Wow.

Was yesterday a game-changer? It certainly carried all the hallmarks of one. The SPX broke its uptrend line off the March lows, and while that’s only moderately interesting (given the number of similar such lines that have been breached during the 10 month rally), the fact that daily futures volume exceeded anything seen last year (even into the lows) was telling.

(click to enlarge)

The catalyst, of course, was Obama’s proposed “Volker Rule” to ban banks from owning/investing in hedge funds/private equity or even from proprietary trading. Now, Macro Man is hopelessly compromised here, as such proposals (if enacted) would be detimental to his profession.

And while it is probably imprudent to comment too much until the details are known, on the face of it such a draconian approach is both woefully misguided and appallingly naive. We can probably all agree that it’s in no one’s best interests to have a situation where a Lehman Brothers owns $50 billion+ in residential and commercial real estate turds, which brings down the firm and threatens the global financial system.

But there’s a big difference between that and having a team of punters (not dissimilar to your author) who coordinate and utilize the market intelligence available to large banks (which is enormous and extremely valuable) to make informed bets in the marketplace. Trying to ban such activities will, in any event, almost certainly be doomed to failure, as swathes of prop guys could simply be stashed away on franchise desks. Indeed, part of being a good franchise trader is to have a view and take prop risk anyways, so how could the Federales credibly eliminate it when it is all part and parcel of “serving the customer”?

Moreover, let’s not forget that it was proprietary trading- namely, the top-down decision to hedge against a subprime collapse- that helped save Goldman’s bacon in ’07-’08. Sure, the Feds stepped in when the crisis went nuclear, and yes that intervention to save the system may well have saved GS….but that doesn’t mean that there was no utility to their top-down decision to take a “prop bet” to hedge against subprime.

In any event, Goldman’s decision to donate $500 million to the Human Fund clearly wasn’t enough to spare the firm from Obama’s ire, let alone the public’s. They clearly know which way the wind is blowing, however; the firm paid out just 36% of revenues in employee comp for 2009. That’s loads less than other “human capital” intensive industries like sports or entertainment, and miles less than Morgan Stanley, which paid out 62% of revenues in employee comp. Morgan Stanley, incidentally, lost money last year, precisely because of these princely wage awards. Regardless, slashing the bonus pool to boost earnings did little for the GS share price; courtesy of Obama, the stock price fell sharply on its highest volume since last April.

(click to enlarge)

Now, let’s be clear: there is plenty to dislike about the way banks have conducted business over the past eighteen months, and things should change. Perhaps these proposals are simply a cack-handed way of re-introducing Glass-Steagall (i.e., dividing banks into commercial and investment banks) without literally re-introducing Glass-Steagall. Perhaps they’re even intended to encourage the likes of GS to re-privatize into partnerships. Macro Man has gone on record suggesting that both of these are desirable outcomes from a systemic perspective.

Surely the thing to do, however, is to impose top-down leverage limits and, within that construct, allow firms to get on with their business as they see fit. Trying to micro-manage the business of banking by creating lists of allowable activities is decidedly substandard. Of course, the policy was likely driven by populist impulses in the wake of the Democrats’ shocking defeat in Massachusetts, and as we know the public’s grasp of nuance leaves something to be desired (nearly 20% of the American public reportedly believe that the sun orbits the earth, for example.)

Regardless, when drastic populist policies are proposed (though perhaps not implemented; Macro Man’s been surprised at the relatively unenthusiastic legislative reaction thus far), the result is generally suboptimal outcomes. If yesterday really was a game-changer, perhaps it’s time to start dusting off those W-shaped forecasts (or even the Cyrillic letter I shapes?!?!) for risky assets.

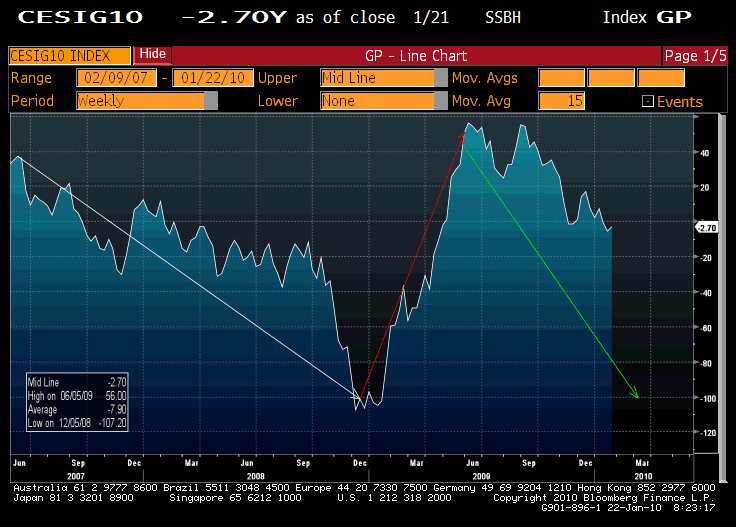

Rumblings of Chinese tightening do not help, nor indeed does the apparent waning of developed market growth momentum. The Citi major economy surprise index, for example, looks to be tracing out either a W or a И shape.

(click to enlarge)

Hmmmm…a tepid economic recovery, a suboptimal, populist-driven policy reaction to a market crisis, and an equity dump after it felt like the worst had passed. How do you spell W again?

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply