We have a lot of confusion in economic forecasts right now. I have mentioned how in the middle of a correction, the market reaches a moment of maximum entropy, in a Chaos Theory sense, with energy flowing about evenly in and out (buying/selling). This ends with a sharp break, a bifurcation one way or the other. The entropy period reflects the market seeking order, and the break finding order.

Something similar seems to be going on with economic forecasts:

- There are V-like indicators (manufacturing, GDP, retail) surrounded by contrary indicators (real estate, unemployment, commercial loans)

- Krugman and deLong want more stimulus, and fear it is too late (see picture)

- Roubini, Rogoff, PIMCO and even Goldman Sachs think we are stuck in a slow U recovery

- Roubini adds that we still risk a double dip, as positive indicators like ISM are fading a bit, and others like housing and durable goods are down

- Shilling, Rosenberg and others expect a double-dip W

After the huge stimulus, both fiscal and monetary, we might have expected a more obvious recovery, if stimulus indeed works. The firehose certainly has some impact, but is all we are seeing it?

We stand at a point of confusion, where this could still go either way. Maybe we have a sharp V up from here, or maybe a flat to down patch.

The international picture is also mixed:

- Greece in trouble, the Euro in trouble? Ireland and Latvia both take deep cuts to regain solvency, but will Greece? And then Spain?

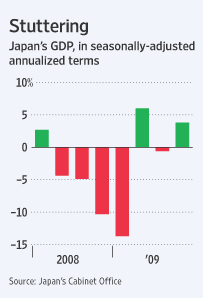

- Japan just revised GDP down after a negative Q3 (see chart)

- UK and much of the Eurozone is skimming the treetops on GDP

- China tightens, real estate is falling hard, but inflation is climbing. Can they muddle through?

I see positive factoids like an increase in floating corporate bond issues, an alternative to bank lending, even as commercial lending is frozen. The retail numbers and revisions look positive, although a lot may be due to tax refunds and Stimulus tax credits, not a sustainable change in consumer behavior. I also see negative projections that GDP may not be that robust in Q1, which puts a damper on the V. I could go on. The factoids are, on the whole, inconclusive.

I hold with the view of a V first, then a rollover back down in Q4 or Q1 2011. Every W starts with a V. Here is the logic:

Inventory levels are quite thin. We have had declining inventory even thru Q4 – what seems like inventory rebalancing is really a smaller drop QoQ, which shows up as positive in GDP calculations. I suspect we have an inventory surprise in Q1 and maybe Q2, where we see a real increase for the first time in a while, adding to GDP and maybe making Q1 and Q2 better than the current modest expectations. Combine that with temp workers fro census, and we can seem to be well on the way to a V shaped recovery by this summer.

Then we have the inventory rebalancing the other way, the dramatic drop in Stimulus (QoQ) and the letting go of those temp census workers – a surprising change of GDP and unemployment to the worse. We hit the Summer of Disillusionment.

The impact of this scenario on stocks would be a flat or rising period into the summer, then a sharp break down. A lot of pundits marvel at how high the Hope Rally has bounced, but they seem to miss the broader context:

- After a deep drop, we always have a sharp bounce

- American businesses cut deeply, and now have reasonable earnings expectations even on modest revenue: say $75 in the S&P, which puts the PE at just 15, about average

- The firehose of stimulus seems to have bounced us off a deep bottom

The rumblin’ stumblin’ rise in stocks fits this circumstance. Economic indicators remain mixed, but the trend is up. With continued concern over GDP in Q2 and a possible early double dip in Europe, stocks might just be flat more than up. I had mentioned in my prior post a possible triple top ending by late March or April, but this economic scenario suggest a slower, rolling triple top:

- First top in Jan at Sp1150

- Next top over the next two weeks at Sp1158-70

- Drop down to the range of the last major low, in July, of around Sp900

- Summer Rally heading into the Summer of Disillusionment

- Third top in late summer at around the same level as the first two tops

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply