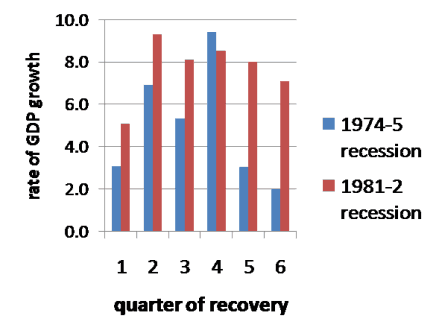

Paul Krugman has a very important post showing fast recoveries from previous big recessions. The 1983-4 recovery was particularly fast. But lest anyone think Reagan might have done any good he points out that a rapid recovery also occurred in 1976. So how did they do it?

I decided to go back and look at the data on fiscal stimulus, and was quite surprised by what I found. In both earlier recessions the budget deficit rose by just over 3% of GDP; from a bit under 1% to 4% of GDP between 1973 and 1975, and then from 3% to just over 6% between 1980 and 1982. I’m no expert on Keynesian economics, but isn’t that mostly the effect of the recession? I don’t see a lot of room for discretionary stimulus. And if we look at the especially fast 1983-84 recovery, we find that the discretionary stimulus that did occur was exactly the kind that Krugman says doesn’t do much good—tax cuts for the rich (who have a lower marginal propensity to consume.)

How about the current recession? I agree with Krugman that without more stimulus we are likely to have a very slow recovery. I hope I am wrong, and I admit that forecasting is very difficult. But I also wonder how a Keynesian would explain the expected slow recovery. Yes, we haven’t done as much as Krugman would like, but this time the budget deficit is rising from roughly 2% of GDP in 2007 to 11.2% in 2009; nearly three times the increase that occurred in the other two big recessions. And this time none of the stimulus is going to tax cuts for the rich. It seems like Krugman should have expected this recovery to be much faster than the 1976 and 1983 recoveries. And yet despite the fact that dramatically higher budget deficits seem to be associated with a much slower recovery, the logical solution seems to be . . . even more massive budget deficits.

Now I am sure that a good economist could find flaws with my analysis. Other things are never equal. I suppose one argument is that continuing banking problems make recovery more difficult this time. Or the overhang of unsold houses. Of course in 1983 there was an overhang of a lot of heavy industry in the rust belt that was gone for good. And the fast 1933 recovery occurred in the midst of severe banking problems.

But let’s suppose the recovery is held back by special factors, doesn’t that still beg the question of why the previous recoveries were so fast? In his previous post Krugman had plugged in the fiscal stimulus numbers and showed that the slow recovery we are getting is exactly what one would expect from the Keynesian model. Boy, am I happy to hear that!! I was getting tired of Keynesians telling me that the real reason for the fast Reagan recovery was not supply-side economics but rather ”good old Keynesian deficit spending.” But we now know from Krugman that the Keynesian model predicts that even if Reagan had done three times as much deficit spending (and by implication far more than three times the discretionary stimulus) the recovery would have been expected to be the sort of anemic 3% plus recovery we are expecting this time. Sure, you can quibble a bit with the numbers—income tax receipts are more cyclical than during earlier decades, so that explains some of the bigger deficit this time. But I don’t see how any amount of fiddling with the numbers will explain the 1983-84 recovery using a Keynesian model of stimulus. So the fast recoveries of 1976 and 1983 remain a mystery.

I think Krugman’s best argument would be that this time monetary policy is stuck in a liquidity trap. The Taylor Rule says we need negative nominal rates, and yet we have no way of getting them. I agree that monetary policy is the key. Where I disagree (as you all know by now) is that I think there are all sorts of ways of making monetary policy much more expansionary:

- Negative rates on excess reserves.

- Actual QE, not fake QE.

- Most importantly an explicit NGDP target path, level targeting.

But at least Krugman sees the real problem. I think most of the profession has still not realized how much more stimulus we will need unless we want millions of workers to remain unemployed far longer than necessary. His views are certainly preferable to Chicago School economists arguing that the relatively mild nature of this recession shows that fears of a severe recession were overblown. So kudos to Krugman for raising the alarm. BTW, I once heard a talk by Robert Lucas where he argued that despite the flaws in his model, Keynes was a great man because he had the basic insight that the Great Depression was unacceptable and it was up the the government to do something about it. I agree. Perhaps DeLong will have to add Lucas’ name to the good old Chicago School.

I’m sure there are errors in my analysis and look forward to the response of my Keynesian readers.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

This is just ignorant. How about a dose of reality. In 1980, a business started. The personal home computer business began to take off. It created wealth and jobs and the government could do very little to stop it. The best thing it did was lower taxes so people could invest in the new business. Seriously, to talk about that period without pointing out that the entire recovery was do to a brand new industry on the rise is just a rewrite of history.