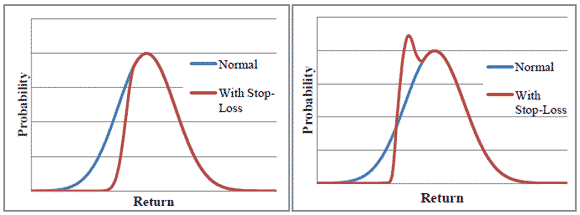

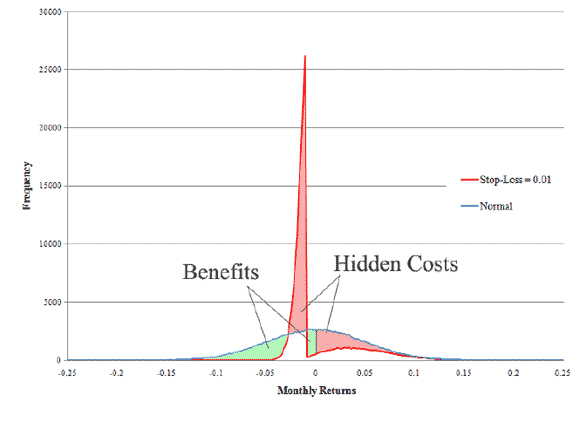

I’m sure everyone has been presented with the following logic: put in a ‘stop-loss’ at some arbitrary amount, say losing 1%. Then, your payoff distribution is tilted towards infinity, as shown above. It’s like the idea of going to Vegas, and saying you will stop when you lose $500, so you think that you still have an equal chance of generating those +$500 and up numbers, and the bad outcomes are just truncated at -$500. Alas, it doesn’t work like the graphs above. Instead, it generates the graph below, with a lot of probability mass at the stop-loss point:

From a nice little paper by Detko, Ma and Morito (2008).

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply