The lackluster August employment report clearly defied expectations (including my own) for a strong number to round out the generally positive pattern of recent data. That said, one number does not make a trend, and the monthly change in nonfarm payrolls is notoriously volatile. The underlying pattern of improvement remains in tact, and thus the employment report did not alleviate the need to adjust the Fed’s forward guidance, allow there is a less pressing need to do so at the next meeting. In any event, the days of the “considerable time” language are numbered.

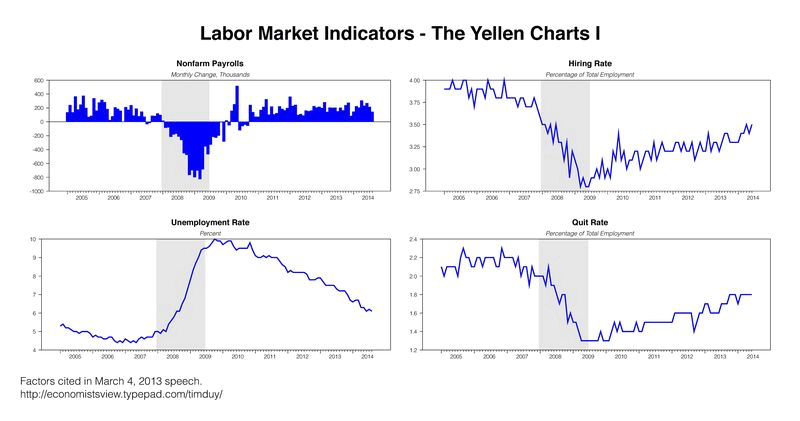

Nonfarm payrolls gained just 142k in August while the unemployment rate ticked back down to 6.1%. In general, the employment report is consistent with steady progress in the context of data that Fed Chair Janet Yellen has identified in the past:

(click to enlarge)

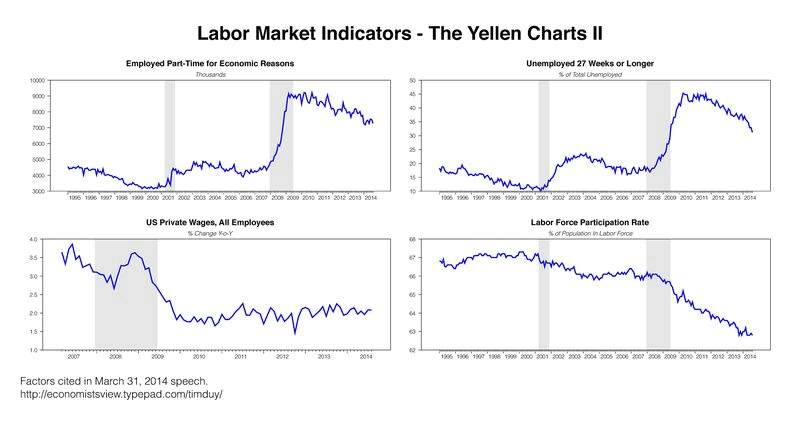

(click to enlarge)

Arguably the only trend that is markedly different is the more rapid decline in long-term unemployment, a positive cyclical indicator. Labor force participation remains subdued, although the Fed increasing views that as a structural issue. Average wage growth remained flat while wages for production workers accelerated slightly to 2.53% over the past year. A postive development to be sure, but too early to declare a sustained trend.

The notable absence of any bad news in the labor report leaves the door open to changing the forward guidance at the next FOMC meeting. As Robin Harding at the Financial Times notes, many Fed officials, including both doves and hawks, have taken issue with the current language, particularly the seemingly calendar dependent “considerable time” phrase. Officials would like to move toward guidance that is more clearly data dependent.

Is a shift in the language likely at the next meeting? Harding is mixed:

Their remarks could mean a move at the September FOMC meeting in 10 days, although there is little consensus yet on new wording, so a shift might have to wait until next month.

The trick is to change the language without suggesting the timing of the first rate hike is necessarily moving forward. The benefit of the next meeting is that it includes updated projections and a press conference. Stable policy expectations in those projections would create a nice opportunity to change the language. Moreover, Yellen would be able to to further explain any changes at that time. This also helps set the stage for the end of asset purchases in October. A shift in the guidance next week has a lot to offer.

A change in the language would also throw some additional light on Yellen’s comments at Jackson Hole. Her typically unabashed defense of labor market slack was missing from her speech, replaced by a much more even-handed evaluation of the data. Was she simply setting the stage for an academic conference, or was she signalling a shift in her convictions? A change in the language at the next meeting would suggest the latter.

Bottom Line: The US economy is moving to a point in the cycle in which monetary policymakers have less certainty about the path of rates. Perhaps they need to be pulled forward, perhaps pushed back. Policymakers will need to be increasingly pragmatic, to use Yellen’s term, when assessing the data. The “considerable time” language is inconsistent with such a pragmatic approach. It is hard to see that such language survives more than another FOMC statement. Seems to be data and policy objections are not the impediments preventing a change in the guidance, but instead the roadblock is the ability to reach agreement on new language in the next ten days.

Leave a Reply