Paul Krugman ([1], [2], [3]) has been arguing vigorously that U.S. budget deficits are no cause for concern. I see things differently.

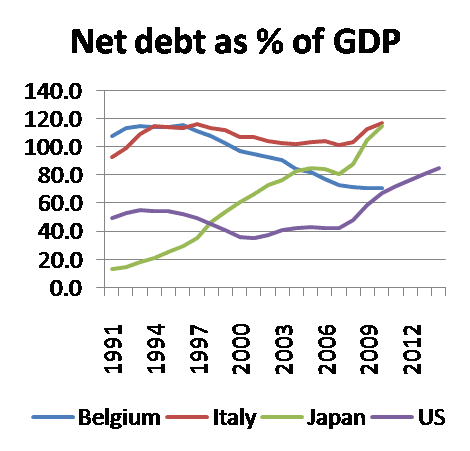

One of the arguments that Krugman makes is that, although the U.S. debt-to-GDP ratio is expected to double over a short period, the higher level would still be substantially below those currently observed in Italy and Japan, and only modestly above that of Belgium. Paul suggests that if these countries can run up debts of this magnitude without serious repercussions, so can the United States.

Source: Paul Krugman

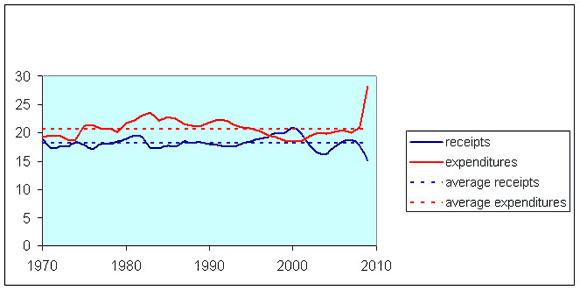

But European politics may not import all that well to this side of the Atlantic. Receipts of the U.S. federal government have never exceeded 21% of U.S. GDP, even at the height of World War II. A permanent move to taxation levels significantly above that would require a major shift in the political landscape, for which I see no consensus of support. To me that implies that any spending trajectory inconsistent with the long-established U.S. norm may be headed for a political brick wall.

Federal receipts and outlays as a percentage of GDP, 1970-2008 and 2009 estimates. Data source: OMB.

One of the ways I have suggested for personalizing this issue stems from the observation that $1 trillion is approximately the total personal income tax receipts collected by the U. S. federal government in 2006. So, to calculate what another trillion in deficits means for me personally, I take the amount I paid in federal income taxes that year and double it; $10 trillion in new debt will require 10 years at that higher rate to pay off. It’s going to be a real problem for any politician who tries to service the growing debt burden by raising taxes. That’s why I see troubles ahead for managing the federal cash flow.

But Paul feels I’m using an inappropriate metric:

Jim gets scary numbers about the debt burden by assuming that we’ll have to pay off the debt in 10 years. But why would we have to do that? Again, the lesson of the 1950s– or, if you like, the lesson of Belgium and Italy, which brought their debt-GDP ratios down from early 90s levels– is that you need to stabilize debt, not pay it off; economic growth will do the rest.

Normally, you’d think that putting off repaying a debt does not make it any smaller. The federal government can (with my wallet) pay the trillion today, or it can wait 10 years to pay one trillion plus 10 years’ interest, or wait 20 years to pay one trillion plus 20 years’ interest. The present value of the service cost on one trillion dollars in debt is exactly one trillion dollars today, no matter how long you put off paying. My comments on how much a trillion really is are perfectly appropriate for discussion of any repayment timetable.

Perhaps Paul is suggesting that there may be a potential free lunch available from postponing payment in this case, arising from the fact that the economy’s growth rate has historically exceeded the government’s cost of borrowing. If I put off paying another year, with interest the amount I owe grows 2% in real terms, but my income grows 3%, so things get easier the longer I put it off.

Let me go on the record as favoring the consumption of truly free lunches. If everything the government buys really is free, then by all means, let’s have them buy more, and more, and more, and rather than double my taxes, let’s cut taxes all the way to zero. Unfortunately, I expect that Paul would agree with me that in fact there is a limit to just how much we can count on supersizing this particular happy meal. At least I know that he entertained such concerns, as Scrivener and Verdon note, when in March of 2003, Paul contemplated the implications of the debt-to-GDP ratio that was then reaching 40%:

we’re looking at a fiscal crisis that will drive interest rates sky-high…. But what’s really scary… is the looming threat to the federal government’s solvency.

What I presume was producing Paul’s concerns in 2003, and is giving rise to my concerns today as well, is the fact that the low cost of government borrowing relative to the economic growth rate– which could produce the apparent free-lunch calculus– is predicated on the historical political equilibrium, which Paul worried might not be continued after 2003, and I certainly worry might not be continued after 2009. Specifically, I would suggest that the low borrowing cost that the U.S. government traditionally faced was very much attributable to the responsible management of the debt. Once that responsibility becomes called into question, the U.S. will cease to enjoy that privilege. This kind of problem gets messier, not neater, the longer you put it off. And that’s why you might not want to assume that an apparent free snack can be scaled up to an unlimited feast.

Which brings me to Paul’s third argument:

Right now, however, the bond market seems notably unworried by deficits. Long-term interest rates are low; inflation expectations are contained (too well contained, actually, since higher expected inflation would be helpful). No problem, right?

Alas, I’m getting the sense that the Obama administration is intimidated all the same. We’ve got the president telling Fox News that he’s worried about a double-dip recession if he doesn’t reduce the deficit soon– as opposed to the concern I and other have that he’ll have a double dip if he doesn’t provide more support. (And why is Obama talking to Fox News, btw?) And the buzz is that admin economic officials are telling him that the bond market needs to be appeased, even though rates are low.

This is truly amazing. It’s one thing to be intimidated by bond market vigilantes. It’s another to be intimidated by the fear that bond market vigilantes might show up one of these days, even though you’re currently able to sell long-term bonds at an interest rate of less than 3.5%.

Paul is absolutely right that, at the moment, we’re observing an amazing willingness of investors and foreign central banks to lend to the U.S. Treasury. On Monday the Treasury successfully auctioned $44 billion in 2-year notes paying the lowest yield on record, and last week the nominal yields on some bills on the secondary market actually turned negative— people paying for the privilege of being able to lend to the government. So if the government were to borrow another dollar today, invest in anything with a positive rate of return, and repay the sum in two years, it would indeed be a great deal.

Those remarkably low yields at the moment in my mind are a result of a flight to safety. Many people are afraid to hold anything other than treasuries until there’s some more clarity to the economic and financial landscape. It’s not so much a market vote in favor of the U.S. Treasury as it is a market vote against everything else.

But the question before us is, what will the situation be another two years down the road, when the government will need to go back to bond markets to roll over the debt it issued on Monday along with new debt to cover the several trillion added to the federal debt between now and then? Krugman’s position is that we should trust the term structure of interest rates to give us the answer. If markets anticipate an explosion of short-term interest rates a few years down the road, why is anyone today buying the longer term debt at such low yields?

If you thought that there is some chance that treasury yields will only rise slightly over the next few years, but also some risk of solvency problems and a panic flight from the dollar, what you might want to do is to take a long position in treasuries hedged with a long position in commodities. I agree with Paul that the long-term treasury yields are hard to reconcile with a market worried about the solvency risk. But I would add that the run-ups we’ve seen in commodity prices are hard to reconcile with a market sold on the deflation scare. What I see is investors buying both bonds and commodities, suggesting that people are spreading their money across a variety of strategies to be in position for several alternative scenarios from here.

Is it possible that some time within the next five years, the U.S. Treasury will run an auction in which there are not enough bids to roll over the debt? My answer is yes.

For other thoughtful perspectives, see Brad DeLong, Carlo Cottarelli, Dean Baker, Tyler Cowen, and Free Exchange.

Yes the future deficits are worrisome

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply