SMACKDOWN WEEK continues! I know its been more than a week, but SMACKDOWN Fortnight doesn’t have the name ring.

MORE BULLISH: INFLATION

This one is a little strange, because what exactly does bullish on inflation mean? What I mean is that inflation will remain low, probably below the Fed’s so-called “comfort zone” for at least a year. I don’t know whether you want to call it bullish or bearish since my view poses a significant risk of dangerous deflation.

Anyway, you can see my basic argument against inflation from the last SMACKDOWN. Instead of rehashing all that, I thought it would be more interesting to talk about what might push inflation the wrong way. Specifically, what I’m looking at to indicate that inflation is starting to become a problem.

First, let’s talk about what we mean by inflation. I’m talking about consumer inflation that rises significantly above the Fed’s comfort level of 1-2% on Core PCE. I don’t want to get into the whole inflation vs. cost of living debate yet again. Suffice to say I’m concerned with monetary inflation, not increases in prices of particular goods categories.

So you ask yourself, where does inflation come from?

Ultimately it has to come from consumers spending money. In the too many dollars chasing too few goods equation, someone has to be chasing. As I’ve written before, if Ben Bernanke just went out and doubled the money supply, but no one actually spent the money, there is no “dollars chasing” only “dollars.”

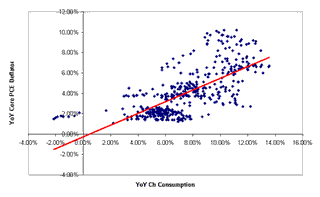

The chart below shows Core PCE deflator vs. the year-over-year change in consumer expenditures. The chart covers every monthly observation (of the 12-month change) since 1969.

Not surprisingly there is a strong correlation here: 0.82. I’ve drawn a fitted trend line, just notice there are exactly 8 observations where consumption growth is negative. Its the last 8 months! To be fair, I’m doing year-over-year numbers to take out some of the month-by-month noise, but the point stands. We’re entering the first outright decline in consumer spending in 40 years.

There are those that talk about the Fed creating another bubble by keeping money easy. That risk exists for sure. But the bubble can only form in a place where money is flowing. Where is money flowing? To a large degree, its into “savings.”

Could there be a bubble in savings? Perhaps. Some think that the excess liquidity is flowing into risk assets, stoking another bubble. But this “savings” isn’t flowing into brokerage accounts so much as its flowing into money markets and paying down debt. 4Q 2008 and 1Q 2009 marked the only outright declines in household indebtedness since 1952! Can there be a bubble in debt repayment?

Our current situation and current policies shouldn’t result in inflation if the easy money is removed in time. I think there is a much greater risk of premature tightening of policy and thus creation of a double dip recession. But more likely we’ll see a very tepid recovery (maybe after an inventory bounce), a recovery not strong enough to stoke inflation.

What worries me is Fed independence. The re-appointment of Ben Bernanke is a huge positive on that front. Obama could have set a new precedent, than the Fed Chair was basically like any cabinet position and every new president gets a new Fed Chief. That would have obviously made the position much more political. But there… off in the distance… you can hear those ominous french horns of fate playing, like Luke looking out onto the twin sunsets…

Recently Ron Paul (who I’m normally 100% behind) said he would get a vote on new requirements for audits of the Fed. Even he says that Congress doesn’t want to interfere with monetary policy, but we all know its a slippery slope. Maybe today’s Congress understands that monetary policy should be apolitical and only wants audits after a considerable lag. Tomorrow those lags are smaller. Then the timing of the audits suddenly coincides with FOMC meetings. Then the FOMC needs to seek “advice and consent…”

MORE BEARISH: THE DOLLAR

Be forewarned that I am not a currency trader. I don’t have a strong opinion about any particular USD/EUR or JPY level as “right.” I am steeped in basic macroeconomics: a currency’s value should reflect two basic fundamentals. Relative inflation and relative investment opportunity. The later should reflect both overall economic growth as well as prevailing interest rates.

So we look at the U.S. versus the rest of the world on those three points: relative inflation, relative interest rates, and relative growth. Worth noting that all these things are inter-related, and that the direction of each from here will be more important than the current level.

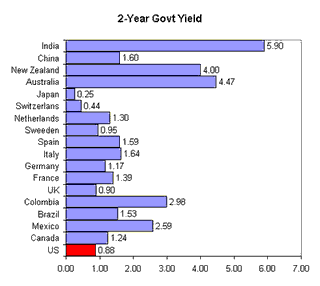

On interest rates, and normally its assumed short-term interest rates matter most, so here are two-year government rates around the world.

You can see that the U.S. is among the lowest worldwide. To the extent that this is reflective of Fed policy, its obviously dollar negative.

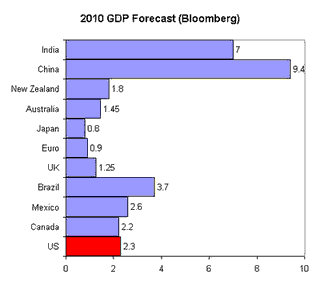

Next I have GDP forecasts for 2010.

The U.S. shows up pretty well on this list. Basically among industrialized nations, the U.S. is expected to grow the fastest in 2010. So that’s somewhat of a dollar positive. However, I believe the main reason why the U.S. is expected to grow faster than the Euro zone is because of more accommodate monetary policy here in the U.S. In other words, we may get more growth, but we’ll also get more inflation.

That’s not contrary to what I wrote above. I expect the Fed’s accommodation to successfully create inflation in the 1% area. Compare this to the Eurozone, where Trichet and company are much more hawkish. I doubt they get to 1%, and I really think deflation is a strong possibility. I think Trichet is making a policy mistake, but regardless it will help the Euro strength. Japan’s problems with inflation are well-documented and thus well-priced into the currency markets.

Anyway, so growth may be a positive for the dollar, but interest rates and inflation are negatives, and I think all that adds up to a weaker dollar.

A related topic is, of course, foreign support for the U.S. bond market. A foreign withdrawal from the bond market could precipitate a dollar collapse. That is something I will address in my next post!

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply