The financial media has been fixated on this topic for the past few months. And the market seems to be expecting it. As with all Federal Reserve announcements (or rumors of announcements), the markets will front-run them. Case in point: the yield on the 10 Year bond is up over 60% year-to-date.

Whether the taper is announced or not is of no concern to this sector of the stock market. These stocks, historically, appear to be taper-immune. When rates have risen, they continue charging on. The gains months after a rate hike, believe it or not, continue to stay in the double digits.

Which sector am I referring to?

The small and micro-cap sector. These companies have a total market capitalization below $5 billion. The micro-cap sector in particular includes stocks under $250 million in total market capitalization. How can we expect these smaller companies to perform in a period of rising interest rates?

While past performance doesn’t guarantee future performance, the data is nonetheless interesting. In fact, some of the data provide clues.

What we’d like to see is how smaller stocks performed in a period of rising interest rates. The idea is straightforward. When rates rise, the general wisdom is that stock prices should adjust. Oftentimes this adjustment is to the downside.

Why?

Higher rates mean higher borrowing costs. Adjustable rate loans charge interest based on certain benchmark rates. Oftentimes, this benchmark is the 10 or 30 year US Treasury Bond Yield. A rise in this rate means higher interest expense for current and future borrowers.

This higher borrowing cost has many immediate effects. One of these is lower discretionary income. This is the cash you have left over after paying off any recurring expenses. If a larger chunk of your paycheck is going to pay interest, you will have less to spend on other activities or goods.

This higher borrowing cost also affects the government. If a larger portion of tax revenue is going toward interest, then less will go into the public sector. I’d love to see the government spend (and tax!) less. Many private industries tend to disagree. These companies are heavily dependent on government contracts and subsidies. When these get cut, the stock prices of these companies will fall.

A higher interest rate affects the manufacturers of capital goods as well. Capital goods are goods used for production of other goods. These are often very large purchases — items such as manufacturing equipment or office buildings. Purchasing these large items requires financing. Businesses will be less inclined to invest in these expensive capital goods if the interest rate is higher.

Not only are producers of capital goods affected by a decline in purchases. So are the companies who reduce their purchases of these capital goods.

As an example, think of a car manufacturer. They are considering expanding operations. In order to expand, they need to make these large capital good purchases. If the purchase price goes up due to a rise in interest rates, they will be less likely to make the purchase. So if this company isn’t expanding capacity, how will they grow in the future? Realistically, they probably won’t.

In financial terms, we would call this a reduction in capital expenditures. When companies cut their capital expenditures, or capex, it is generally looked at unfavorably from the investor’s perspective. A company would purchase capital equipment to meet projected future demand. If these investments aren’t being made, it could imply that the management does not see future growth opportunities. This does not bode well for the stock price.

There are other metrics that go into a stock’s valuation.

One of these metrics is a discounted cash flow.

In a discounted cash flow, analysts project future cash flows for years (or decades). Then, they discount the cash flows back to the present. The idea is that the value of a stock or other asset today is what it can produce in the future. Think of rental property. Part of its value comes from the future rental payments. The same goes for stocks and what cash they can generate.

While the cash flow estimates are important, the rate used to discount them is important as well.

Where does an analyst get this rate? Oftentimes, it comes from the US 10 year bond.

All else equal, a higher discount rate equals lower value. The inverse is true as well: the present value will increase if the discount rate is lower. So, in a rising interest rate environment, what would you expect to see? Simply put — lower stock valuations.

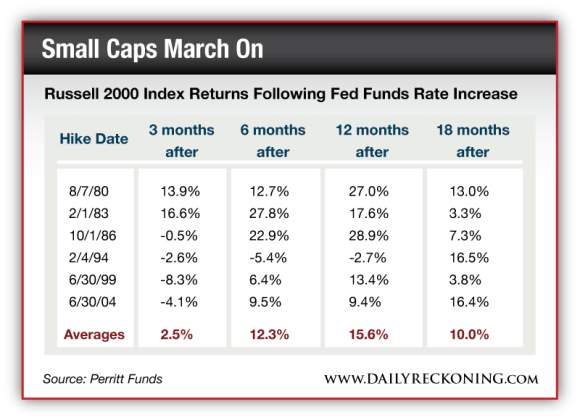

In the small cap sector, however, we see a different result.

The chart below makes a convincing case:

The results are shocking. After a rise in rates begins, small caps continue to march on.

12 months after a rise in rates? The average performance is 15%.

18 months? 10%.

Not bad.

So why could this be?

A few thoughts come to mind.

For one, the smaller companies are not very correlated to the larger caps. Just because the large cap companies are dropping does not necessarily mean that small caps will follow suit to the same degree. This correlation works in both directions.

Second, immunity to macro forces. The smaller stocks aren’t always tied to macroeconomic factors. They tend to focus on a small niche of their respective markets. Many times, this niche is disruptive and cutting-edge. Investors, regardless of what is happening from a top-down perspective, still see value in these little disruptors.

And lastly, size. The smaller companies are just that — smaller. In a rising rate environment, being small can be an asset, and not a liability. Why is that? Making changes in strategy due to higher interest rates as a large cap company is a slow process. Imagine changing the direction of a cruise ship. It’s a gradual bulky shift. Contrast this with smaller companies. They are nimble and able to react much quicker. This quicker reaction time allows the smaller caps to earn outsized returns. Bigger is not always better.

To conclude, the jury still seems to be out as to whether or not we’ll get a taper in bond purchases from the Federal Reserve. Those who say there will be a taper say the economy is recovering. They argue that the housing market has recovered. And, they say, unemployment is down.

Sure, it’s down — down according the government’s own statistics. Never mind the exclusion of a large portion of the population from the overall labor force. And ignore the fact that the gains in employment are very low quality. Working hours are down. Average take home pay is declining. And most employment gains are coming from part-time jobs.

The other side suggests that maybe we’ll get a small taper, but nothing substantial. After all, any “taper” would really mean a reduction in the unprecedented level of monthly bond purchases. Currently, the Fed is buying $85 billion a month in bonds and mortgage backed securities. If this was reduced by, say, $10 billion, it will be lauded as a “taper.”

But is it really? In my opinion, it’s still expansionary and inflationary.

To the small cap sector, the data shows that it doesn’t matter. The positive performance of small caps after a rate-hike makes for a convincing argument. Different investors will recommend different strategies. Incorporating the smaller stocks in your investment portfolio might be something to consider if you fear the taper — or not.

Leave a Reply