Conditions have changed since January, and we might expect some additional stimulus from the Fed at the next FOMC meeting.

Many observers have wondered why the Fed seems to be completely disregarding its objective to try to maintain full employment. If the Fed’s long-run targets call for an inflation rate of 2% and an unemployment rate below 6%, then any balancing of the tradeoff between the two objectives would imply we’d want to see an inflation rate above 2% as long as unemployment remains as high as it presently is.

Part of the answer, as noted on Friday by Federal Reserve Bank of Atlanta President Dennis Lockhart, may be concerns that the stimulus options currently available to the Fed raise their own set of risks. Lockhart also discussed the conclusion of some observers that if the U.S. economy were as far below its current potential as some observers claim, it’s puzzling why we’ve continued to see a low but persistently positive rate of inflation over the last 3 years. The failure of inflation to decline over this period might be taken by some as one indicator that there actually is not that much potential for the Fed to achieve significant additional improvements in the unemployment rate.

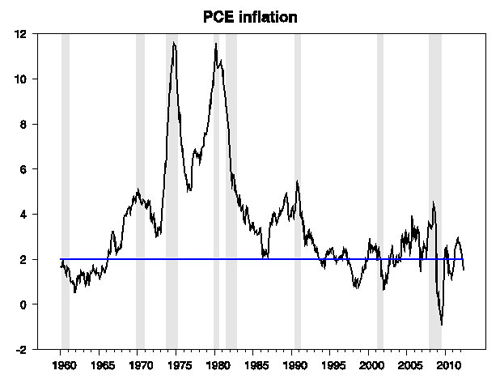

Insofar as this has been a concern, the abatement in inflation over the last few months gives a renewed reason for the Fed to act. The most recently reported year-over-year change in the PCE deflator, the Fed’s favored measure of inflation, came in at only 1.5% in the latest release. Thus, even if the Fed didn’t care at all about unemployment, its announced objective in terms of inflation would suggest the desirability of further easing on grounds of that objective alone.

Year-over-year percent change in monthly PCE deflator, 1960:M1 to 2012:M5. Horizontal line at 2.0%. Data source: FRED

There’s another reason why a lower inflation rate is relevant for anticipating the Fed’s next step. While the hawks on the FOMC are generally perceived as wanting to avoid inflation, they also are committed to avoiding deflation. Although we may disagree about how much a higher inflation rate might benefit the economy, there is much wider agreement that deflation would make our problems worse and is something the Fed can and should avoid.

And the Fed’s policymakers seem to have taken note of the recent abatement of inflation. At the January 25 FOMC meeting the highest anticipated inflation rate for 2012 reported for any FOMC participant was 2.5%. By contrast, after the most recent meeting, the highest reported rate was 2.0%. There now seems to be essential unanimity within the FOMC that inflation is coming in below their target at the same time that a lower unemployment rate is achievable. That means that any way you slice this cake, you’d want to see some additional stimulus.

FRB Atlanta President Lockhart summarized the situation this way:

my support for the current stance of policy rests on a forecast that sees a step-up of output and employment growth by year-end and into 2013. If the economy continues on the track indicated by the most recent incoming data and information, that forecast will become untenable, as will the policy premises underlying it.

Or, to wipe away a little of the Fedspeak, if things don’t improve quickly, Lockhart thinks the Fed needs to do more. And here’s Bill McBride’s take-away:

In the press conference [on June 20], Bernanke made it clear that further accommodation is very likely if employment indicators don’t improve soon. He also pointed out that the Fed can’t do any more “twisting” because of the lack of short duration securities.

And that strongly suggests QE3 following the two day meeting ending August 1st.

I say, don’t bet against the Fed. And for sure don’t bet against Bill McBride.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply