If an airplane is moving too slowly, the plane is about to head down. Federal Reserve economist Jeremy Nalewaik has an interesting new paper exploring whether the same is true for the U.S. economy.

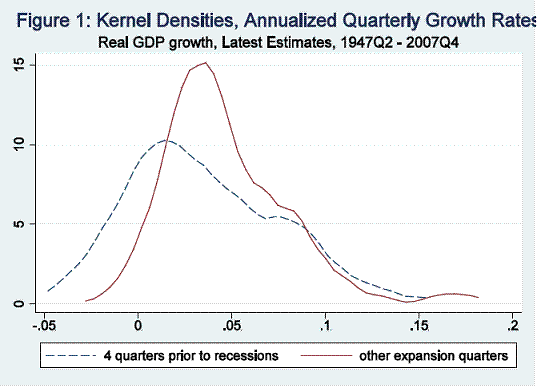

Nalewaik notes first that the 4 quarters prior to recessions were usually characterized by slower real GDP growth than is typically observed in an economic expansion.

Estimated density of real GDP growth in the 4 quarters prior to an economic downturn (dashed blue) and all other quarters characterized as economic expansion (solid red). Source: Nalewaik (2011).

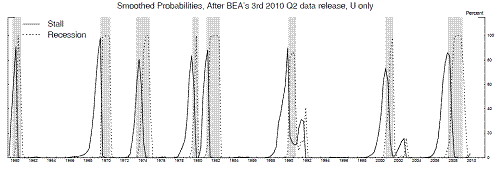

He then estimates Markov-switching models in which there may be an intermediate phase the economy moves into before or after an economic recession. This approach allows for a variety of possible outcomes. For example, it could capture a phase of rapid GDP growth in the first few quarters of a recovery, as proposed by Sichel (1994). However, Nalewaik usually finds evidence of a “stall” phase that the economy enters before going into a full-blown recession. For example, real GDP might be expected to grow at only a +1 to +2 percent annual growth rate per quarter while in the stall phase, before falling outright at a -1 to -2 percent rate during a recession. Unemployment in the stall phase might be expected to increase by 0.1% per quarter, before rising at 0.6% per quarter once the recession proper begins. The graph below shows the inferred probability that the economy was in the stall phase and the recession phase as inferred from unemployment dynamics.

Probability (reported as percent out of 100) that the U.S. economy was in the stall phase at any given date (solid) and in an economic recession (dashed) as inferred from unemployment rate alone. Shaded regions correspond to NBER recession dates (not used in estimation). Source: Nalewaik (2011).

The figure above represents an inference based on the full sample of data as subsequently observed. It is a trickier business to construct real-time forecasts with this approach. Slow economic growth or gradually rising unemployment sometimes is a precursor for a recession, but sometimes it’s just a temporary hiccup before more robust growth resumes. Nalewaik recommends a more detailed model for forecasting that makes use of other leading indicators such as the slope of the yield curve or housing starts.

And of course the big question right now is whether the recent sluggish growth could turn out to be part of another pre-recession stall phase. The yield curve is steeply sloping up at the moment. In normal times that would be a favorable indicator, but it’s pretty hard to interpret in the current setting with the short-term interest rate artificially stuck at zero. Housing starts are likewise of limited help at the moment since residential construction has been dead for so long.

My position remains that recent slow growth rates do not signal a coming recession, but that slow growth is a very painful and unsatisfactory outcome given the current high levels of unemployment. Nalewaik’s research gives us another reason to be concerned about forecasts of sluggish growth in 2011.

When the economy reaches stall speed

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply