The bond fund PIMCO popularized the term New Normal to explain the investment environment for the next five years: low growth, high unemployment, slow banking, slower securities, and steady erosion of productive capital stock. In their words:

The bond fund PIMCO popularized the term New Normal to explain the investment environment for the next five years: low growth, high unemployment, slow banking, slower securities, and steady erosion of productive capital stock. In their words:

Global growth will be subdued for a while and unemployment high; a heavy hand of government will be evident in several sectors; the core of the global system will be less cohesive and, with the magnet of the Anglo-Saxon model in retreat, finance will no longer be accorded a preeminent role in post-industrial economies. Moreover, the balance of risk will tilt over time toward higher sovereign risk, growing inflationary expectations and stagflation. …

The result is a prolonged pause, or in some cases, a violent reversal in certain concepts that markets had taken for granted.

McKinsey and others had also used the phrase The New Normal to describe the next few years: less leverage, more government, new protectionism, less consumption and a focus on Asia. They think innovation will continue, and investment in human capital.

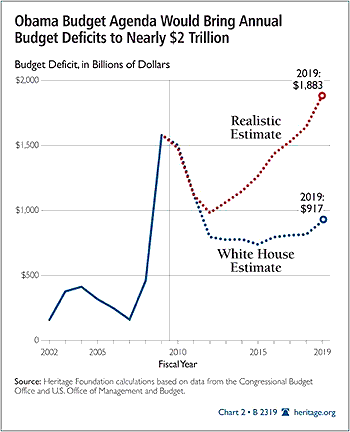

Now John Mauldin in his weekly newsletter takes issue with these projections as too optimistic, dismal though they may seem. He had been a proponent of the Muddle Through economy, one of slack growth (1-2%) and slack employment – kind of like the New Normal. He developed his Muddle Through concept before we had $1T deficits as far as the eye can see. He is even more worried that the optimistic projections underlying the White House estimates (see chart) are unrealistic: they assume 3% growth and a return to 5% unemployment, much better than expected in the New Normal. Hence $2T deficits may be the real New Normal.

The problem he sees is that deficits of this magnitude crowd out private investment, and will continue to suppress consumption in favor of savings (in this case buying Treasuries mostly!). GDP is measured as:

GDP = C + I + G + X

or Consumption + Investment + Government Spending + Net Exports (exports in excess of imports).

The Keynesian plan is for an increase in G to make up for a drop in C. But if that G is funded by huge deficits, it crowds out private investment, and I drops. In order for GDP to continue to grow, we must have an increase in I to fund the private sector. It would have to come from the outside, measured as a positive X (net exports); but for a long time we have run a trade deficit and have had negative X. Will that change? One of the common themes of the New Normal is for capital to leave the US for Asia. This will not create a positive X.

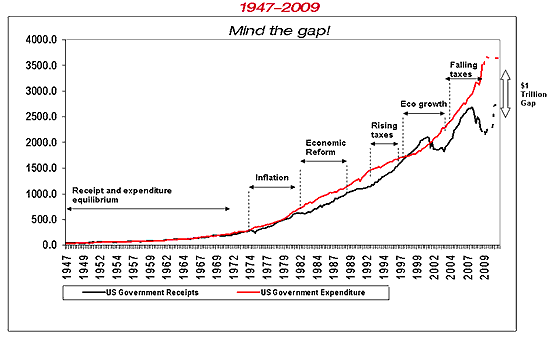

You could take issue with the chart above, as the worst case deficit projections come from the Heritage Organization, a conservative group opposed to Obama. But Société Générale came up with a similar analysis, concluding that we will quickly have a Trillion Dollar Gap with no clear way to fill it. See chart, courtesy The Big Picture.

Now, heretofore the overseas US investments have had returns back in higher than the trade deficits have bled out. This seems likely to change, and also puts pressure on X and how to fund the huge deficits. Right now the US banks are getting deposits at very low rates and buying Treasuries at 2% or higher – such a deal! It enhances the Fed’s QE but does nothing for investment in the private economy.

Picking up on my theme from yesterday, as we starve private investment and send capital overseas, we starve the Golden Goose.

Prognosis: after the inevitable dead-cat bounce in GDP, we should see slow growth with periods of negative growth: The New Normal. Taxes should go up first in 2011 with the Bush cuts expiring and then in 2012 and beyond if any of the bills get passed (the healthcare bills all raise taxes, as does Cap&Trade). Tax increases will further suppress GDP.

In this environment, hard assets and bonds should do better than stocks.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply