The doom-loop between banks and the national governments played a dominant role in the Eurozone crisis for Ireland and Cyprus. A Eurozone banking union is usually viewed as the solution. This column argues that the doom-loop cannot be undone as long as banks hold oversized amounts of their government’s debt. A simple solution would be to apply the general rule that banks are prohibited from holding more than a quarter of their capital in government bonds of any single sovereign.

The purpose of the proposed banking union is to de-link banks from their sovereigns.

- Putting the ECB in charge of supervision and creating a common resolution mechanism should help.

But this is not enough.

- European banks hold too much government debt of their own governments to really sever the sovereign-bank link.

Until the link is broken, the Eurozone will continue to be vulnerable to disruptive, self-reinforcing feedbacks of the type that brought the Eurozone to the brink of collapse in 2011-12.

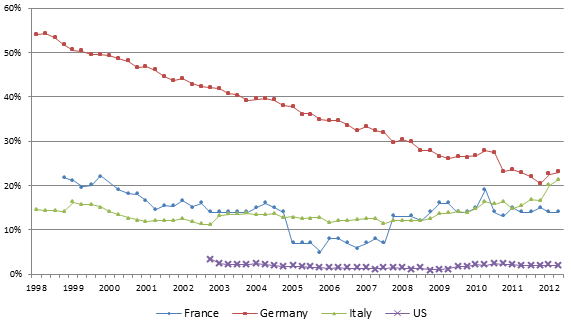

Data on share of own-government debt in bank holdings

The concentration of public debt on bank balance sheets is not just a result of the euro crisis (Figure 1). The numbers show that French and Italian banks always held a considerable fraction of total public debt. The data for Germany are surprising. They show that in the not-so-distant past more than one half of the country’s total national debt was held by German banks. The German banking system has diversified its holdings of government debt only since the creation of the euro.

Figure 1. (National) government debt held by domestic banks in France, Germany, Italy and the US (% of total)

Source: Agence France Trésor, Bundesbank, Bank of Italy and FED.

Why do banks hold so much government debt?

The answer is simple – regulators have made it attractive for them to hold such debt.

- Banks do not have to hold any capital against their holdings of government debt.

Banks hold capital against their investments only if regulators assign a risk weight to this investment. But the risk weight is zero on sovereign debt. This assumption that government debt is riskless permeates all banking regulation and thus contributes indirectly in many ways to induce banks to hold government debt. It is difficult to understand why this assumption has not been changed after the ‘PSI’ (private-sector involvement) operation in Greece showed that banks can lose money on their holdings of Eurozone sovereign bonds. Moreover, PSI is now also official policy since the ESM Treaty foresees explicitly the possibility of a haircut on public debt if a debt sustainability analysis shows that the country cannot service its debt in full. There is thus no reason to continue with the regulatory fiction that sovereign debt is always riskless.1

Introducing risk weights for government debt will not be enough to prevent a crisis because of the ‘lumpiness’ of sovereign risk. Experience has shown that sovereign defaults are rare events, but the losses are typically very large (above 50%) when default does materialise. In many peripheral countries, banks hold sovereign debt equal to (or greater than) their total capital. Even with a risk weight of 100%, these banks would only have sufficient capital reserves to cover losses of 8%.

- Large banks are allowed to cherry-pick regulatory approaches.

There is an obscure but very important clause: ‘Permanent Partial Exemption’. This term refers to one of the many wrinkles in the way the EU has implemented the Basel agreements on banking regulation in its own capital requirements Directive (CRD). In essence large banks are allowed to use their own models to assess the riskiness of their own assets. But when these models would signal that government debt has become risky (for example because the debt has become unsustainable or CDS spreads signal risk), the normal risk models are put aside in favour of the general presumption that government debt can never be risky.

In essence banks can cherry pick. Most large banks use their internal risk models to calculate the riskiness of their lending to households, the corporate sector and their other assets. By doing so they can generally arrive at a lower level of capital requirement than under the so-called standardised approach in which all lending falls in certain risk classes determined by ratings levels. However, these internal risk models are put aside in the case of government debt. Given this, there is little wonder that European banks lack the capital to weather a sovereign debt crisis (which by regulatory definition should not be possible).

- Liquidity requirements favour government bonds.

Another reason why banks hold large amounts of government debt on their balance sheets is that they have to hold a certain amount of ‘liquid’ and safe assets. Until recently, only government bonds were recognised as liquid. However, experience over the last few years has shown that at times even government bonds can become illiquid. Forcing banks to hold large amounts of government bonds might make sense if it were true that that this is the only class of liquid and safe assets, but this is manifestly no longer true.

Fortunately the latest version of the so-called liquidity cover ratio (LCR) allows banks to also hold other assets to satisfy the requirement of the LCR, whose purpose is to ensure that a bank can always offset potential outflows of funds by selling liquid assets. This incentive to hold government debt might thus be somewhat diminished.

- There is no limit on the concentration of sovereign risk.

The most basic principle of finance is reducing risk through diversification. The need to diversify risk is the reason why all regulated investors (banks, insurance companies, investment funds, pension funds) have to limit their exposure to any single counterparty to a fraction of their total investment or capital (for banks). For banks, the limit on the exposure to any one borrower is 25% of their capital, but this limit does not apply to sovereign debt. The logic of this exemption was simple: since there was thought to be no risk in sovereign debt, there was no reason to put any limits on its concentration. The result of this lack of exposure limits has been that banks in the periphery have too much debt of their own government on their balance sheets which has greatly contributed to the deadly feedback loop between sovereigns and banks.

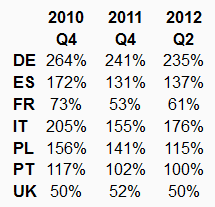

Table 1 below shows the degree of ‘domestic leverage’ of the systemically important banks in major Eurozone countries that were subject to the EBA stress tests (and soon will be supervised by the ECB). It is apparent that in most countries the domestic banking system would not survive a Greek-style ‘haircut’ on public debt. (In the context of the PSI operation of March 2012, holders of Greek bonds had to accept a nominal haircut of over 50%, and on a mark-to-market basis the haircut was over 80%. It is apparent that no bank that has a sovereign exposure worth over 100% of its capital would survive such a loss.)

Table 1. Domestic sovereign debt leverage (sovereign exposure/capital)

Source: CEPS database.

All four elements could and should be changed.

Concluding remarks

The belief that government debt is riskless is a fundamental assumption in banking regulation. In Europe this has induced banks to hold large amounts of government debt and, even worse, to concentrate their holdings on their own sovereign – thus ensuring that a sovereign-debt crisis also becomes a banking crisis.

The key aspect for the stability of the euro and its banking system is the concentration of bank holdings of their own sovereign. If this could be changed, the banking system would become much more resistant to sovereign-debt problems.

- A simple solution would be to apply the general rule that banks are prohibited from holding more than 25% of their capital in government bonds of any single sovereign.

This rule could be applied only to new investment during a transition period so that it would not force any abrupt selling of the existing holdings.

The treatment of government debt in banking regulation is one of those dogs that did not bark. The EU has recently completed a wide-ranging overhaul of its banking regulation framework in the context of the renewal of the capital requirements Directive (CRDIV). The regulatory treatment of sovereign debt was not even discussed in this context. Why? Simply because governments want to maintain a source of demand for their own bonds.

But this self-serving treatment of government debt in banking regulation is short-sighted because it leads to a situation in which Eurozone banks hold a large proportion of government debt – much more than in the US. This is dangerous given that banks are highly leveraged and that sovereign debt is inherently subject to default risk within the Eurozone. For financial-stability reasons, it would thus be preferable if a higher proportion of government debt were held by unleveraged investors, e.g. directly by households or via investment funds. But this would of course reduce the income of the banks. The unholy alliance of short-sighted finance ministers and bankers interested in keeping their business will be very costly because it perpetuates the negative feedback loops between banks and sovereigns.

References

•Acharya, Viral V and Sascha Steffen (2012), “The ‘Greatest’ Carry Trade Ever? Understanding Eurozone Bank Risks”, University of Virginia, Charlottesville, VA; 18 November.

•BIS (2013), “Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring tools” Bank for International Settlements, January, Basel.

•De Grauwe, Paul (2011), “Governance of a Fragile Eurozone”, CEPS Working Document No. 346, CEPS, Brussels, May.

•Kopf, Christian (2011), “Restoring financial stability in the Eurozone”, CEPS Policy Brief, CEPS, Brussels, March.

•Gros, Daniel (2013), “Banking Union with a Sovereign Virus The self-serving regulatory treatment of sovereign debt in the Eurozone”, CEPS Policy Brief No. 289, CEPS, Brussels, 27 March.

__________

1 The standard objection to risk weights on sovereign debt is that they contradict fundamental principles on which the Basel capital adequacy regime is based. It is indeed true that all Basel accords stipulated that banks do not necessarily have to hold any capital against claims on their own government (and in their own currency) because government debt is regarded as riskless if it is the national currency.

The rationale for zero risk weights under normal conditions (i.e. the country has its own national currency) is clear: when the country has its own currency the government can, in extremis, always order the central bank to print enough money to be able to service its debts. But as emphasised by (Kopf 2011 and de Grauwe 2011), in the Eurozone no individual debtor government has any authority over the creation of money. The ECB is actually forbidden to provide monetary financing to any government, or even the EU authorities. When monetary and fiscal authorities are separate entities as in the Eurozone, default risk on sovereign debt is not zero. This was the intellectual mistake made when the Basel rules were transcribed into EU law (i.e. the capital requirements Directive).

Leave a Reply