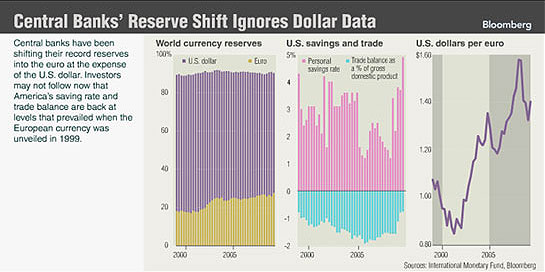

Yesterday the YE$ currency (Yen Euro $Dollar as the reserve basket) hit a milestone: the past three months have seen the Yen/Euro get 63% of new reserves vs the Dollar at 31%, or below even one-third among the three. The US Peso is now down to its lowest level as a reserve currency since the break with gold in 1971 at 62%. While this is not quite the fancy headline “Dollar Loses Reserve Status” it does show that pressure is building on Bernanke to raise rates to support the Dollar.

The Fed’s conundrum can be simply explained (this is a quote from John Mauldin from Mish’s site yesterday):

You cannot continue to run deficits significantly larger than nominal GDP for too long without risking the demise of the economic system. But we are in a deflationary environment, so the Fed can monetize the debt far more than any of us suppose without risking immediate and spiraling inflation.

The mistake we are running is to have huge fiscal stimulus (deficits) alongside huge monetary stimulus.

The concept of monetary stimulus to avoid serious deflation and ease the write-down of excessive debt comes from Irving Fisher’s seminal Debt-Deflation Theory of the Great Depression paper of 1933. He gave a cogent explanation of the events that led to the debacle, and discussed how Hoover almost got it right in the summer of 1932 when he began reflating the currency – we began to emerge from the Depression between May32 and Sep32 – then lost heart during the election and let it come tumbling down. At the time Fisher was the pre-eminent US economist, the Keynes of the US so to speak.

His work is required reading, even with recent revisions. He explained as simply as I have seen why the Depressions of 1929, 1873 and 1837 were different in kind from deep Recessions in 1921, 1893, 1859 and 1820 (and 1981): the Recessions were due to over-production, while the Depressions were due to over-indebtedness. As now.

His remedy is now accepted wisdom: massive liquidity from the central bank is needed to ameliorate deflation and prevent money from being hoarded. Back in the 1930s people may have stuffed bills into mattresses, but today we stuff them into short-term Treasuries. Same effect – the money is not spent nor is it invested (which is also then spent, on new plants and new hires). Hence plopping savings in short-term low-interest notes is the same as taking it out of GDP and stuffing it in mattresses. As now.

Bernanke’s Fed reacted too slowly, and drove US consumers to pay down debt and plunk their savings in safe instruments; but has heroically pumped liquidity since. The dilemma comes not from Bernanke but Obama: the massive Federal deficits to finance stimulus are creating a terribly negative dynamic. I have previously discussed the impotence of fiscal stimulus: rather than reinvigorate the private economy, it acts as short-run life-support.

The worse position to be in is where the deficit grows faster than GDP. This creates a dynamic where the government simply digs a deeper and deeper hole. Right now economic projections even in the V-Shaped recovery have us growing the deficit faster than GDP. Only Obama’s optimistic projections suggest otherwise, and they are not taken seriously. From Judy Shelton in a WSJ op-ed yesterday:

Even with the optimistic economic assumptions implicit in the Obama administration’s budget, it’s a mathematical impossibility to reduce debt if you continue to spend more than you take in. Mr. Obama promises to lower the deficit from its current 9.9% of gross domestic product to an average 4.8% of GDP for the years 2010-2014, and an average 4% of GDP for the years 2015-2019. All of this presupposes no unforeseen expenditures such as a second “stimulus” package or additional costs related to health-care reform. But even if the deficit shrinks as a percentage of GDP, it’s still a deficit. …

The U.S. is thus slated to enter the ranks of those countries—Zimbabwe, Japan, Lebanon, Singapore, Jamaica, Italy—with the highest government debt-to-GDP ratio … .

Sadly, due to our fiscal quagmire, the Federal Reserve may be forced to raise interest rates as a sop to attract foreign capital even if it hurts our domestic economy. Unfortunately, that’s the price of having already succumbed to symbiotic fiscal and monetary policy. If we could forge a genuine commitment to private-sector economic growth by reducing taxes, and at the same time significantly cut future spending, it might be possible to turn things around.

Worse, the maturity of Treasury debts is decreasing, from 6 years in 2000 to 4 years today, and dropping towards 2 years. As Karl Denninger comments, this places Treasury in an untenable position: it has to roll over the whole deficit every four years PLUS tack on new debt to cover the deficit. Why would the maturities decrease? Maybe that is all our trading partners will take, since they are rolling out of the Dollar into the YE$ basket. By reducing their exposure to long-term Treasuries they better prepare to get out if the US Peso continues to fall.

When something cannot go on, it doesn’t. Expect something to break, and soon, and the USD to begin to rise again.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply