Usually when we talk about savings rate, we talk about the savings of our citizens. This personal “savings” rate should not be confused with money that is in savings accounts. No, the savings rate is a calculation based upon how much money is not being spent on other things. And this means that DEBT REPAYMENT generally counts as personal savings.

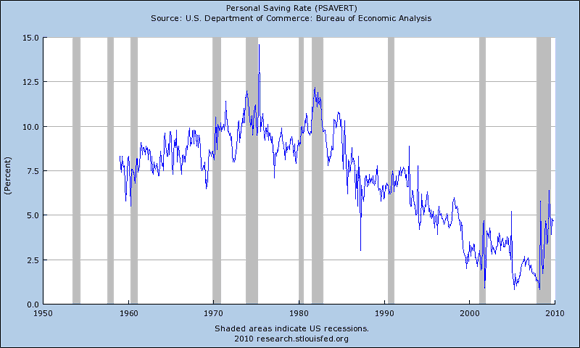

The personal savings rate went negative (although no longer reflected on the Fed’s charts), but since this crisis began has turned back positive, the result of citizens pulling in their spending while deleveraging by paying off debt. Below is the chart of the Personal Savings rate, it is currently just below 5%:

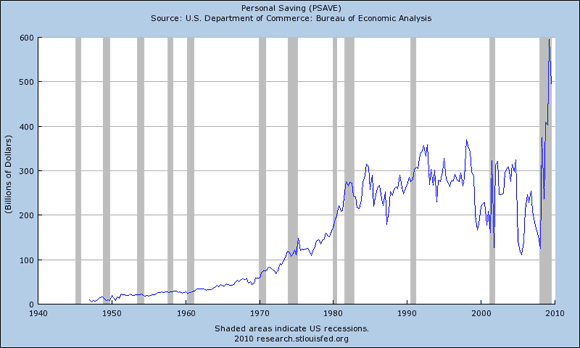

The next chart shows the personal savings AMOUNT in billions of dollars:

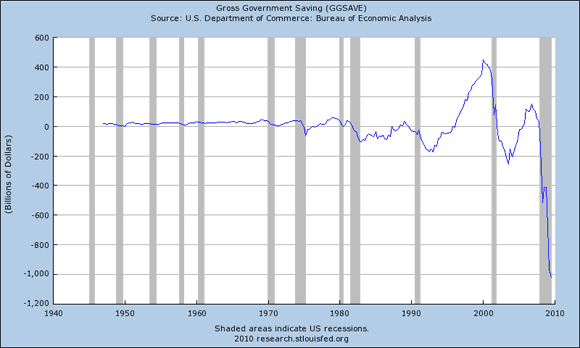

What is occurring is that the government, of course, is trying to make up for the slowing by spending themselves into huge deficits. Below is the chart showing Gross Government Savings, a hugely negative figure, one that I contend in reality is many times larger:

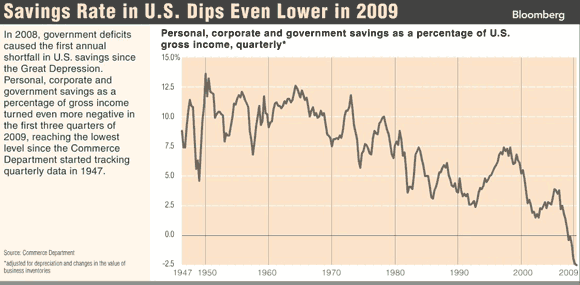

If you take personal, corporate, and government savings and combine them into one chart, you wind up with the lowest overall savings rate since the Great Depression, and once the 4th quarter is tallied, 2009 will likely wind up being the worst year ever:

Below is the Bloomberg article that discusses this chart:

U.S. Savings Rate Falls to Depression-Era Levels: Chart of Day

By David Wilson

Jan. 6 (Bloomberg) — Government deficits have caused the U.S. savings rate to turn negative for the first time since the Great Depression, and the gap is widening even as households and companies put away more money than ever before.

The CHART OF THE DAY shows net savings, adjusted for depreciation and changes in the value of business inventories, as a percentage of gross income. This rate is provided by the Commerce Department on a quarterly basis since 1947, when the chart begins. Annual figures go back to 1929.

The savings shortfall widened to negative 2.3 percent in the first three quarters of last year from negative 0.2 percent in all of 2008. Before 2008, there hadn’t been a full-year drop since 1934, the last year of a four-year period when rates were below zero.

Deficit spending by the federal government reduced net savings at an annual rate of $1.33 trillion during last year’s third quarter. State and local government deficits widened the gap by another $14.9 billion. At the same time, personal and corporate savings increased by a record $983 billion.

Health-care outlays represent “the key for savings” in the next few years, according to Michael Mandel, president of South Mountain Economics. The former chief economist at BusinessWeek magazine — now owned by Bloomberg LP, the parent of Bloomberg News — published a similar chart two days ago on his Innovation and Growth blog.

“The U.S. will be stuck between a rock and a hard place” if costs keep soaring, Mandel wrote yesterday in an e-mail. “If health-care reform manages to restrain spending, then we’ll see net national savings eventually head upwards.”

What all this shows is simply that your government is spending your savings faster than you can save. This is a symptom of DEBT SATURATION and attempts to create never ending credit growth. We are all just going along for the mathematical ride at this point, that is until and unless we can resume control of our government, and take it back from the hands of the central bankers and other special interest groups.

Speaking of special interest groups, LOL, “If health-care reform manages to restrain spending?” Is he kidding? That’s the funniest one I’ve heard yet from an “analyst.” Sure, we all expect such lies now from our politicians. Want to know why we have come to expect it?

Try $126,536,249 reasons why. This is how much money was contributed to the campaigns of 100 Senators who voted on the latest health care “reform.” Please review the table at the following link: The Senate Passes Health-care Bill – A look at how members of the U.S. Senate voted (ht W.S.).

I’m not even sure if that includes money from the insurance industry or not. I’m guessing not, and they are likely to be the largest winners. This is how things currently get done in the United States, not on your behalf, but on behalf of those who make the largest contributions. The largest contributors of them all? Central bankers, of course.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Have you seen more recent figures? Does the Fed report on personal savings rates on its website? I’m wondering what personal savings rates are doing.

I did not know that paying down debt counted as Saving. Then my Saving has been high for some time I guess, not just since I got it all paid off this year (w00t!).