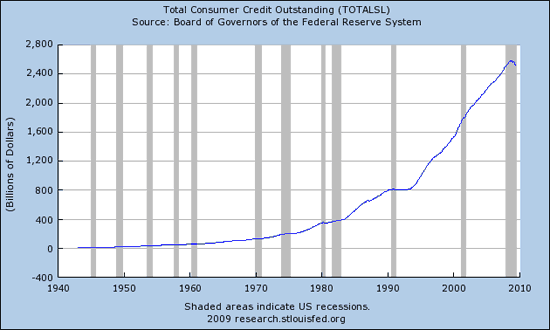

Since fiscal 2000, total outstanding consumer credit, which is composed of revolving and non-

revolving credit, and reflects most consumer short-and intermediate-term credit, has grown to unprecedented levels.

Divided by the number of adults in the U.S. over 18, this works out to an increase of approx. mid $4K per person. And as the following NYT article suggest, that number may continue to increase as borrowers still have a crushing amount of debt to deal with.

Confronted with unprecedented number of delinquent accounts, credit card companies are now resorting to settling red accounts for substantially less than the amount owed.

From The NYT: Revolving credit, a close approximation of credit card debt, totaled $939.6 billion in March. The Federal Reserve reported that 6.5 percent of credit card debt was at least 30 days past due in the first quarter, the highest percentage since it began tracking the number in 1991. The amount being written off was also at peak levels.

After a balance has been delinquent for six months, regulations require the card company to reduce the value of the debt on its books to zero. If a borrower has not paid by this point, chances are he never will.

“The creditors would rather have a piece of something now instead of absolutely nothing down the road,” said Adam K. Levin, the founder of the consumer education Web site Credit.com.

Banks and credit card companies are discussing new programs that would, for the first time, allow credit counselors to invoke reductions of principal as a routine part of their strategy, said Jeffrey S. Tenenbaum, a lawyer for many counseling agencies. In the past, counselors could persuade card issuers to adjust interest rates and modify late fees, but the balance was untouchable.

An example of how quickly the card companies are shifting their approach is in the behavior of HSBC, a major issuer, toward Mr. McClelland.

He was paying fitfully on his card, which was canceled for delinquency. In April, HSBC offered him full settlement at 20 percent off. He declined. A few weeks later, it agreed to let him pay half.

emphasis added

Graph: St Louis Fed

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply