The dollar raced higher this morning against the Euro and against the Yen, reaching the 77 level. Long bonds are lower, continuing their breakdown for now. Oil is up slightly but is failing, so far, to get back above $70 per barrel, while gold is down pretty sharply.

The worthless Goldman ICSC sales report showed a .4% gain week over week, and a 2.4% gain year over year. Redbook showed a 1.5% yoy gain. Funny, but sales tax revenue are still showing historic collapses, just yesterday we learned, “Texas collected $1.7 billion in sales taxes last month, down 14.4 percent from November 2008. It was the tenth month in a row of year-over-year declines and the sixth consecutive month of double-digit percentage drops.”

If Texas is even close to the mean, the disconnect between reports like Goldman’s and reality are historic in nature as well.

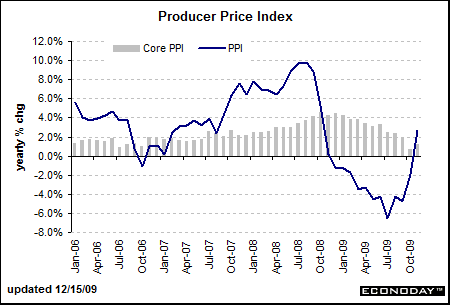

Want to know what results when you pump money into a debt saturated economy, and your money is backed by debt? Okay, here is the PPI report that showed a leap from a yoy -1.9% change in prices to a positive 1.8% change, a yoy jump of 3.7%!!

Highlights

We got the worst of both for this morning’s initial economic news. Producer prices surged while Empire manufacturing fell back sharply. Energy costs jacked up the headline PPI for November but the core also rose significantly. The overall PPI jumped 1.8 percent in November after gaining 0.3 percent in October. The boost in the latest month far exceeded the market forecast for a 1.0 percent increase. The November gain was led by a 6.9 percent spike in energy and a 0.5 percent gain for food. At the core level, the PPI rebounded 0.5 percent after a huge 0.6 percent drop in October. The market had projected a 0.2 percent rise for the latest month. It is easy to jump on the worry wagon about inflation from today’s report. But there should be a little caution about that. Oil prices have since come down and the jump in the core partly or mostly reflected getting back to near-term trend after October’s sharp drop. The core rebound was mainly for light trucks and cigarettes.

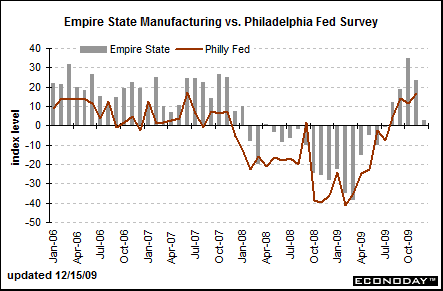

Okay, so we had a large speculative spike in oil, but we know that oil is down about 14% in just the past few weeks. This will have the inflationist’s screaming, but I’m sticking to the deflationary force thesis. Why? Well, let’s take a look at the Empire manufacturing report – the general business index had gone back positive, last month it was 23.51. Expectations were for it to grow to 25… instead it came in at only 2.55! This took off 89% of the positive growth in just one month:

Highlights

Month-to-month growth slowed to a crawl in the New York manufacturing region, according to the Empire State index which barely came in above zero for the December reading, at 2.55 vs. far stronger rates of growth in November (23.51) and October (34.57). Nearly everything is slowing this month: new orders 2.20 vs. November’s 16.66, shipments 6.30 vs. 12.97, employment -5.26 vs. 1.32, workweek -5.26 vs. 5.26, and unfilled orders, -21.05 vs. -2.63. The month-to-month contractions in unfilled orders and the workweek are bad news for the area’s factory workers, especially those that are unemployed right now.

Prices paid (inputs) was one thing that didn’t slow, at 19.74 vs. 10.53. But the region’s manufacturers definitely don’t have the pricing power to pass through the higher costs to their customer as prices received (outputs) is showing deepening contraction, at -9.21 vs. -2.63.

Even the general six-month outlook fell back, to a still strong 43.01 but down nearly 14 points from last month. Today’s report is surprisingly soft but will have to be confirmed by tomorrow’s Philadelphia report on the Mid-Atlantic region before questions emerge over manufacturing, a sector that is definitely moving forward though its pace is uncertain. Later this morning the Federal Reserve will post the October U.S. industrial production report, the heart of which are the manufacturing components.

So, clearly the strategies of the pump monkeys like Bernanke are failing to produce anything but speculative price increases in localized commodities like oil. The mark to fantasy world of paper has been fluffed, but the real world is still in the toilet. My thesis here is that while the overall PPI turned positive, the moment the stimulus is removed you will immediately return to deflation. In fact, it may be returning regardless, look at oil. And because of their debt pumping and pushing, each subsequent down cycle will be worse than the last.

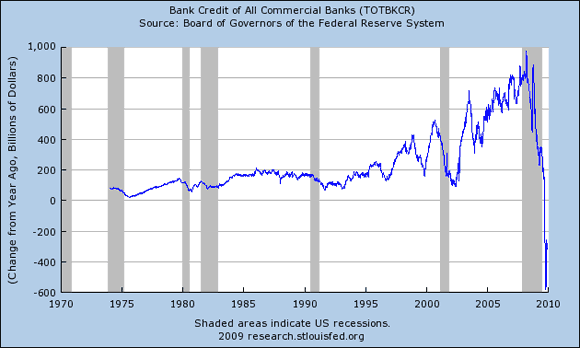

Yesterday Obama (sarcasm on) really told off those “fat cats” on Wall Street! (sarcasm off). Why he had them so shaking in their boots that Bank of America (BAC) even offered to pump an entire $5 billion into small businesses! Like that would actually have a significant impact… look at the total bank credit figures, this is how much they have fallen in the past year:

Of course what Obama does not get is that you can’t push more credit into a credit saturated environment! Oh, you can try, but it won’t work! Incomes are not high enough because we don’t do anything real! Thus, the people cannot afford to keep afloat the overbuilt strip malls, coffee shops, bubble priced auto dealerships, etc.

The more they flood the country with debt backed money, the worse this disparity is going to get. Have you ever seen such disparity in two reports like the PPI and Empire Manufacturing reports above? I haven’t.

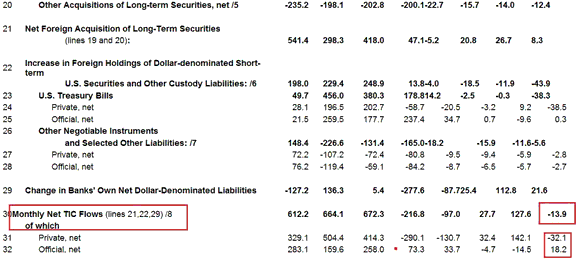

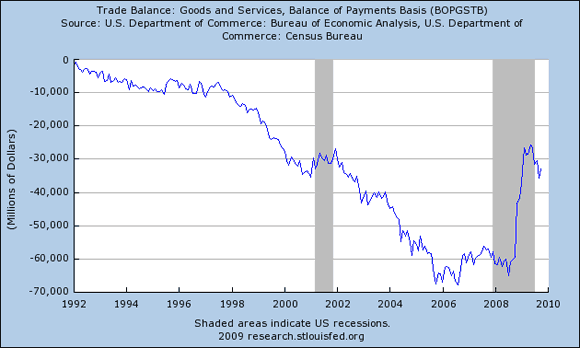

And the monthly TIC data (Treasury International Credit) came out for the month of October, it went back negative again, this time the net TIC flows were negative by $13.9 billion. Keep in mind that we are still running a $30 to $40 billion trade deficit each month that must be financed, that means that just for the month of October we were short of financing our consumption by about $55 billion:

Industrial production figures come out at 9:55 Eastern, should be interesting…

Yesterday Wells Fargo (WFC) announced that they are doing the same exact steps as BAC and Citigroup (C) did to pay off the TARP. This is Timmy Geithner playing tricks on the public and them selling stock to dilute current bag holders while they still can. What they don’t raise in equity sales they are going right back to the Fed and exchanging more garbage for taxpayer subsidized loans and in this way all the executives are snaking out from under those “ominous” bonus restrictions.

But even though they are offloading their waste onto the taxpayer via Fed, Treasury, and GSEs, they are still BURIED in it! Take, for example Citi. Remember their not so little SHELL GAME? They created another company (shell company which IS ILLEGAL) and moved their most toxic leftovers into that company, even Bloomberg is reporting on it:

Dec. 15 (Bloomberg) — Citigroup Inc. Chief Executive Officer Vikram Pandit, emerging from a U.S. bailout with higher capital levels and loan-loss reserves than any peer, still has a $617 billion reason to worry.

That’s the amount of assets left in Citi Holdings, the division that Pandit set up to strip his bank of unprofitable businesses, troubled loans and securities. While the bank has unloaded almost $100 billion of the assets so far, getting stuck with the rest may hinder earnings for years, analysts said.

Again, under the rule of law creating shell companies to shuffle assets around is ILLEGAL. Yet our government and regulators do nothing. Capital cannot flourish in this environment, that pile of rubbage is exactly what has “zombified” our banking industry. They need to be cleared out, but they need to be cleared via the rule of law!

Anybody else seeing some messages in the above data? I’m thinking that we’ve reached the point where cramming more debt into the system simply isn’t going to do anything productive!

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply