Thanks to the life support of $12 trillion and 515 rate cuts by the world’s central banks since March 2009, the global economy’s heart is beginning to beat again. As the market senses a robust economic recovery is underway, expectations are climbing that this growth will continue. Even the Federal Reserve has hinted that it may taper quantitative easing because of the improved economic situation. As a result, interest rates are increasing.

Europe was the lone wild card, but following Germany’s change of heart away from austerity, a positive outlook for growth, and therefore, rates, is rising in that area of the world as well.

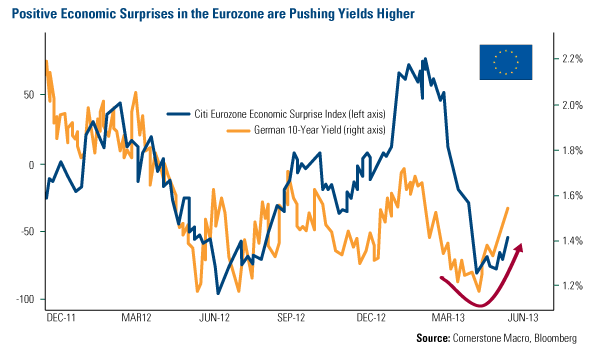

In the chart below, you can see the close correlation between the eurozone’s positive economic surprises and bond yields. The Citi Eurozone Economic Surprise Index, which compares economic data to expectations, has improved, bouncing from a low in April. At the same time, the yield on Germany’s 10-year bond has also begun to increase.

Given this rising interest rate environment, we wondered how gold, oil, and commodities, as well as energy and materials stocks have historically performed. With a hot economy, will we see hot commodities?

We found some compelling results for resource investors.

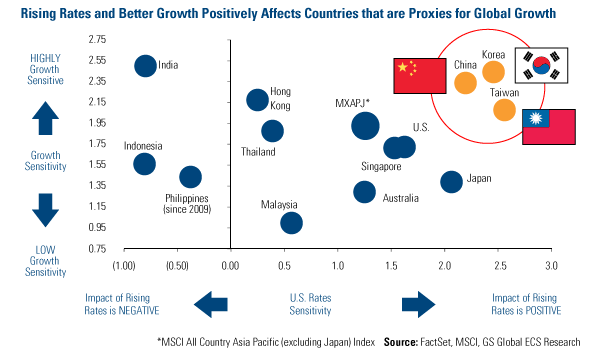

Goldman Sachs’ historical playbook finds that “higher rates are ok for Asian equities.” Since 1990, there were 35 periods in which U.S. rates rose 50 basis points or more, and 75 percent of the time, the MSCI All Country Asia Pacific (excluding Japan) Index climbed higher, says Goldman.

The research firm plotted Asian countries as well as Australia according to their growth sensitivity compared to their U.S. rate sensitivity. You can see that the index tends to be positively impacted by rising rates in the U.S. and is relatively growth sensitive.

Across Asia, China, Korea and Taiwan—proxies for global growth—are the most positively affected by rising rates. These three countries are also the highest growth-sensitive areas of the world. That makes today’s situation of economic growth with rising rates a powerful combination for commodity investors. When economies such as China and Korea are growing, their use of commodities tends to expand as well.

On the opposite end of the spectrum, countries such as India, Indonesia and the Philippines are negatively impacted by rising rates, as their economies are domestic driven and do not benefit from rising growth expectations in the U.S.

The Key is to Take Action Now

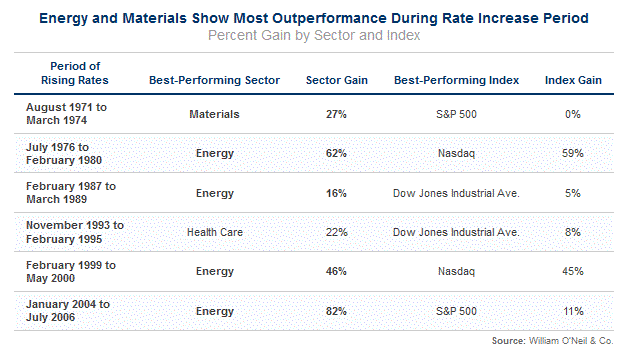

Don’t wait for the Fed to officially raise rates, as research shows that investors get the most benefit from materials and energy stocks by getting in now. Take a look at William O’Neil & Co.’s table below, which illustrates how critical it was to be invested in commodities before rates increased.

The firm looked at individual sectors, such as retail, technology, and utilities, along with broad indices, including the S&P 500 Index, the Dow Jones Industrial Average and the Nasdaq over four decades. It calculated the gains not only received during the period of the rate increases, but also six months prior to the initiation of rate increases.

In every instance, the energy sector performed “extremely well during these periods,” with basic materials also outperforming, says William O’Neil.

A Rerun of That ‘70s Show?

Looking ahead, if the economy starts to experience runaway inflation, history shows it makes sense to hold real assets. A decade ago, Investment Advisers Stephen Leeb and Donna Leeb wrote a very informative book on how to profit from the “Turbulent Post-Technology Market Boom.” The book, Defying the Market, discussed how to protect against deflationary and inflationary scares, comparing investment ideas that were likely novel to many people in their day, including energy, food, gold, and small-cap stocks.

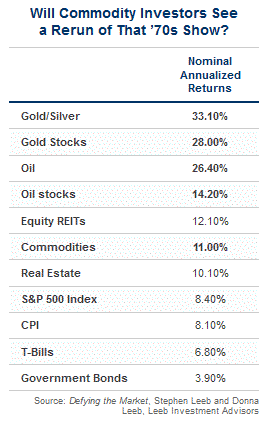

One table listed the performance of these investments during an earlier era when Americans faced high inflation—the 1970s.

One table listed the performance of these investments during an earlier era when Americans faced high inflation—the 1970s.

In that decade, gold, silver and oil outperformed many other areas of the market. Gold stocks rose 28 percent on an annualized basis and oil companies grew 14 percent. The S&P 500 Index, on the other hand, grew 8.4 percent on a nominal basis. After factoring in sky-high inflation of 8.10 percent, gold and oil still added significant real returns. The real return of the overall stock market, on the other hand, was nearly zero.

“Stocks leveraged to growth, such as the oils and oil drillers, did splendidly. But the big-cap stocks [i.e. the general market] … were complete duds,” wrote the Leebs.

While it is still too early to tell whether investors will see “That ‘70s Show” again, one valid consideration to protect from inflationary measures is an allocation to real assets like commodities.

An investment that covers all the commodity bases is the Global Resources Fund (PSPFX), which selects commodity stocks across 10 diverse industries, including oil services, exploration and production companies, as well as precious metals stocks. We believe this approach offers investors the possibility for better growth with lower volatility.

Leave a Reply