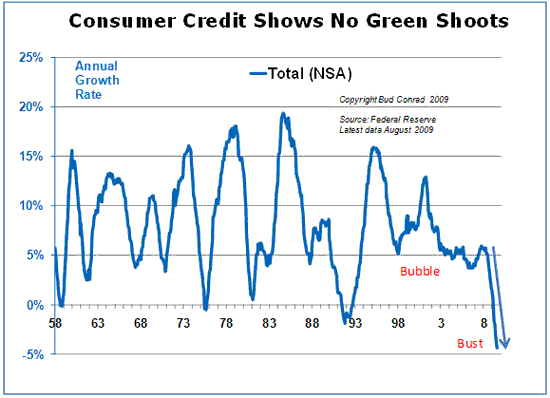

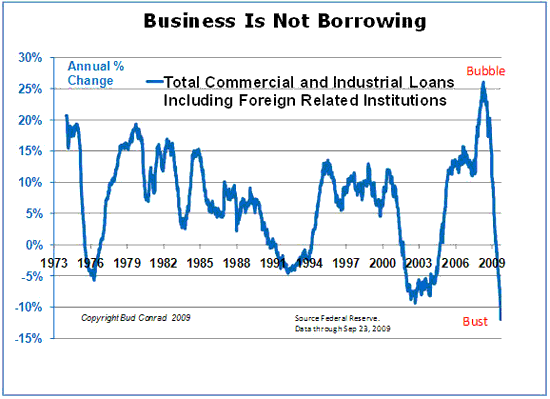

There can be no real recovery without the private sector, and credit is collapsing for consumers and business. These two charts show the businesses are not able to borrow and consumers are not able to get credit. On the consumer side, overall credit is declining at 5%/yr and revolving credit (credit cards) is declining even faster at 8%. Business loans are down 12% yearly, and in the last three months a frightening drop of 19% annualized for total loans and a 28% annualized in commercial loans. This means the credit crunch is accelerating.

One of my investments is living this nightmare. Their sales will triple this year in a bad market for retail products, but they have a difficult time getting a line of credit even when backed by real assets – receivables – and have to pay an effective rate of 15%.

The public looks at the extremely low Treasury interest rates & deposit interest rates, and presumes that businesses can borrow close to them. Instead, normal everyday commercial credit is run up to usurious levels. And almost everyone knows someone who has faced seemingly rapid and arbitrary increases in credit card rates to a stunning 28%. New accounting rules which are supposed to enhance transparency may make consumer credit even harder to get.

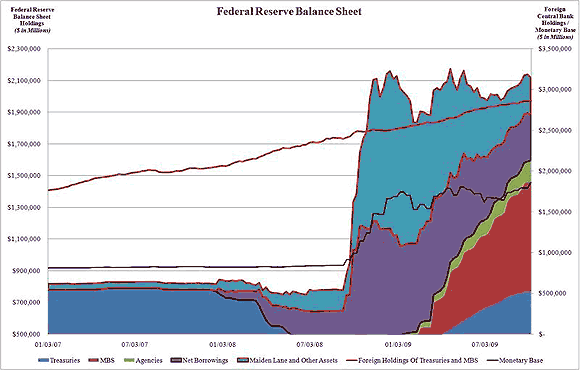

The reason for the worsening crisis is the way the Fed has handled the situation, as described the Run on the Dollar post: by burying the toxic debt inside the Fed, they have postponed the day of reckoning for the banks but have not cured it.

You can see in the chart how much the Fed has buried, inside their Maiden Lane vehicle and using the TALF program. Total bank reserves have hit an all time high.A huge chunk of it (70%) are “non borrowed reserves” which as best as I can figure from the Fed’s gobbleygook are the reserves burined int he Fed. They are not being used for active lending.

This postponement has consequence. The banks have apparently taken their reprieve and used it to speculate in bonds and equities – the current Obama Hope Rally. Yet they are still tightening credit and pulling back on lending because the buried reserves lock up lending capacity. After all, at some point the Fed will swap them back! And then the banks will have a much harder time avoiding insolvency, since these assets will have to be marked down due to their lack of liquidity and the underlying distress of the assets lent against (primarily real estate).

So far the Fed has postponed the necessary write-downs of the first phase of the crisis – primarily subprime and alt A mortgages to people of questionable credit who have since defaulted at very high rates.

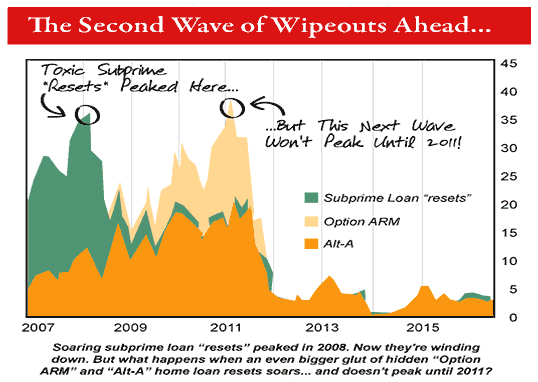

In the next two years the second phase will hit: optionARMs, HELOCs (home equity lines of credit) and commercial REITS, mortgages to borrowers of decent credit. The optionARMs and HELOCs are destined to reset to much higher rates. They were typically designed as a five-year balloon, with the expectation that they would get refinanced within that period. Since real estate values have dropped, this is now a fantasy, since many of these homes are underwater – the mortgage is more than the equity value.

The expectation of course had been for continuing appreciation. HELOCs in particular are distressing, since they were taken out by people of good credit as second or sometimes third mortgages with every intent and capability of covering the payments and repaying the loans. Yet all around them the subprime and no-money-down mortgages drove up the price of housing, both inflating the size of the optionARMs and seducing homeowners into HELOCs.

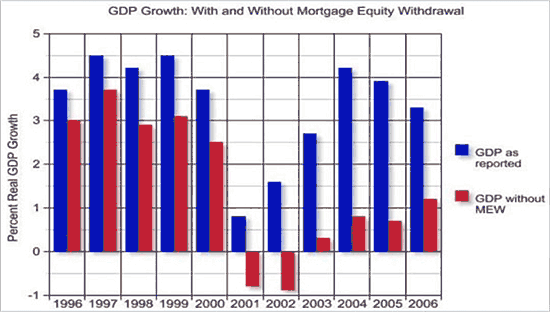

In effect we began using our homes as ATM machines, withdrawing to buy SUVs, HDTVs and vacation property. The MEWs or mortgage equity withdrawals drove the rising GDP during the Greenspan Bubble. This chart shows how different GDP would have looked without MEWs.

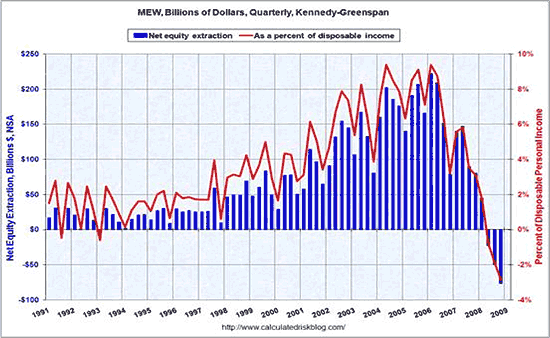

The chart below it shows how the home ATM has run dry.

With MEWs we borrowed beyond our means and spent it on stuff that pulled in future GDP to the present, meaning GDP that would have happened anyway after we earned more to afford it was pulled forward by a debt binge. Just as the mortgages that funded the MEWs have to be repaid or written off, the unearned GDP will have to be given back in the form of lower GDP or actual drops in GDP over the next five years.

The piper has to be paid.

This is what makes this situation so different from a normal recession. Normally when we get ahead of ourselves we have borrowed too much but did it against earnings power (or expected future earnings). In this case we borrowed too much based on asset (home) appreciation, and got way ahead of earnings power. As houses fall, the mortgages get written off, and consumer credit will have to wait until our earnings again catch up.

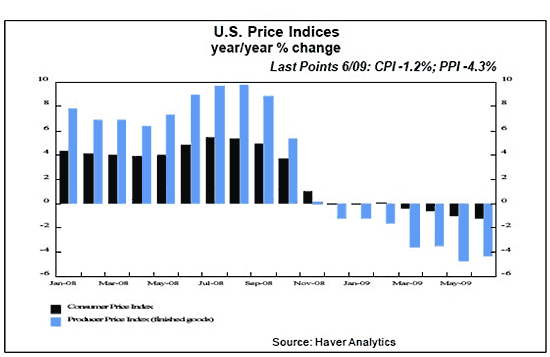

The debt write-offs cause deflation, and as this chart shows we have been in a deflationary period for the past year. But we have had a relatively mild deflation compared with the scale of the excess debt. That is due of course to the Fed hiding the problem. When the second wave of the crisis rolls over, the Fed will be sorely stressed to continue to hide the hot potato.

The Fed has an inordinate fear of deflation. So did Hoover in the 1930s, and his attempts to prop up wages and prices helped turn a bad recession into a long depression.

Ironically they see the situation backwards. As the economy adjusts to excess debt and the pulling forward of GDP, debt write-downs reduce income and layoffs lower wages. With deflation, prices also drop, and less income goes a longer ways. It softens the blow.

Worse, the low interest rates devastate the return on capital. This gives capital an incentive to invest outside the US for higher returns – China? Australia? With a Dollar depreciation risk on top, it pushes investment away even faster. Deflation at least gives protection to the Dollar; but the deeper risk is as the Fed exits a round of deflation then gives way to inflation given the huge overhang of Fed liquidity created to bury the toxic debt.

When might the chickens come home to roost?

The second wave of mortgage problems crests in 2011, and can be postponed a bit.

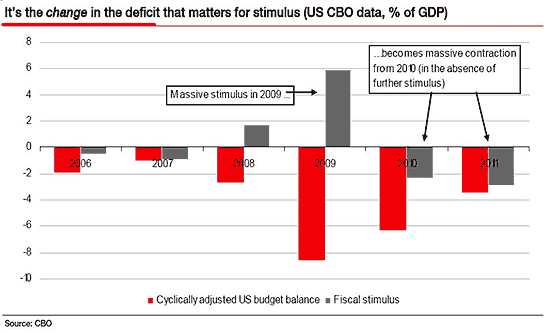

Fiscal policy in 2010, however, may create an additional set of stresses. The Bush tax cuts are set to expire, causing a huge tax increase in the face of a recession. The Stimulus will be past peak in 2010, and decreasing. The net impact will be a huge negative stimulus in 2010. This chart shows the Federal deficit in red and the change in it in grey; and the year after a stimulus it acts as a brake on the economy.

Obama has room for a second stimulus. The deleveraging of total debt has been postponed by the Fed, but not avoided entirely. Private debt is still be written down faster than the increase in the Federal deficit. This gives room for a tax cut in 2010 to counter the expiration of the Bush cuts, and room for a second stimulus.

We can debate the value of stimulus but it would have some short-term impact to at least ameliorate the potentially large negative stimulus next year. And maybe this time they can do a Stimulus bill that acts faster.

The wildcard for the day of reckoning is a series of defaults come out of Europe. The mainline European banks are more over-leveraged than US banks, especially in Eastern Europe. Latvia just had a failed bond auction, and it is ratcheting Sweden. Other countries may follow. including Ireland.

The bottom line remains: a continued if not accelerating decline in commercial and consumer credit.

The longer the Fed tries to postpone the inevitable, the deeper the hole for the private economy to climb out of. All that is left is to try keeping the zombie banks at bay and the economy on some form of government life support until the US creditworthiness begins to seriously weaken.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

The credit crunch is going to be hard for many people. Along with increasing prices there is also the possibility of losing your job and not being able to pay utility bills or a mortgage. In these times of financial hardship and general monetary belt tightening, many people look around to find sources of extra income. Reduce your costs and raise your income – this is the simple sounding answer to the credit crunch problem.

Brilliant summation with some really poignant charts.