The European confectioners are boiling up a new batch of their famous Greek Fudge. Just like last year this is being served up as a Willy Wonka-style panacea for European ills. The ingredients haven’t been listed on the box but TMM suspect they are:

- 4 lbs of European Artificial Sugar (Aspartame to get the markets ADHD really going)

- 3 lbs of Buttery Rhetoric, (greasy enough to make you sick)

Flavoured with: - 1 lb of Greek promises

- Liberal handfuls of Hope and Desperation.

But even if the market does swallow this latest melange it won’t satisfy their hunger any longer than a Friday night Chinese takeaway and will cause such indigestion that it will be repeating on them all year until it finally comes heaving back up as an issue in a year’s time. TMM are putting a big red ring around May 2012 and looking at 1yr fwd 1 month vol.

But undeniably, the risk regarding an imminent catastrophe is also significantly high, with domestic Greek political situation approaching a potential break point with Tuesday’s confidence vote. The ECB remain fiercely opposed to a restructuring that would spark banking system contagion (not to mention result in the central bank itself having to go cap in hand to politicians for new capital…), the fall of PASOK’s position in the polls to trail Samara’s ND party has clearly emboldened domestic brinksmanship, as has the German’s position on private sector involvement. TMM noted a few weeks ago that it seemed to them as though EU policymakers appeared panicked, and the commentary over the past few days has been consistent with this view (c.f. – Wellink’s comments regarding a doubling of the bailout fund). On top of that, Irish Finance Minister Noonan has returned to the rhetoric expressed while in opposition regarding imposing losses on senior bank bondholders in Anglo Irish. This isn’t just about Greece.

TMM get the sense that markets have moved beyond the actual Greek restructuring to consider the contagion that will likely emerge as a result of the A-Team Fudge boiling. Indeed, we were particularly interested to read of the exposure of US money market funds to European bank CP/CD/ABCP and repo, sitting at something like 44.3% of total assets. While the bulk of this is almost certainly in the “core” European banks, TMM would note that the events of the past few years would suggest that such institutions are likely to reduce their exposure to such paper when faced with potential uncertainty (one only has to recall the ABCP buyers strike in August 2007 and the even more serious wholesale funding run in September 2008). Moody’s placing of several French banks on review for downgrade clearly puts this risk on centre stage, and therefore,it is unsurprising to see a resurgence of financial system stress trades in the form of front-end flattening and basis spread widening (see 3m EURUSD basis below). While such moves have often turned out to be speculative in nature, with Libor not moving, TMM find it pretty hard to disagree with these trades in the context of a 0.24%-handle for 3m Libor.

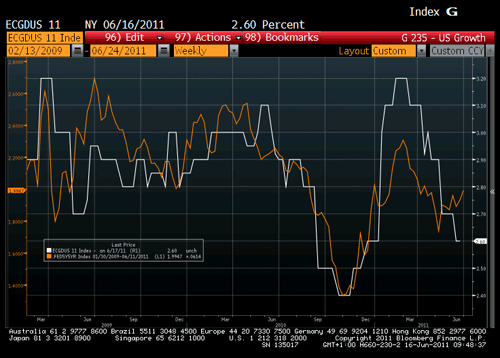

Of course, the above is only half the story, with the global data continuing to disappoint beyond what could plausibly be described as a Japanese supply chain impact. TMM would note that while both the PhD and market community have lowered their growth forecasts, they still sit well above levels consistent with what we have been seeing in the survey data. One of TMM’s favourite charts is the lagged 5y5y forward real rate (see chart below, orange line) vs. economist consensus 2011 GDP (white line), and despite the deceleration, the bond market has increased it’s growth expectations. Of course, this could arguably be risk premia as a result of the debt ceiling, rather than a true GDP upgrade, but TMM’s view is that this is a trade for late July, not now. Under this prism, TMM expect the curve to continue to bull-flatten given the absence of positions and a true embracing of the global growth slowdown.

With the ECB demanding that it gets its money back, the Germans insisting on “private participation” and the IMF offering money to tide the situation over until September on condition the Greeks sort themselves out, whilst the Greeks themselves dissolve their government and riot in the streets against austerity, TMM think the Eurostriches best chances are to shine the silhouette of a bat into the skies over Europe.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply