Gasoline prices (in case you’ve been hiding in a cave and didn’t know) have been on something of a roller coaster the last few years. And it looks as though we’re climbing back up another hill at the moment. How much are the recent increases in gas prices likely to weigh down American consumers?

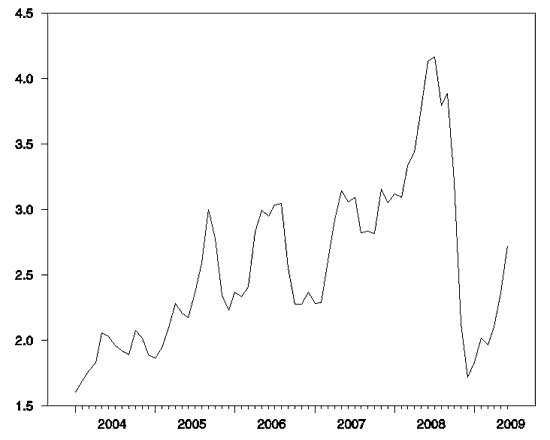

U.S. average retail gasoline price, in dollars per gallon, plotted monthly using the data from the middle week of the month, January 2004 to June 2009. Data source: EIA.

Up until the fall of 2008, consumer sentiment had been closely following that roller coaster, with a sharp plunge in consumer sentiment accompanying the spiking gas prices associated with Hurricane Katrina in 2005, a second, broader drop in sentiment accompanying the second, broader bump in gasoline prices in 2006, and then a significant sustained decline in consumer sentiment as gasoline prices began their remarkable rise over 2007-08. The burden on consumers from that last run-up was in my opinion a key factor that precipitated the initial economic downturn over 2007:Q4 to 2008:Q3. The path of consumer sentiment is plotted as the solid line in the figure below. I’ve also plotted gas prices on an inverse scale (the dashed line in the picture below) in order to highlight visually the negative relation between sentiment and gas prices. The dashed line was calculated as 22/P for P the gasoline price in dollars per gallon, which you could interpret as how many miles you could drive for every dollar you spent on gasoline if you get 22 miles to the gallon.

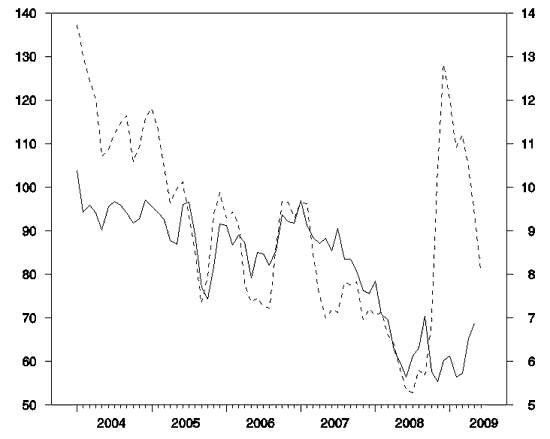

Consumer sentiment versus miles per dollar. Solid line (left scale): Reuters/Michigan index of consumer sentiment, from FRED and MarketWatch. Dashed line (right scale): miles per dollar spent on gasoline, calculated as 22 divided by the price from the previous figure.

That strong relation between gas prices and consumer sentiment continued as the falling gasoline prices (or rising miles per dollar) between June and September 2008 lifted consumer sentiment back up. However, the subsequent financial scares and credit problems in the fall introduced a very dramatic new dynamic, causing consumer sentiment to drop back down to the June 2008 lows by November despite plummeting gas prices.

So how should we assess the likely consequences of the fact that gas prices have now come back up significantly from their lows of December? The Edelstein-Kilian regressions employed in my paper from a recent conference at the Brookings Institution imply that a 20% increase in energy prices would historically be followed within 2 months by a 15-point drop in consumer sentiment and a 1.4% decline (relative to trend) in real consumption spending. From that perspective, the 46% (logarithmic) increase in (seasonally unadjusted) gasoline prices since December is quite worrisome.

On the other hand, since those December prices were 88% (logarithmically) below the July 2008 peak, consumers should have been giddy in December and still be significantly more sanguine now than they had been last summer, if the only thing on their mind was the price of gasoline.

Only problem is, consumers were anything but giddy in December. Credit and employment challenges have weighed far more heavily than gas prices over the last 9 months, and are presumably far more important than gas prices for determining what happens over the next few months as well.

But whatever may come next on the credit front or for unemployment, the impressive spring spike in energy prices can not be a welcome development for American consumers.

Gasoline Prices and Consumer Sentiment

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply