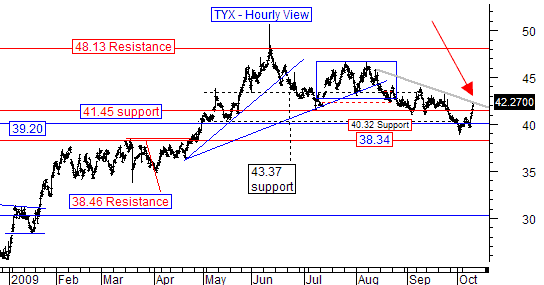

The Long Bond is way up in the past few days, with yields shooting from 3.95% on Oct2 to 4.2% Friday. The yield curve had been flattening, but is now going the other way. See chart from StockTiming. Bond markets are closed today for Columbus Day Fall Weekend Day. Tomorrow should be interesting. Does this sharp change in bond yields reflect local turmoil last week in forex markets, meaning it will settle back down this week, or is it presaging a trend change in the Dollar?

Treasury had a surprisingly poor auction on Friday. Perhaps the CBO long term analyses are causing concern, since they point to fiscal doomsday. Curiously, despite last week’s sneak attack on the Dollar, it came back on Friday. The Dollar is down today except for a collection of Asian Tigers who have been intervening to devalue their currencies (including Japan). My experience with bond markets is they don’t look out that far; instead are driven by the trading environment. That may be about to worsen.

First, central banks are worried over holding the hot potato: too many Dollar holdings when the bottom drops out of it. While central banks are not decreasing USD holdings, they are shifting proportionately away. In effect, central banks are shorting the Dollar. Why?

No one wants to be caught holding too many dollars, and this rising reluctance is increasing pressure on the USD. This is an obvious USD negative, but it is also means that the ECB and the EUR are caught between a rock and a hard place. The capital flows into the EUR have very little to do with any euro area cyclical dynamism..

Second, we seem to be in a swirl of events that may soon change the current market dynamic. Besides Latvia having a failed auction and potentially defaulting, now Romania may collapse tomorrow. Fear of fiscal dominoes is bullish on the Dollar as a safer haven.

Third, the other shoe to soon drop may be China. The Shanghai exchange had been closed for over a week, opened strong Friday and faded today. Nw a report is out that lending in China hit a new low in September. From the report: “Yet the September decline was doubly ominous, as it comes in a time when banks traditionally let the spigot on full blast.”

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply