The Congressional Budget Office released their ten-year outlook for the US economy today. It is a very complex analysis. There are dozens of critical variables that go into this long-term report. A Base Line set of assumptions is put into a (very big) computer. The report makes projections on future debt levels.

This document is significant as virtually all other long-term federal budgets are built around the operating assumptions that CBO uses. Economists and politicians will use this report to push their own agendas. That is how things work.

My crystal ball is cloudy these days. I’m having trouble looking down the road past a week. I don’t have a clue what conditions will be like in five years. Neither does the CBO. But they have to produce this report and they have to make assumptions to do that. I think the variables were set at levels that are on the optimistic side. But I’m a pessimist so I’ll let you decide if these are reasonable assumption.

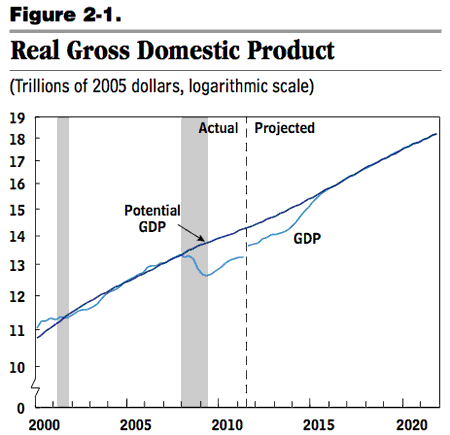

The most critical variable is GDP. The folks at the CBO see clear sailing and high growth for the whole ten years. Their average growth rate is ~15% higher than the previous decade. That is because of the big 08 recession. The CBO believes that won’t happen again. No “dip” in ten-years. There is no basis for that. The US has a recession every 5-6 years.

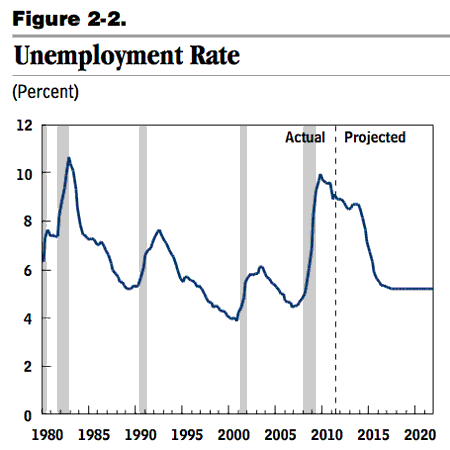

Another central assumption that drives the results is the rate of unemployment. According to the CBO happy days are right around the corner. Unemployment will fall to 5% in just a few years and stay at that level forever. We should be so lucky.

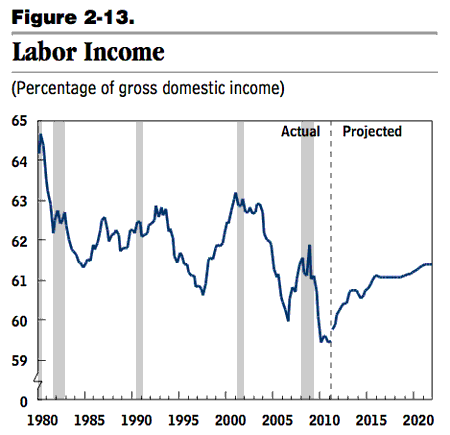

With the drop in unemployment would come an increase in hourly earnings. At least that is how the CBO sees it. Note that the hockey stick of improvement is supposed to happen, well, about a six months ago. Maybe I’m not looking in the right places.

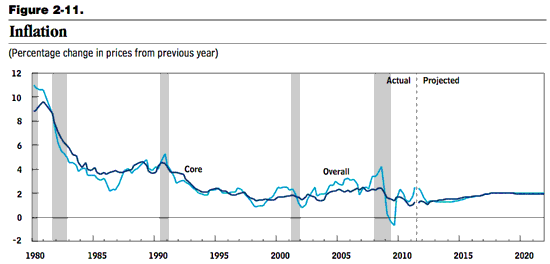

Inflation drives many components of the federal budget. I’m not sure what number to use. The CBO thinks it will be tame. Maybe. But I doubt it. We are in a ‘short’ resource world and the monetary authorities are pumping high-octane fuel. It would be helpful if the CBO were to stress test this at 4 or 5%. The results would be quite different.

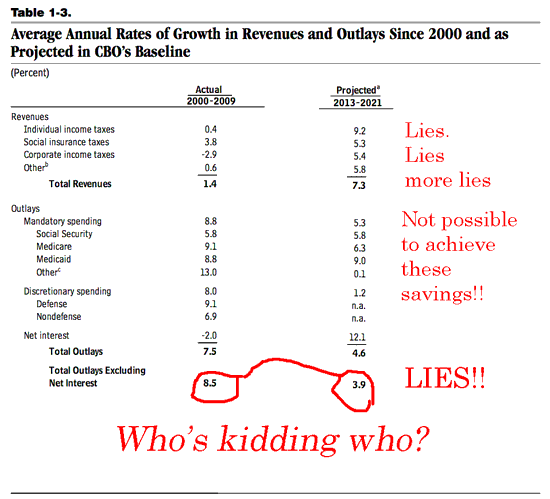

There are numbers for the revenue and expense side. Once again, the CBO plugs in some rosy assumption about the direction of income and spending. Just about every arrow is pointing in the right direction.

The bottom line from the CBO is that debt held by the public will rise from its current level of $10T to $14.5T over the decade. The good news is that the percentage of debt to GDP will fall from the current level of 67% to 61%. The conclusion is we’re headed in the right direction.

To do that the USA will have to hit the numbers that the CBO has set out. I see little chance of that happening. There’s too much ‘up-side’ built into the projections.

When S&P went to the White House and told them they were going to cut the USA’s AAA the Treasury Department went on the offensive. Tim Geithner led that charge and did his very best to convince the American people that S&P had it all wrong. That they were incompetent and did not understand the macro economic dynamics that drive our debt profile. Geithner used these CBO projections to make his case that the US was on a good track.

S&P said “No Sale” to that argument. Looking at the assumptions that Geithner relied on to make his case I don’t blame them.

Leave a Reply