The minutes of the December 2013 FOMC meeting will be released Wednesday. I am looking for divisions within the FOMC on key topics, notably likely timing of the first rate hike, likely pace of rate hikes, and discussion of what follows the Evans rule. I am not so much concerned with the tapering process at this point. In my mind, that is now something of a dead issue. Barring any large shifts in the pace of economic activity, I think the Fed is largely committed to winding down that program this year. And I think that the Fed is likely committed to low interest rates through 2014. It’s in the 2015 policy outlook that the real divisions start to show.

As far as quantitative easing is concerned, I think the Federal Reserve is looking to end the program. Although they have not fully explained the calculus in the background, I think the cost/benefit analysis shifted against asset purchases. Moreover, the markets did not collapse after policymakers pulled the trigger on the taper, and everyone (all right, everyone but Boston Federal Reserve President Eric Rosengren) seems relatively comfortable with the pace at with asset purchases are expected draw to a close. Sure, arguably the hawks would like to see it brought to a close sooner than later, but are really just happy to see a path out, a clear indication that there is no such thing as QEInfinity.

With regards to interest rates in 2014, here again I think the vast majority of FOMC members are comfortable with the idea that short term rates will most likely hold near zero for the remainder of the year. Even if the US economy receives a faster than expected burst of cyclical activity, the still large output gap and high unemployment rate suggest there is room to let the growth engine run on all cylinders for awhile This is especially the case given the inflation numbers.

There is enough uncertainty about inflation, however, that I think the Fed will hesitate to lower the unemployment threshold. Unless they change the threshold, the Evan’s rule becomes defunct in just 0.5 percentage points. I tend to think that the Fed does not want to change the threshold, and would like to let such specific, numerical rules-based guidance die a quiet death. Of course, that leaves as an open question of what would be the nature of any rules based guidance going forward.

This could be a place where fundamental divisions among policymakers would be important. Most policymakers could get on board with Evans rule considering the special circumstances – the ongoing Great Recession – and the reality that a 6.5% threshold was in some sense not likely to be meaningful in the first place. I doubt more than one or two policymakers thought that the Fed would be hiking rates anytime before 6.5%. In effect, it was a promise that was easy to keep. Not changing the threshold, however, suggests they they can’t agree on any other promise would be easy to keep. In any event, I am watching the minutes to see if there is more support for a specific change to the Evan’s rule than I currently expect.

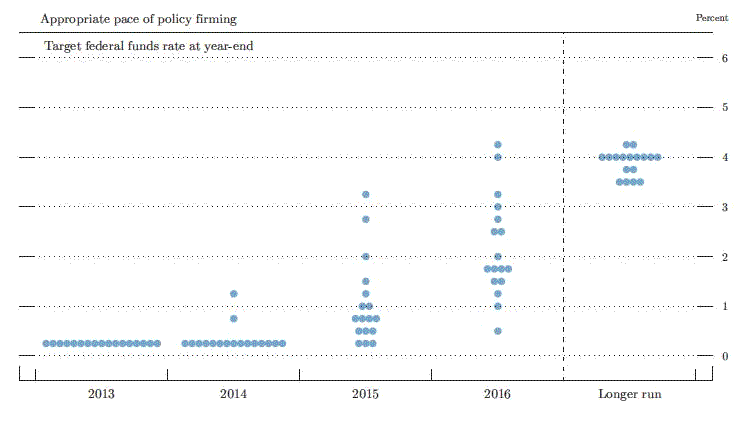

That leaves 2015. Here, I think, we tend to be overlook the wide range of expectations for 2015 (and 2016, for that matter):

(click to enlarge)

Yes, in 2015 there is a weight on the dovish side of the Fed – but even within that side there is a range of 100bp. Which means some relatively dovish policymakers still think a rate hike toward the beginning of 2015 is likely. And 2016 offers an even wider spread of rate expectations – forecasts of the pace of rate hikes vary widely across policymakers. This suggests deep divisions.

But what is the source of these divisions? If the divisions simply represent different economic forecasts, they might not be very interesting. Presumably, as economic forecasts converge so too would the rate forecasts. In other words, as long as most FOMC members are working with roughly the same reaction function, they really won’t be divided when it comes to actually setting policy – they will line up on the dovish or hawkish side as data dictates. So your view of rate policy is driven by your forecast, and how strongly the Fed leans against that view is dependent how closely they believe the incoming data matches that forecast.

More interesting is the possibility that some of the difference represents fundamentally different reaction functions. To be sure, this is already likely the case to some extent, and is visible in the 2014 forecasts. Even more interesting is the possibility that some of the difference is attributable not just to differing reaction functions regarding inflation and unemployment, but to difference opinions regarding the importance of financial stability in the formation of monetary policy. In other words, do some policymakers desire to accelerate the pace of rate increases to step in front of potential financial instabilities that may be brewing?

Such a camp would be expected to include Kansas City Federal Reserve President Esther George and Dallas Federal Reserve President Richard Fisher. Neither of them, however, have sufficient intellectual weight to move the needle. Governor Jeremy Stein, however, is another matter. He is an intellectual force. And while there is a widespread hope that macroprudential regulation is sufficient to address stability concerns, Stein has already shown a willingness to consider using the tools of monetary policy as an alternative:

Nevertheless, as we move forward, I believe it will be important to keep an open mind and avoid adhering to the decoupling philosophy too rigidly. In spite of the caveats I just described, I can imagine situations where it might make sense to enlist monetary policy tools in the pursuit of financial stability….

Importantly:

Second, while monetary policy may not be quite the right tool for the job, it has one important advantage relative to supervision and regulation–namely that it gets in all of the cracks.

Could Stein bring incoming Chair Janet Yellen and others along to accepting a more aggressive policy to prevent the financial instabilities we have seen in recent cycles (assuming he heads in that direction himself)? The presumption is that Yellen will shy away from using the tools of monetary policy to achieve financial stability. Neil Irwin at the Washington Post, however, see this as Yellen’s greatest challenge:

…Yellen confronts an old dilemma, the same one that she and current chairman Ben Bernanke have been wrestling with for the last three years or so. The tools they have to try to pump up growth are deeply flawed and can create dangerous side effects. But the central bank is the only policymaking entity in Washington focused on encouraging growth at all.

So the debate has been this: Do we use the tools in our arsenal, even aware of the risks? Or do we allow growth to underperform its potential, leaving millions of jobless by the wayside when we may just be able to help, out of fear of some theoretical risks of a new credit bubble and ensuing crisis.

The Fed’s answer this past three years — with strong support from Yellen — has been that the unemployment crisis is so severe and the risks from interventionism are small and theoretical enough that, yes, the Fed should employ its full set of tools to try to boost growth. But as financial markets get closer to levels that suggest they are fully valued, and flirt with bubble territory, the cost-benefit analysis may well change.

I don’t know where Yellen’s thoughts will evolve on this topic. What I do know is this: She has been built up as an dove of the highest order. Consequently, I can’t help but think there is only one surprise she could possibly deliver. Since I think it would be virtually impossible for her policy direction to be more dovish than anticipated (the outcome of optimal control-based policy orientation), the only surprise that seems possible is that she is more hawkish than anticipated.

Bottom Line: What I am watching for in the minutes – signs of division. Division on the forecasts themselves will make it hard to agree to a successor to the Evans rule. Divisions on the reaction function will make it even harder. And the possibility that monetary policy could have a role in pouring cold water on financial markets; it is hard to see how they lower the unemployment threshold while keeping that option open. And, of course, I am wary of the opposite as well – maybe they surprise me and lean toward lowering the unemployment threshold soon. There may still be more dovish tricks in the old magic hat after all.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply