It’s been raining cats and dogs for most of the last week (though sadly not during this turgid display, which might have excused the unappetizing fare on offer), so Macro Man has domestic pets on the mind.

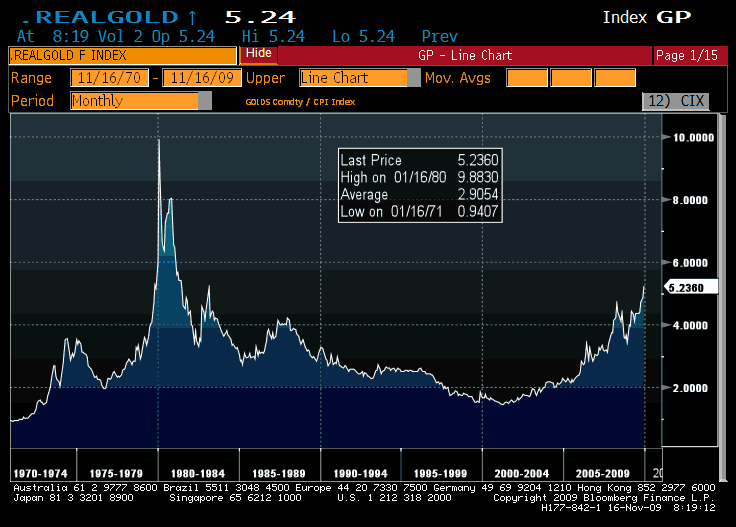

After a brief respite last week, it feels like every man, woman, cat and and dog in the world has put in a bid for gold, taking the shiny metal/only “real” currency/barbarous relic (delete as appropriate) to fresh all time highs. Or at least, fresh nominal highs. While gold is starting to get a bit of that “Nasdaq 1999” feel about it, Macro Man is well aware of the quasi-religious fervour of some of its adherents. And if we want to devise a measuring target, looking at the “real” price of gold (or at least, the price of gold deflated by headline CPI) isn’t a bad place to start. As the chart below suggests, the nominal price would nearly have to double to approach the early 80’s “real” highs, though the metal’s subsequent collapse suggests, post hoc, that such levels were, shall we say, bubblicious.

(click to enlarge)

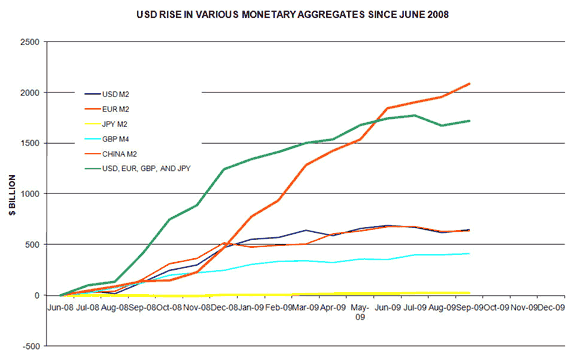

Meanwhile, in currency land, China and America are starting to fight like cats and dogs: a bit of barking and hissing with no real violence. The APEC meeting produced no substantive results, other than a cunningly-timed story in the FT in which China bemoans America’s monetary policy settings. Leaving aside the fact that no one forces China to get to the dollar or to set deposit rates at farcically low levels; perhaps we should just revisit the chart of aggreagate money supply growth over the past year-and-a-bit?

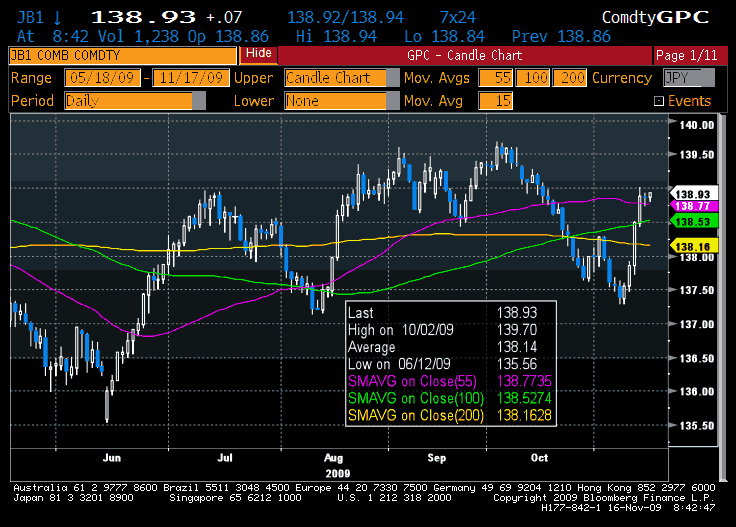

Moving along from cats and dogs to flamingos, Japan has hosted the latest painful goolie-squeeze of popular trades. Shorting “Japan, Inc.” has been a popular theme over the last couple of months on the deteriorating fiscal situation and underlying demographic challenges. At one point last week, Japan’s soverignn CDS premium was wider than that of Spain. (As a reminder, only one of those countries has $1 trillion of FX reserves.)

Anyhow, the worm turned towards the end of last week, and even a well-above consensus print on Q3 GDP (1.2% q/q, non-annualized versus an expected 0.7%) derailed the squeeze in JGBs.

(click to enlarge)

Four or five weeks to build a position and profit, a few days to lose it all. Such are the joys of portfolio management in a position-driven market. It almost makes arguing (or raining) like cats and dogs seem enjoyable by comparison…

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply