Sales of state-owned assets have been proposed as a way for highly-indebted countries to ease the pain of fiscal consolidation. This column argues that, despite the potential merits of privatisation in terms of long-run efficiency, in practice it is unlikely to improve short-run fiscal solvency. Since governments rarely alienate control rights, the efficiency gains from privatisations are often small. Moreover, financial markets may not fully reflect these gains – particularly during a financial crisis. The implication is that the Troika policy of linking financial assistance to privatisations is inappropriate and self-defeating.

In the midst of the European debt crisis, it is tempting to think that high-debt countries could alleviate the recessionary impact of the budget-consolidation process by selling (poorly managed) assets and stakes in their state-owned enterprises (SOEs), and by using the proceeds to buy back their debts (Hope 2011). In addition to providing a cushion for ongoing adjustment programmes and improving solvency, privatisations are deemed to entail long-term efficiency and welfare gains by attracting foreign direct investment and managerial expertise, thus spurring competition and growth.

Indeed, privatisations have been part of the Troika’s conditionality in Greece since the outbreak of the crisis. In March 2011, Greece signed an agreement with the Troika for a very ambitious privatisation plan. This envisaged the sale of public utilities, tourism resorts, concessions for the Athens airport and the port of Piraeus, and government shares of the OTE telephone company, as well as the partial privatisation of the Greek Agricultural Bank. In exchange, Greece could have borrowed from the European Financial Stability Facility at more favourable rates. The original plan was to raise €50bn – about 17% of the (then) outstanding debt – by 2015.

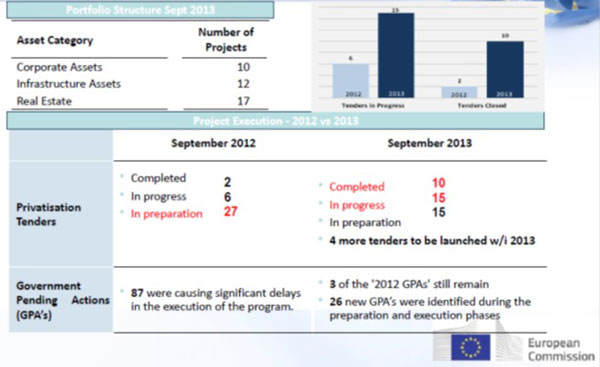

The plan’s progress was disappointing – in 2012 only two out of 35 privatisation tenders were completed (see Table 1), mainly due to delays in the required legal and regulatory changes (‘Government Pending Actions’ in the Commission’s jargon). In 2013, just 10 tenders were completed.

Table 1. Greek privatisations

Source: European Commission

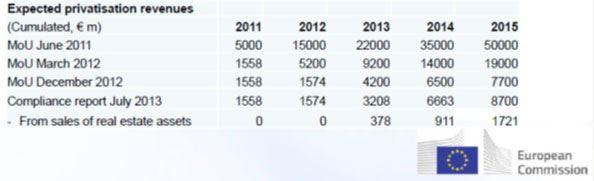

In the following years, the expected revenue from privatisations of state-owned enterprises, real estate, and banks was dramatically scaled down (see Table 2), dropping to just €8.7 billion in the Memorandum of Understanding of 2013.

Table 2. Expected revenues from privatisations

Source: European Commission

In this column I will focus on the following question: Is large-scale privatisation a viable option to improve the solvency of high-debt countries? I will argue that, in practice, the conditions required for state asset sales to improve solvency are unlikely to be met, particularly when a country is in financial distress. Thus the lessons from the recent Greek privatisation fiasco are probably quite general. I will first provide a simple numerical example, and then describe the relevant empirical evidence.

An example

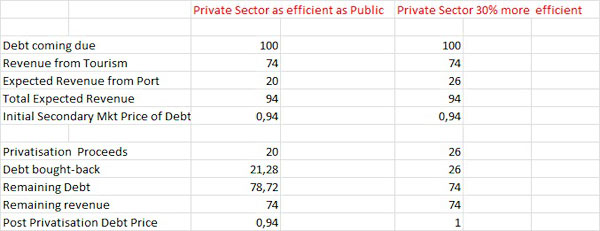

Consider the following example (Table 3). A country (call it Greece) has a debt coming due amounting to €100, consisting of 100 promises (bonds) to pay €1. Greek revenues come from two sources: one (tourism) generates €74 for sure, and one (say, the port of Piraeus) yields, on average, €20. Since the value of total (expected) revenues (€94) falls short of the debt coming due, Greece is insolvent, and its debt sells at a discount of 94 cents to the euro (this is the ratio of total expected payments, €94, to the value of outstanding bonds, €100).

Table 3. An example of privatisation

In order to improve solvency, the government (e.g. the Troika) decides to privatise the port of Piraeus, and to use the proceeds to buy back some of the debt. This example describes a very large asset sale – about one-fifth of the total debt at pre-privatisation prices. Let’s first consider the benchmark case in which the public sector is as (in)efficient as the private sector in managing ports (lower part of the first column, Table 2). In this case, the port of Piraeus will sell for €20 (the net present value of revenues), and with the proceeds the government will buy back 20/0.94 = 21.28 units of debt. After the privatisation, the total outstanding debt will thus fall to 100 – 21.28 = 78.72 units.

Has government solvency improved? Not at all. The government has forgone €20 of revenue from the port of Piraeus, and now it has to repay €78.72 worth of debt with only tourism receipts (€74). It is exactly as insolvent as before, and in fact the price of the debt on the secondary market is unchanged – expected payments/outstanding debt = 74/78.72 = €0.94.

Now consider the case in which the private sector is much more efficient (+30%) than the state at running ports, and may generate €26 (instead of €20) from managing the port of Piraeus (second column of Table 2). If capital markets are competitive, the port will now sell for €26. It will always be profitable for private investors to bid up to this price. It easy to show that, after the sale, the secondary price of debt will rise to €1, so that the government will buy back exactly €26 worth of its debt. Thus, only €74 of debt will be left – exactly equivalent to the remaining revenues from tourism (which confirms that the debt must sell at par).

Three lessons from the example

This example teaches us three lessons:

1. First, the government benefits from privatisation only as long it appropriates the increase in the asset value generated by the private sector. However, it takes a very large public inefficiency (-30%) in order to generate a small improvement in solvency (the price of debt improves from €0.94 to €1);

2. Second, for these benefits to materialise, the government must relinquish the control rights on the privatised asset – selling minority stakes or keeping ‘golden shares’ won’t work.

3. Third, financial markets must be competitive and have ‘deep pockets’, so that the state-owned enterprises are priced at the present value of the future dividends they generate;

Finally, note that a ‘successful’ privatisation plan should be associated with an improvement in the secondary market price of debt.

The evidence

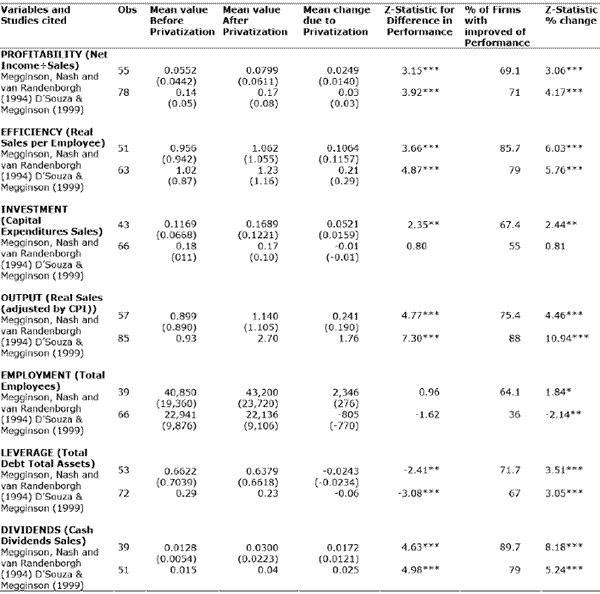

How large are the gains in profitability, productivity, dividends, and capitalisation of privatised (ex) state-owned enterprises? There is a large empirical literature, mainly referring to the privatisation episodes of the 1980s and 1990s. The results are often inconclusive and vary over time, episodes, and countries, as issues such as the regulatory and legal framework and the details of the privatisation process are crucial. Table 4 is taken from Megginson and Netter (2001), and compares the pre- and post-privatisation performances of 113 ex-SOEs.

Table 4. Empirical studies on privatisations

Whatever measure of efficiency we consider, the gains from privatisation appear at least an order of magnitude below the scale required for solvency to improve (30% in the example). Note that, from a methodological point of view, this literature is unconvincing – it does not compare the pre- and post-privatisation changes of SOEs and that of a ‘control group’ of SOEs which were not privatised, so the inference of the effect of the privatisation ‘treatment’ is quite dubious. Goldstein (2003) looks at the evidence of the Italian privatisation experience of the 1990s and compares pre- and post-privatisation changes to those of a control group of enterprises in the same sector. He finds no significant effect of privatisations.

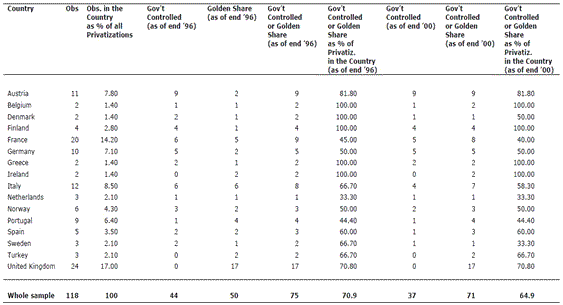

The second issue is that of the transfer of control rights. Bortolotti and Faccio (2004) present evidence from a sample of 118 SOEs privatised during the 1990s in Europe. The evidence suggests that the transfer of control rights after privatisation was far from complete – in as many as 65% of the cases analysed, the government retained 10% or more of the shares of the privatised firms and/or control rights through ‘golden shares’ (see Table 5 below). This fact highlights how reluctant politicians are to loosen their grip on SOEs, and provides a possible explanation for the less-than-expected gains from privatisations.

Table 5. Control rights

Source: Bortolotti and Faccio (2004).

Finally, it seems unlikely that a country which has lost access to the international debt markets can sell assets at a profit, although this cannot be ruled out in principle. The recent Greek episode provides an example of a lack of improvement in the secondary market price of debt following the announcement of an ambitious privatisation plan.

Conclusion

Privatisations should be judged on their own merits. Things like reducing the role of the state in the economy (particularly when this is associated with corruption) and boosting competition in the medium term are valid goals. As a tool for improving solvency, by contrast, privatisations are unlikely to be effective. Governments rarely alienate control rights, and the resulting efficiency gains are often less than expected. Moreover, financial markets, particularly during a financial crisis, may not price assets according to their expected returns. In the short term, a crisis-stricken country has little alternative to resorting to a mix of fiscal restraint, debt restructuring, and real depreciation. The implication is that the Troika policy of linking financial assistance to privatisations is inappropriate and self-defeating.

References

•Bortolotti, B and M Faccio (2004), “Reluctant privatization”, EGCI Working Paper 40.

•Goldstein, Andrea (2003), “Privatization in Italy 1993–2002: Goals, Institutions, Outcomes, and Outstanding Issues”, CESifo Working Paper 912.

•Hope, Kerin (2011), “Greek PM calls for consensus on privatisation”, Financial Times, 14 March.

•Megginson, William L and Jeffry M Netter (2001), “From state to market: A survey of empirical studies on privatization”, Journal of Economic Literature 39(2): 321–389.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply