This equity price action is becoming almost Biblical: “and on the fifth day, the market rose again….” Macro Man was somewhat bemused by the enthusiastic reception to yesterday’s GDP number, by the economics profession at least as much as the marketplace.

After a four-day slide, that an above-consensus real GDP print encouraged a bounce was hardly shocking, particularly in light of the history of the last seven months. Yet the reaction from sell-side economists: “A very strong report! We’re upgrading our forecasts!” bordered on the nonsensiscal.

For one thing, the margin of the consensus “beat” was razor-thin: 0.3% anuualized is less than 0.1% q/q. That this is the advance number that will be revised twice in the next month or two provides even less reason to go overboard with the enthusiasm.

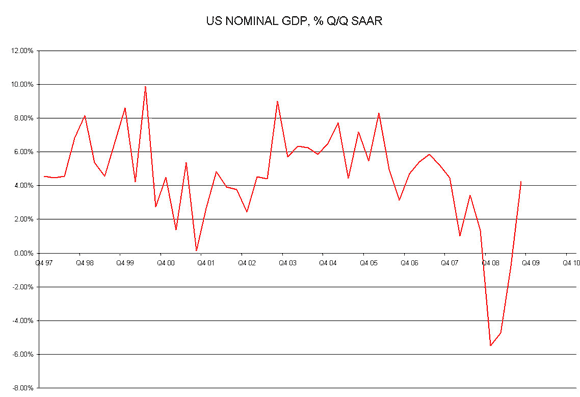

More viscerally, however, to Macro Man’s mind the report was actually worse than expected. Years of poring through Japanese national accounts data have taught him that in deflationary/bubble-bursting/highly distressed economies, nominal GDP is what matters. And on that score, the resultant figure- + 4.3% q/q, SAAR – undershot the 4.6% consensus by the same margin that the real figure beat it by.

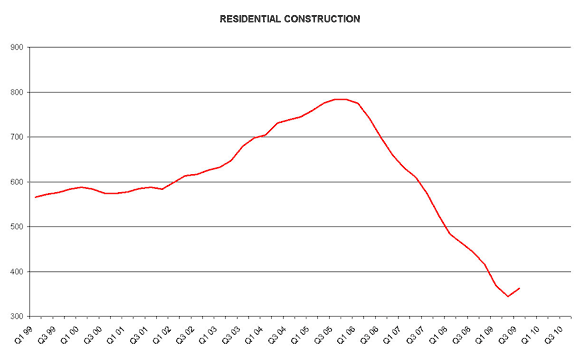

Moreover, as the chart above illustrates, the quarterly nominal growth was well below “trend”, even as the real figure exceeded trend. Colour Macro Man unimpressed. Of course, there were some positive aspects to the report: residential construction rose for the first time since 4Q05. Of course, whether that can continue with plenty of untapped housing supply from foreclosure sales remains to be seen. Similarly, the surge in auto sales and the decline in the savings rate last quarter suggests that it will be difficult to maintain a 2.36% contribution to growth from household spending.

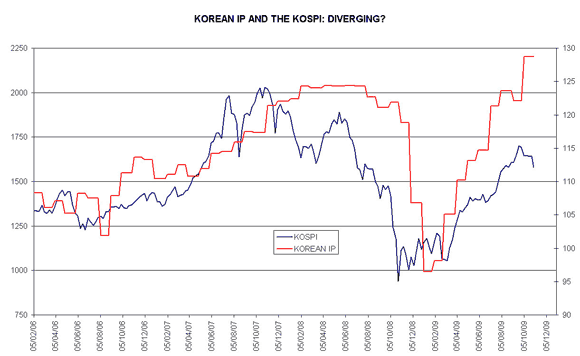

Meanwhile, the latest interesting twist out of Korea occurred last night. Industrial production surged 5.4% in September, taking the y/y growth rate to 11% and the underlying production index to an all time high. This, combined with the smart bounce in the US, surely gave a tasty boost to the Kospi, right?

Nuh-unh. After a half-hearted gap higher on the open, the index sagged badly into the close, falling to its lowest level since August 20th. The divergence between the Kospi and IP is curious, not least because the Kospi peaked more than a month ago, leading other markets by several weeks.

At the risk of beating a dead horse, Macro Man finds it very interesting and very troublesome that a cyclical market like Korea with apparently rock-solid macro fundamentals is trading so poorly. By way of comparison, the SPX was at 1007 the last time that the Kospi closed as low as it did today.

It’s the season for tricks and treats (hint: here comes the obligatory Halloween tie-in); somewhat worryingly, it’s becoming a tad tricky to tell the difference between them. The evidence is increasingly mounting that the naked liquidity trade is coming to an end, and that markets will soon have to float or sink on their own merits. Judge for yourselves what that implies for the goodies that have stuffed many high-beta portfolios over the past couple of quarters.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply