Incoming data continue to support expectations that the Federal Reserve will hold rates at rock bottom levels for the foreseeable future – likely into 2011. But interest rates should not be the focus of policy analysts. The Fed will manipulate policy via the balance sheet long before they fall back to the interest rate tool. The question is whether or not the slow growth environment is sufficient to persuade the Fed to hold the balance sheet steady or even expand the balance sheet beyond current expectations. And there always remains the third option, favored by a minority of policymakers – withdraw the stimulus now that growth has reemerged. At this point, I suspect the Fed will stick with the hold steady option.

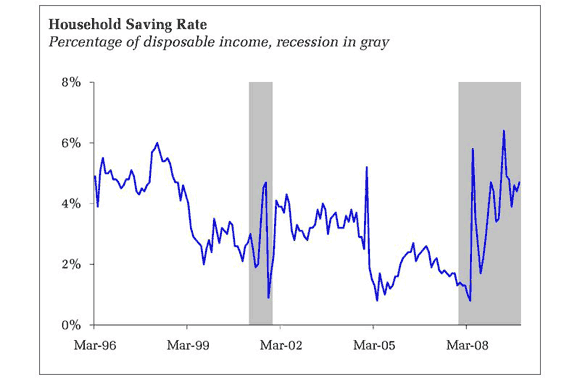

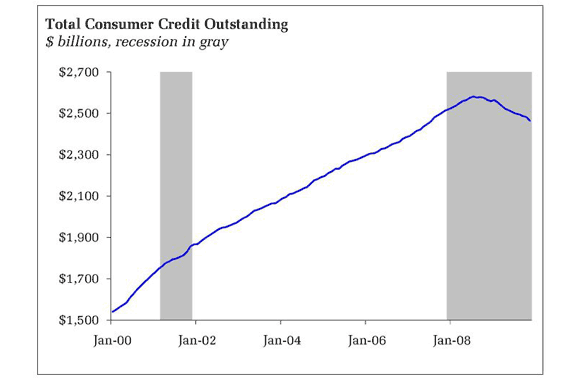

One of the key elements of the slow growth story was the inability and unwillingness of households to revert to past spending habits. The critical parts of the story are that savings rates would rise as household struggled to rebuild tattered balance sheets and that credits would become dearer. These stories are playing out in the data:

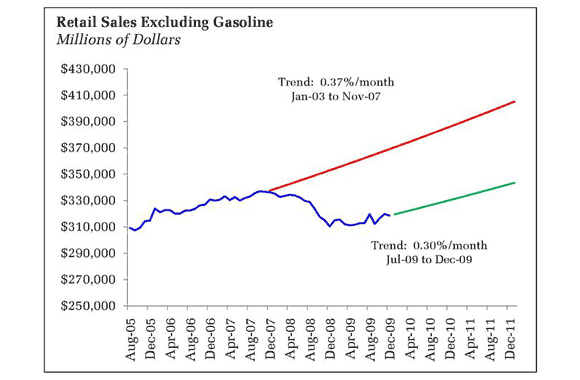

Yet the trends of consumer spending has been undoubtedly upward since June, as has been overall economic activity. Cyclically, the economy is on an upswing, surprising many who believed the apocalypse was at hand. But fears of a consumer apocalypse were always overblown; the change need only be moderate to have a large impact on the overall economic environment. It is not necessary that consumers crawl into their basements, curled into a fetal position hugging a bar of gold in one arm and a loaded shotgun in the other, to dramatically alter the role of households in the economy. Consider, for instance the path of retail sales excluding gasoline:

The November-December average monthly growth trend is 0.032% (note: log difference approximation), while the July-December trend is 0.03% and averages out the distortion caused by the “Cash for Clunkers” program. In either case, the spending trend is below the prerecession trend in sales growth. What are the takeaways from such an analysis?

1. Underlying demand is rising. The resulting stability is helping stabilize the job market; the December decline in nonfarm payrolls was negligible in contrast to the 600k or 700k monthly losses at the height of the recession. This is not meant to imply that the unemployment picture is positive; just that it is significantly less bad.

2. The pace of underlying demand during the recovery to date slowed compared to prerecession growth rates. This is the slow growth story evolving. Stronger retail spending is dependent on stronger job growth (but faster growth could entail a rise in energy costs, which would squeeze other spending). We are not there yet.

3. Retail activity remains well below the trend expected in 2007. A forgotten piece of the puzzle, in my opinion. The capital infrastructure of the retailing sector was predicated on the expansion of spending along the red line. A lower path leaves the sector overcapitalized on a long term basis, suggesting that a rapid rebound in retail commercial real estate is very unlikely. Moreover, the spending that would have occurred absent the recession must now find another home.

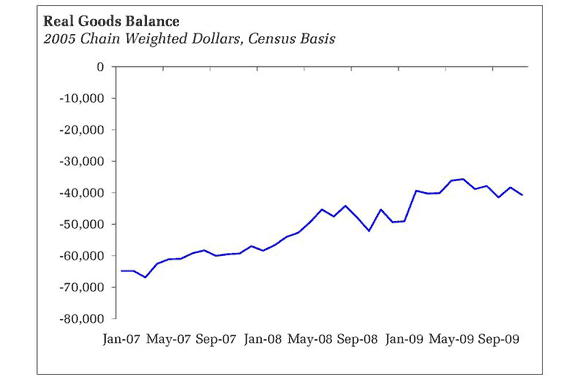

One hope was that the consumer decline would be offset by improvements on the trade side of the equation, the rebalancing story. But no such luck yet. Improvement in real net exports has stalled as the rebound in global activity has stimulated US imports slightly more than US exports:

To be sure, trade is supporting improvement in some manufacturing industries. But net exports is the key for overall economic activity, and it looks like we need much stronger growth abroad to sustain overall net exports. But the news out of China this week was worrisome on this point:

Chinese authorities on Thursday took the latest in a series of steps to cool the country’s supercharged economy amid worries over inflation, engineering a minor tightening of credit that unnerved global markets.

For the first time in nearly five months, the central bank edged up the interest rate on its three-month treasury bills by about 0.04 point, to 1.3684% from the 1.3280% yield that has prevailed since August.

It would be unfortunate if inflationary pressures abroad slowed US export growth. Some have logically speculated that tighter credit controls foreshadows an eventually appreciation of the yuan. I am hopeful yet skeptical; I can also see Chinese authorities attempt to use the external sector to compensate for waning domestic stimulus.

In short, the recent trade and retail sales data suggest what many expected: Absent inventory correction and federal stimulus, the underlying rate of growth is anemic at best (note that perhaps half of the anticipated 4.5-5% growth in Q4 is inventory related). In this case, the v-shaped recovery emerging in manufacturing is not sustainable for the broader economy. But the absence of these factors does not guarantee recession; I think an anemic recovery remains the most likely medium term outcome.

In such an environment, with a significant gap between capacity and demand combined with mostly downside risk to the pace of activity in the second half of this year, monetary policymakers should be wary about withdrawing stimulus. Yet not everyone is. Kansas City Fed President Thomas Hoenig sent up a hawkish signal last week:

Unfortunately, mixed data are a part of all recoveries. And, while there is considerable uncertainty about the outlook, the balance of evidence suggests that the recovery is gaining momentum. In these circumstances, I believe the process of returning policy to a more balanced weighing of short-run and longer-run economic and financial goals should occur sooner rather than later…

The group pushing for a near term withdrawal of stimulus is likely small (hopefully, a group of one). But an effort to shrink the balance sheet is not the immediate threat. Soon to come is the conclusion of the mortgage asset purchase program, an end that is likely to trigger a rise in mortgage rates. And Fed officials know it. Via Calculated Risk:

Eric S. Rosengren, president and chief executive of the Boston Fed, said in an interview at The Courant that he expects [mortgage] rates to rise when the [Fed MBS purchase] program ends — or before, as the end approaches…

“Actually, I’ve been surprised that we haven’t seen more of a backing up already,” Rosengren said. “You maybe would have thought you would have seen rates move up more quickly than they have, but nonetheless that is a concern.”

…The mortgage rate increase of one-half to three-fourths of a percentage point from the end of the Fed program would happen regardless of any Fed action in interest rates, Rosengren said.

It seems the Fed knows they will be delivering a contractionary blow to the economy just by ceasing balance sheet expansion – indeed, everyone (except maybe your local realtor) knows the housing market is being held together by little more than bailing wire and duct tape. Hence why some policymakers are troubled by the impending exit. From the minutes:

The Committee emphasized that it would continue to evaluate the timing and overall amounts of its purchases of securities in light of the evolving economic outlook and conditions in financial markets. A few members noted that resource slack was expected to diminish only slowly and observed that it might become desirable at some point in the future to provide more policy stimulus by expanding the planned scale of the Committee’s large-scale asset purchases and continuing them beyond the first quarter, especially if the outlook for economic growth were to weaken or if mortgage market functioning were to deteriorate. One member thought that the improvement in financial market conditions and the economic outlook suggested that the quantity of planned asset purchases could be scaled back, and that it might become appropriate to begin reducing the Federal Reserve’s holdings of longer-term assets if the recovery gains strength over time.

This translates into the following: The Fed is not committing to an absolute end to asset purchases, but the bar to extending purchases is relatively high considering policymakers appear to be divided on the issue. A backup in mortgage yields is expected, and by itself will not be cause for alarm. Either financial distress or ongoing job losses are likely to persuade officials to return to asset purchases.

Critically, the focus is on asset purchases. From Bloomberg:

The Fed should retain flexibility by adopting a “state- contingent” policy that would allow for the adjustment of such purchases as new information becomes available, Bullard, who votes on monetary policy decisions this year, said today in prepared remarks for a speech in Shanghai. He said it was “disappointing” that markets focus more on interest rates instead of the Fed’s quantitative monetary policy.

U.S. central bankers switched last year to asset purchases and credit programs as the primary tools for monetary policy, including buying mortgages and government securities to reduce borrowing costs and stimulate growth. The Fed has expanded its balance sheet to $2.24 trillion at the end of 2009 from $858 billion at the start of 2007.

“Markets are still thinking of monetary policy strictly as changes in interest rates even though the Fed has been conducting successful policy this past year through quantitative easing,” Bullard said. “Markets should be focusing on quantitative monetary policy rather than interest rate policy.”

St. Louis Fed President James Bullard is delivering a pretty clear message. In his view, policy for the foreseeable future is about altering the rate of asset purchases, not interest rates. This will be a challenging new ocean for Fed Watchers to navigate. Will the Fed scale up asset purchase by $25 billion? $50 billion? Hold steady? Sell $25 billion back into the markets? Fun, fun, fun.

Bottom Line: The underlying pace of growth is in doubt. To be sure, manufacturing is getting a boost from inventory correction and pent up demand; the upward trend in industrial production, ISM, capacity utilization, and new order for nondefense, nonair capital goods all look solid. But households are financially hobbled, and net import growth remains lacking. All told, the net impact is to stem the pace of job losses and, if temporary help is an indication, set the stage for actual gains in nonfarm payrolls in the months ahead. But a rapid reversal of the dreary employment setting looks elusive, especially given the likelihood that growth slows as government stimulus wanes in the second half of 2010. Loose cannons like Hoenig aside, all of this should keep monetary policymakers on hold, not pushing to actively contract the Fed’s balance. Further expansion of asset purchases is not out of the cards, as Bullard makes clear. But the bar to additional purchases looks high; the Fed will wait to see how actively evolves before taking that road.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply