Here’s a sign of changing times — not necessarily for the better. The WSJ reports that Option ARMs are now performing worse than subprime.

From the WSJ article:

For the third straight month, option adjustable-rate mortgages are generating proportionally more delinquencies and foreclosures than subprime mortgages, the scourge of the U.S.

Option ARMs were typically issued to creditworthy homeowners and allow borrowers to make a range of monthly payments. The payment options include a partial-interest payment that adds the unpaid interest to the loan’s balance. On many such loans, balances have risen while values of the underlying properties have plummeted amid the housing crisis.

As of April, 36.9% of Pick-A-Pay loans were at least 60 days past due, while 19% were in foreclosure, according to data from First American CoreLogic, a unit of Santa Ana, Calif.-based First American Corp. In contrast, 33.9% of subprime loans were delinquent, with 14.5% of those loans in foreclosure, the figures show.

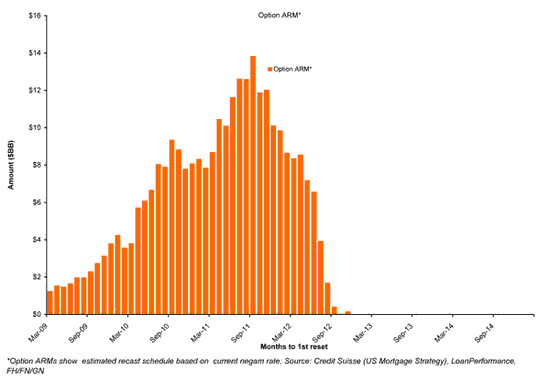

As you can see from the chart above, this is kind of disconcerting since these loans are just beginning to be recast. We haven’t even started to deal with this problem and their already cratering. I suspect that many of the borrowers are just throwing in the towel as they recognize how truly far under water they are. Do the math and figure out what 30% price depreciation combined with 10% negative amortization does to your equity position. Not pretty!

Then throw in a new amortization schedule at market rates on a 25 year term and you can quickly see that there is no feasible way out of this quagmire short of either massive foreclosures or massive modifications. We aren’t talking about starter homes either, folks. These loans were used by the overreaching middle class to buy the McMansions. Hold your fire if you want to trade up, the deals are coming.

The article in the Journal names Wells Fargo (WFC) and JPMorgan Chase (JPM) as being heavily exposed to this sector. True, both bought banks that had big portfolios of this junk. But there’s a big difference in the portfolios.

JPMorgans comes from WAMU (WAMUQ.PK) who did a lot of stated income deals with fairly low down payments. They cap out at neg ams of 110% generally. Big problems with this portfolio. Wells on the other hand bought Wachovia which bought their portfolio from World Savings. Most of these were done at 75% to 80% LTV and don’t cap out and require a reset until they reach 125% LTV.

Perversely, World was conservative in terms of the equity it demanded going in but pretty liberal in terms of the amount of negative am they would allow. Net, net they probably have a less exposed portfolio than Morgan.

The one thing you can expect is that there will be some sort of massive bailout of these loans. The people who used these mortgages to buy their homes have more political clout than the subprime folks. They have some levers to pull so expect to pay for their mistakes.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply