The reflation trade is on, so on, baby, kick-started by Don Kohn’s suggestion last night that the output gap is wider than the Grand Canyon and another wave of better than expected earnings, led by Intel (NASDAQ:INTC) after last night’s close. JP Morgan (NYSE:JPM) announces at noon London today, kicking off a busy week of kleptocrats’ banks’ earnings.

But while equities are performing strongly, the real story of the day thus far has once again been the dollar. Not only has EUR/USD made a new high for the year above 1.49, but now even oil has broken out, suggesting that a sinking dollar lifts all boats.

While the dollar is traditionally weak in Q4 as FX reserve managers top up their non-US$ holdings (a trend that should be in full effect this year as Voldy and co. scoop up zillions in fresh reserves via intervention), it’s hard to shake the feeling that the Obama administration is secretly delighted with the demis of the buck. To date, there have been no meaningful adverse effects of a dollar decline- Treasury auctions are still going swimmingly, and oil prices have been in a range for the past several months.

Sure, they’ve had to field the odd angry phone call from the Europeans, but that’s pretty small potatoes to date. Still…it’s not hard to see a scenario where the Eurogroup (and potentially the ECB) start hammering more forcefully on the Americans about dollar weakness and the Chinese about euro strength.

Yet while Macro Man has considerable sympathy for the view that China needs to quit taking the piss when it comes to its and others’ currencies, he finds it less easy to swallow the Europeans’ viewpoint vis-a-vis the dollar. A few charts will explain why.

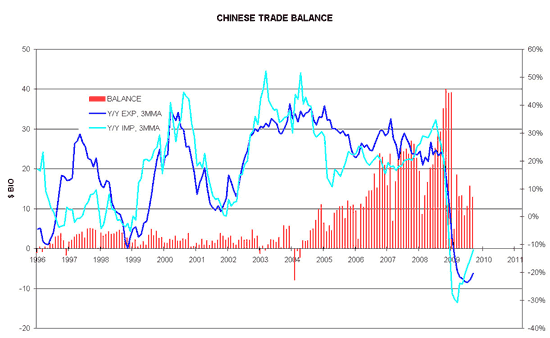

The first chart below shows China’s trade data, the September edition of which was released overnight. Gratifyingly for the green shoots brigade, imports were substantially stronger than expected, propelling a modestly lower trade surplus. Observe, however, how the proud owner of the world’s largest trade surplus managed to safeguard its monthly positive trade reading throughout the entire financial crisis- helped, no doubt, by the decision to arrest a strengthening of the RMB versus the USD last July.

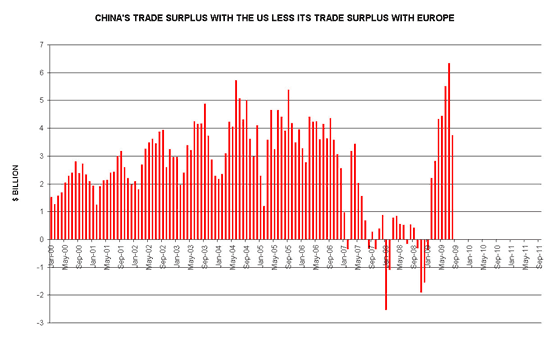

Now, it’s certainly the case that China has been an active buyer of euros in the open market, and that that activity, when combined with their persistently large USD/RMB intervention, has exerted an upward pressure on EUR/RMB. So Europe has a beef, right? Well, maybe, but certainly one no larger than that of the Yanks’. The chart below shows the difference between China’s trade surplus with the US and its trade surplus with Europe. A positive reading shows that the surplus with the US is larger. As you can see, from 2H 07 – 1H 09, the two were roughly the same size. Over the past few months, however, China’s surplus with the US has widened considerably relative to its surplus with Europe….and that’s with EUR/USD trending higher.

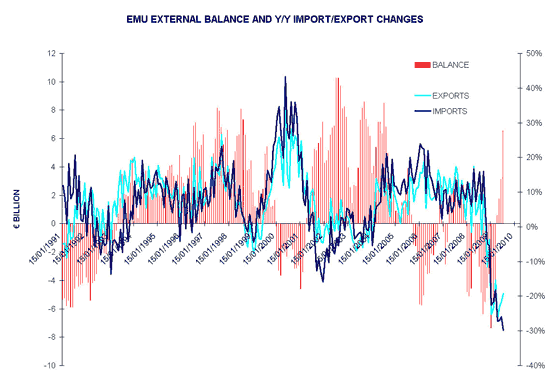

Indeed, looking at Europe’s trade figures, it’s hard to see why they’re a-bitchin’. Over the past several months, the extra-EMU balance has surged into surplus. Observe also how cyclical Europe’s trade balance is, evolving from surplus to deficit and back again as the economic cycle turns. For a developed, mature economy like Europe’s, this is almost certainly “fit and proper.”

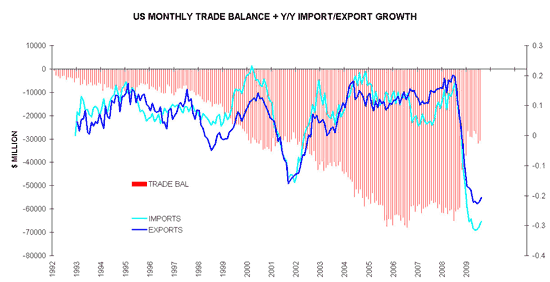

Compare the above chart with the equivalent one from the US; you can certainly see the impact of the financial crisis on the deficit, but also observe that that balance has remained in deficit consistently over the past seventeen years. Don’t forget to check the scale, either; America’s last, “small” trade deficit is basically three times the size as the worst one on the Eurozone chart. Remind me again why Europe is bitching?

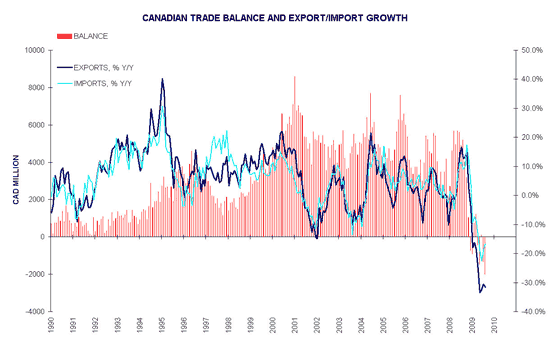

When a demand-heavy country like the US experiences a negative shock, it’s trade partners are supposed to see a retrenchment in its external balances. Canada, for example, as recently been registering record trade deficits (well, in fairness, any trade deficit in the Great White North is close to a record.) And while the BOC and FinMin have observed that the strength of the loonie is crimping the economy’s style, to Macro Man’s ear their observations have been considerably less strident than those emanating from Europe.

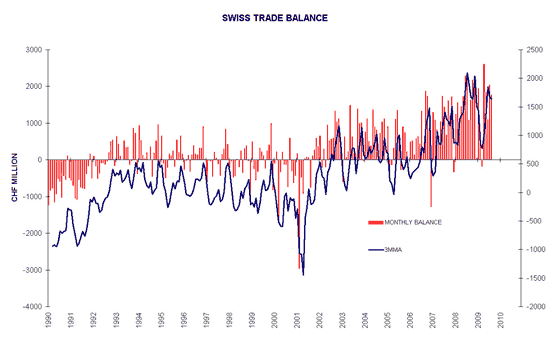

There’s another interesting distinction to be drawn, namely between Switzerland and Japan. Both have traditionally enjoyed large trade and current account surpluses. Over the past seven months, the Swiss have obviously taken concrete steps to weaken “stabilize” the franc, thereby safe-guarding its trade surplus near all-time highs.

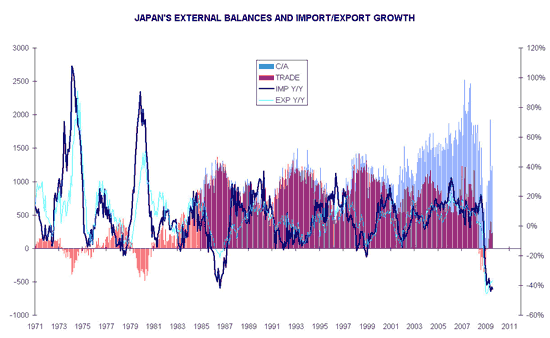

Compare that with the relatively newfound laissez-faire attitude of the Japanese towards the yen, which helped engender the first trade deficit in nearly thirty years. While the trade account has modestly tilted back into surplus, it’s nowhere near as good relative to history as Switzerland’s.

So what lessons are we to draw from all this? Looking at the assembled charts above, it seems pretty clear that (quelle surprise!) further rebalancing is required in the US. A weaker dollar would appear to be part of that equation; certainly the anecdotal evidence here in the UK (another persistent deficit country with a toilet paper currency) is that sterling weakness has curtailed the amount of foreign-made goods available for purchase.

Unfortunately, the (admittedly unscientific) contrast between Japan and Switzerland sends the message that protecting your patch is the right thing to do, while letting the global rebalancing chips fall where they may is an act of supreme folly. It’s a message that China and Europe appear to have learned all too well.

Looming protectionism has been a flashing dot on Macro Man’s radar for sometime; the apotheosis of the DGDF trend is likely to bring it into sharper focus. With the global recovery still on shaky footing, it seems likely that dollar weakness is going to force everyone (including the Americans) to try and protect their patch, whether they “should” be running a positive trade balance or not.

Unfortunately, there is no divine right to a trade surplus. Seventeenth and eighteenth century European monarchs once thought that they, too, had a divine right- in their case to rule as they saw fit. That worked fine…..until it didn’t. (Just ask Charles I or Louis XVII!!)

One can only hope that the denouement to the current “divine right” thinking is a bit less bloody….

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply