Today is a “taper-on” day as financial market participants reacted to the initial claims report by sending Treasury yields up over 2.8% before they settled back to just a few basis points below that mark. If you didn’t believe tapering was coming as early as September, and by December at the latest, the initial claims report was something of a wake-up call. Claims moved decisively lower in the last few weeks:

and are pushing into a range consistent with stronger job growth:

One might respond that other data has been lackluster. Industrial production, for example, is edging forward at an anemic pace:

Retail sales were up in recent months, but like industrial production, given the noticeable slowing trend since late last year, it is difficult to call the growth gangbusters:

Moreover, the Philly Fed report, while not a disaster, disappointed on the downside. On the upside, builder confidence rose in August despite the increase in interest rates. The Fed will interpret this as a sign that higher rates have yet to meaningfully derail the housing recovery.

How might all of these pieces fit together for the Fed? They might decide that there is no evidence the economy is falling off a cliff, thus there is no reason to abandon their baseline forecast. Moreover, declining initial claims will support the contention that labor markets are poised to strengthen further in the months ahead, leading them to discount the softness in the most recent employment report. A solid report for August will be given greater weight than a weak report for July. And when it comes to tapering, progress in reaching “stronger and sustainable” labor markets is the most important benchmark.

What about inflation? St. Louis Federal Reserve President reiterated his belief that the Fed needs to be wary about the inflation numbers. From Bloomberg:

“The committee would not normally remove policy accommodation in an environment where inflation is below target and is projected to remain there,” said Bullard, who votes on policy this year, in prepared remarks in Louisville, Kentucky. The Fed’s inflation goal is 2 percent.

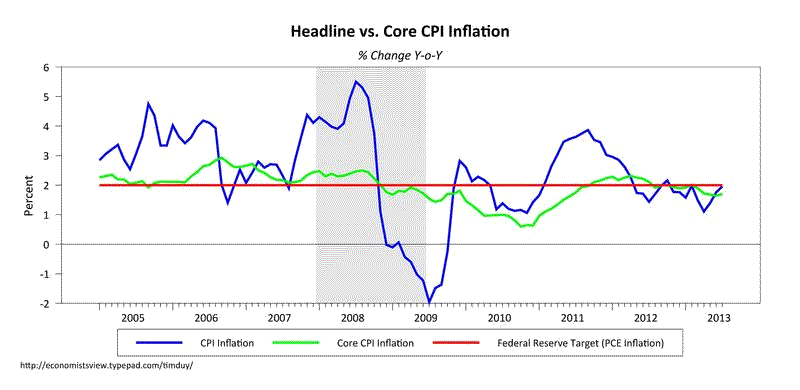

I suppose the key word here is “normally.” We live in anything but “normal” times for central banking. That said, today’s CPI report gives the smallest hint of a possibility that the inflation outlook is set to change:

(click to enlarge)

I wonder if the stage is being set for another Bullard dissent in the near future. One ccould argue that the small uptick in year-over-year core is a sign that inflation is bottoming, consistent with the Fed’s expectations (note I include the Fed’s target for reference). Assuming the PCE numbers are similar, would I hang my hat on this number? Probably not. Would FOMC members, in the context of ongoing declines in initial claims? I wouldn’t bet against it. Remember, though, my bias: I think that fundamentally they are looking to exit asset purchases and refocus attention on the federal funds rates as the first step in policy normalization. Thus I believe that although they might say things like “the decision is data dependent” and “the data is mixed,” they will tend to focus on the positive aspects of the data as justification for moving forward with tapering sooner than later.

Regardless of the date of the tapering, however, the initial claims report reiterated that the writing is on the wall. Tapering is happening, and as long as that idea is still sinking in, I suspect the Federal Reserve is going to have a hard time keeping a lid on interest rates despite their best efforts to push back the timing of the first rate increase. I think there are still market participants who have yet to adjust their expectations that QE is not forever, and that expectation delivered unusually low term premiums. Hence rates remain under pressure until everyone comes to the acceptance that end of asset purchases is arguably a paradigm shift.

And, speaking of paradigm shifts, note that long-time deflationist David Rosenberg is changing his tune. Via Joe Weisenthal:

it’s VERY strongly worth noting that David Rosenberg has written a note and slide dek[sic] today (which we published at Business Insider) wherein he departs from the deflation camp.

Are we at the low water mark for inflation? Maybe, and if the Fed even suspects this is the case, they will be even more eager to end asset purchases and normalize policy.

Bottom Line: The realization continues to grow that whether it is September or October or December, the end of asset purchases is now in sight.

Leave a Reply