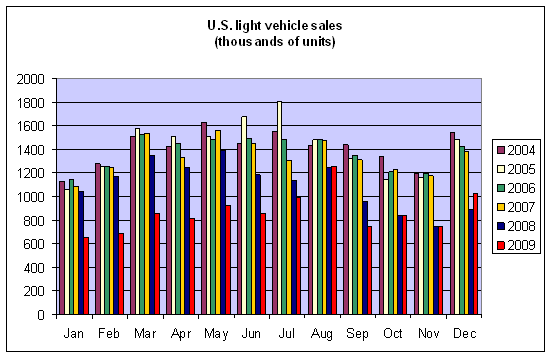

December auto sales looked reasonably good, at least when you compare them with the numbers we’ve been seeing over the last 15 months. Apart from the cash-for-clunkers August 2009 outlier, seasonally unadjusted U.S. car sales in December were higher than any month since the Lehman failure in September 2008. Even so, that still leaves December 2009 30% below the average December over 2004-2007. The worst may be behind us, but we’re still a long way from normal.

But without question Friday’s report that seasonally adjusted U.S. payrolls declined by another 85,000 workers in December was a disappointment. I recall that when President Obama was asked on February 9, “how can the American people gauge whether or not your programs are working?”, he responded:

I think my initial measure of success is creating or saving 4 million jobs. That’s bottom line No. 1, because if people are working, then they’ve got enough confidence to make purchases, to make investments. Businesses start seeing that consumers are out there with a little more confidence, and they start making investments, which means they start hiring workers. So step No. 1, job creation.

With Friday’s numbers, total U.S. employment has now fallen by over 4.1 million jobs, from 135.1 million Americans working in December 2008 to 130.9 million a million last month. That’s a bigger loss (by about a million workers) than was seen in any other 12-month interval between 1939 and 2008.

If you’d hoped that growth in employment had finally begun, Friday’s numbers were rudely disappointing. But if you instead had been seeing an anemic recovery not yet strong enough to bring employment up with it, this week’s news says that’s still about where things stand. Andrew Samwick and Phil Izzo survey some of the different responses to the employment report. I think Donald Marron had the right perspective:

job losses averaged 69,000 per month in the last quarter of 2009. That’s unwelcome, but much better than the average of 691,000 jobs lost in each of the first three months of the year.

Rather than a robust V, the recovery seems to be held back by ongoing deleveraging by consumers and the institutions that would lend to them. If that continues, we might expect to see continuing output growth in 2010 that eventually starts to bring employment back up, though it may be a long time before employment levels return to those achieved in 2008.

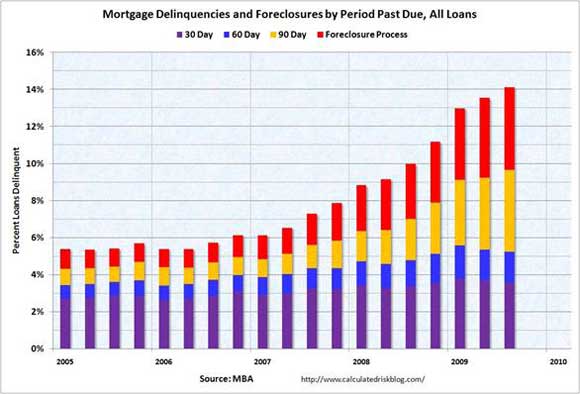

As long as the status quo continues, the recovery still has a lot of fragility. As the president observed, job losses themselves contribute an unfavorable dynamic to spending and bankruptcies, and there are a lot of mortgage delinquencies that have not yet reached the foreclosure stage. I do not rule out the potential for another round of concerns about the solvency of key institutions as those developments play out.

So yes, the situation continues to improve, but no, it’s not anywhere near where we’d like it to be.

Charts: WardsAuto, Calculated Risk

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply