During the Boston Federal Reserve conference on Fulfilling the Full Employment Mandate, there was a panel discussion on the importance of the dual mandate for the US Federal Reserve. The panelists were two of the Presidents of the Federal Reserve System (Kocherlakota and Evans), a member of the monetary policy of the Bank of England (David Miles) and Lars Svensson from the Riksbank (Swedish Central Bank). The four panelists presented complementary views on how central banks manage the trade off between inflation and unemployment under different mandates: an explicit dual mandate for the US Federal Reserve and a single mandate for the Bank of England or the Riksbank (same as the ECB).

Despite the differences in the way their mandates are written, the panelists stressed the similarities in actions of the three central banks and they also expressed support for aggressive monetary policy given the current circumstances.

What I found shocking in the presentations is how the panelists felt the need to explain the obvious. Both in Sweden and the US (as well as in the Euro area), inflation is and has been below the target for the recent past. Even if one thought of these central banks as being responsible for just inflation (single mandate), it is clear that they are failing to keep inflation from reaching that target. As Svensson made explicit, in the case of Sweden, inflation has now been below 2% for a significant period of time and it is unclear how the Riksbank will manage to produce an average around 2% over a medium-term horizon.

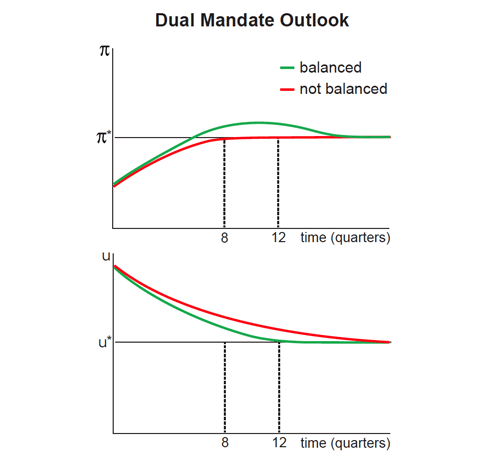

In addition, if one takes seriously the notion of a dual mandate, then there is a much stronger justification for current central bank actions. Both Evans and Kocherlakota showed very simple charts about the trade off between unemployment and inflation to support the notion that given the level of unemployment, having inflation be slightly above the target in the short run to accelerate the transition of unemployment towards what we consider normal is consistent with the dual mandate of the US Federal Reserve. Below is one of the slides used by Kocherlakota to explain this logic (full presentation can be found here).

Given the simplicity of the argument, the real questions is who they are trying to convince or, to put it differently, who are the ones who have opposing views on the inflation / unemployment outlook and monetary policy. I see two set of voices that are critical of the current central bank actions. First, there are those scared of inflation, or as Evanst put it, those who are afraid of “unlocking the long-ago-vanquished inflation demons from the dungeon”. Given how low inflation has now be for decades and how anchored inflation expectations are, it is difficult to understand where those fears are coming from. The second argument might sound more rational: if you want inflation to be around 2% in the long-term and given that we know that inflation will be higher one day when the recovery gets stronger, it might be ok to see inflation below target for a significant period of time (while the recovery is weak). But this argument depends on the slope of the Philips Curve. In a world where the Philips Curve is very flat (as it is for all these countries), it is very unlike that any fast reduction in unemployment will bring any significant inflation in the future. Therefore the fear of inflation when the recovery is strong, is not supported by the data either.

The panel discussion left me with a sense that over the years we have developed an unfounded fear of inflation and a very asymmetric view on what is admissible: being below the target is ok, being above cannot even be discussed as an option. And it was refreshing to see voting members of the monetary policy committees of the US Fed, Bank of England and Riksbank saying this explicitly — it was just the ECB that was missing.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply