The battle for the narrative of the Fed actions in the early-to-mid 2000s continues. The latest salvo comes from a blog post by David Altig of the Atlanta Fed and a Cato Policy Analysis piece by Jagadeesh Gokhale and Peter Van Doren. In both cases the authors absolve the Fed of any wronging doing during the housing boom period. I am not surprised to see Fed cheerleading coming from a Fed insider, but from the CATO institute? These are strange times.

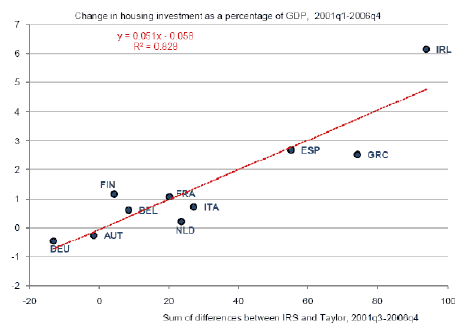

In the first article, Altig conveniently finds a modified form of the Taylor Rule that shows the Fed acted no differently that it had in past 20+ years when monetary policy seemingly worked fine. The first problem with this piece is the obvious problem of data-mining a modified Taylor Rule that justifies ex-post his employers actions. If Altig really wants to be convincing, he needs to explain why the original Taylor Rule, which does show the Fed being unusually accommodative during the housing boom, is suspect and why his modified Taylor Rule is better. As John Taylor has shown, the original Taylor rule goes a long way in explaining this crisis. For example, Taylor shows in the figure below that deviations from the Taylor rule in Europe were closely associated with changes in residential investments during the housing boom there.

Even if Altig could show that his modified Taylor rule makes more sense, there is still the question of whether monetary policy was truly optimal during the previous 20+ years to the housing boom. This was the period of the Great Moderation–a time of reduced macroeconomic volatility–whose appearance has been attributed, in part, to improved monetary policy. As many observers have noted, though, this also was a period of the Fed asymmetrically responding to swings in asset prices. Asset prices were allowed to soar to dizzying heights and always cushioned on the way down with an easing of monetary policy. This behavior by the Fed appears in retrospect to have caused observers to underestimate aggregate risk and become complacent. It also probably contributed to the increased appetite for the debt during this time. To the extent these developments were part of the reason for the decline in macroeconomic volatility, the Great Moderation and the monetary policy behind it becomes less of a success story.

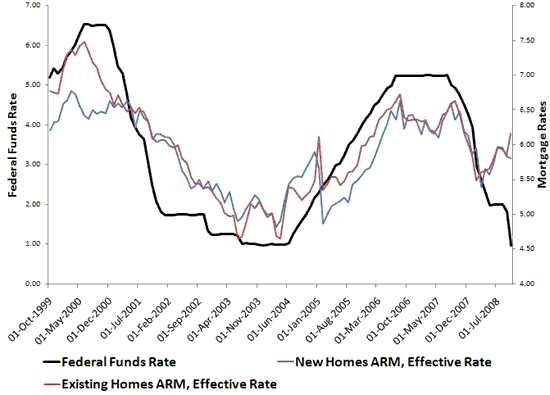

In the second article Gokhale and Van Doren make the following arguments: (1) detecting asset bubbles is a difficult thing to do; (2) even if the Fed could have detected and popped the asset bubble in the housing market in the early-to-mid 2000s it would have done so at the expense of a painful deflation; and (3) the Fed’s ability to reign in home prices was limited. On (1) I agree that responding to an asset bubble after it has formed is challenging. But that is not the the point of most observers who find fault with the Fed during this time. They would say the Fed could have prevented the housing boom from emerging in the first place had monetary policy started tightening before June 2004. On (2) the authors still think the deflationary pressures of that time were the result of a weakened economy. This is simply not the case. As I just recently noted on this blog (here and here), rapid productivity gains were the source of the deflationary pressures, not declining aggregate demand. In fact, by 2003 nominal spending was soaring at a rapid pace. In other words, the deflationary pressures of 2003 were vastly different than the deflationary pressures of 2009. On (3) the authors claim that there was simply no way for the Fed to reign in home prices since the influence of its target federal funds rate on other interest rates declined during the time of the housing boom. While it is true the link between monetary policy and long-term interest rates is more tenuous, the authors argue that even interest rates on ARMs and other subprime-type mortgages were beyond the Fed’s influence. A CATO Policy Briefing by Lawrence H. White, however, provides evidence that supbrime market was in fact very sensitive to the Fed’s action during this time. Below is figure that corroborates White’s work by showing the effective interest rates on ARM mortgages along with the federal funds rate. Is there any doubt?

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply