Equity futures are roughly flat to up a little this morning after being lower, then higher.

The dollar swung higher and then fell back to flat overnight, collapsing back down quickly, showing its propensity to return to the 75 level. There’s a battle going on here, and my saying is that the longer something keeps knocking on the door, the more likely it is to break through… but it cannot and will not sit at this level forever, the break will be interesting. Break up, equities will go down. Break down, most people believe equities will moonshot, and that may be true initially, but the dollar breaking down WILL eventually tank equities, there is no fooling mother nature, no way to get around paying our debts, they must be cleared. Bonds are higher, and if you’re looking for a clue as to equity direction for the day, that is probably it. Oil is down slightly, gold is up a little more, $1,169.

Yesterday was the 10th Monday ramp job out of the past 12 weeks. I must have read four different people talking about that, look for future ramp jobs to come on, oh, Friday. No, wait, most of the Goldman boys are gone that day spending their bonuses, so we better schedule that for Wednesdays.

Both Robert Prechter and McHugh pointed out the time and price relationships in play at this juncture; the B wave rally has now taken exactly half the time of the A wave descent, and it has retraced half the plunge, a very important confluence of price/time. Thus Prechter said, once again, that he believes the top was just put in. McHugh is saying it’s important, but there is still the EW possibility of higher.

The short term stochastics are obviously overbought, there are new short term bearish divergences on top of the historic much larger ones.

The absolutely unreliable ICSC showed store sales were flat week over week but rose 3.3% yoy on much easier comparisons. That’s interesting because sales tax collections are down roughly 8%. Which is correct? Well, the sales tax collections, of course as they are not manipulated. The ICSC suffers the same flaws as the indices with substitution bias among other inaccuracies. The Redbook likewise showed a 2.8% yoy increase against easier comparisons, again, a flawed report, as sales tax data is also yoy, but even it is now measured against this time last year making for a very easy comparison.

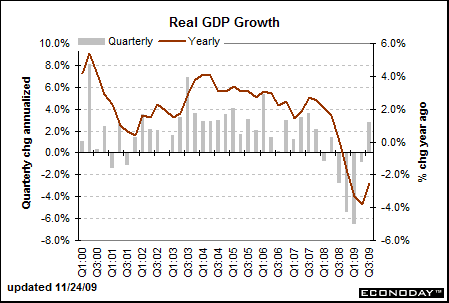

The first revision of Q3 GDP lowered the annualized growth rate down from the much ballyhooed 3.5% down to 2.8%, a mere drop in growth rate over that advertised of only20%! Business as usual here during the Great Deception. But of course that was expected… Look, they can, and do, make this number come out any way they want. Did the economy actually grow in the 3rd quarter? NO. It is still shrinking when measured in real money, as it has been ever since the year 2000. At any rate, here’s the propaganda for public consumption:

Highlights

The recovery is not as strong as hoped, based on the latest Commerce Department revision to third quarter GDP. Economic growth was revised downward to an annualized 2.8 percent from the initial estimate of 3.5 percent. The market consensus had expected a 2.8 percent figure for the new estimate. Nonetheless, the third quarter boost is still the first positive number for GDP since a 1.5 percent gain in the second quarter of 2008. The third quarter increase, however, appears to have ended the recession which faded with a 0.7 percent dip in the second quarter.

The downward revisions were broad based, lowering estimates for PCEs, nonresidential structures, residential investment, business inventories, and net exports. Upward revisions were seen in business equipment & software and in government purchases.

But compared to the second quarter, the improvement in real GDP in the third quarter still reflected upturns in personal consumption, exports, and residential fixed investment and a smaller decrease in nonresidential fixed investment and inventory investment. These were partly offset by rise in imports, a downturn in state and local government spending, and a deceleration in federal government spending.

Motor vehicle output added 1.45 percentage points to the latest quarter’s growth, compared to the initial estimate of 1.66 percentage points.

Year-on-year, real GDP stood at minus 2.4 percent compared to minus 3.8 percent in the second quarter.

Turning to inflation, the GDPI price index was nudged down to a 0.5 percent annualized pace and compares to the initial estimate of 0.8 percent and the median forecast of 0.8 percent.

Two items stand out in the report. Final sales were revised down to an annualized 1.9 percent from the initial estimate of 2.5 percent. Demand is not as strong as earlier believed. Second, the downward revision to the price index also indicates softness in demand. These two issues could weigh on equities at open and soften Treasury yields. But there is much more economic news ahead today.

And talk about more fantasy, marked to fantasy corporate “profits” on year over year comparisons were up and annualized (key word), 71.9%… huh? PLEEEZZZE. How ’bout we annualize the weekly Treasury auctions, shall we? Try $9 trillion a year, so that all the businesses in this country can generate $1 trillion a year in phony profits! Nice try, Econoday, let’s just stick to the year over year percent change that shows a 7.2% drop which is better than the 19.2% plunge in the second quarter. Yes, reported profits were up slightly, but the yoy number is against a much easier comparison, and that time last year the financial industry was still marking somewhat to market, unlike this year where all bets are off and they are back to marking all their assets to whatever gives them the biggest bonuses. Again, no basis in reality, look at tax receipts instead for reality:

Highlights

Corporate profits in the third quarter posted a sharp gain to $1.181 trillion annualized-up from $1.031 trillion the prior quarter. Profits in the third quarter were up an annualized 71.9 percent, following a 24.5 percent boost the prior quarter. Profits are after tax but without inventory valuation and capital consumption adjustments. Corporate profits are still down 7.2 percent on a year-on-year basis, compared to down 19.2 percent in the second quarter.

The Case-Schiller data showed a very slight improvement, the 20 city index rose from 146 to 146.51 in September. Here’s Econoday:

Highlights

Home prices continue to improve according to Case-Shiller data. The report’s index for the top 10 cities rose 0.4 percent in September, on the low side of what is a long strong string of improvement. Year-on-year rates continue to improve, now down to single digit contraction at minus 8.5 percent for the 10 index. A look at the quarter-to-quarter rate shows steady improvement, at plus 3.1 percent for both the third and second quarters. Improvement is especially evident in the West and Florida, high flying areas hit hardest by the housing downturn. This report, noted for its vigorous methodology, continues to contrast with price data in the existing home sales report where contraction, though slowing a bit, is still underway. New home sales data for October will be posted tomorrow. Prices in this report did show improvement in September.

Pretty much a yawner. Another report came out and said that 1 in 4 mortgages are now underwater…

NEW YORK (CNNMoney.com) — In a sign that more foreclosures could be on the horizon, 23% of people with mortgages owe more than their home is worth, according to a report released Tuesday.

Almost 10.7 million U.S. mortgages were “underwater” as of September, said research firm First American CoreLogic.

Another 2.3 million homeowners are within 5% of negative territory, the report said. The two figures combined comprise almost 28% of all residential properties with mortgages.

Negative equity, also called an “underwater” or “upside down” mortgage, has become more common as home values plummet. The report is closely watched because borrowers who are underwater are more likely to be foreclosed.

Of course we know that the option-ARM reset debacle is just now picking up where sub-prime left off. Amazing how many people ignore it.

Consumer Confidence comes out at 10AM…

I’m just waiting for the nut to crack and not getting too worked up about anything at this juncture. Soon the dollar and equities will pick a trend, it’ll probably be real obvious when they do. The E.W. counts say that trend will be up in the dollar and down in equities. If the dollar rolls down further as those in the administration are trying to force, I think the outcome will not be what they expect. They think they can devalue debt away. The problem nature has with that is that when they do, people’s purchasing power goes down, thus they must work more to get the same amount of goods. It all boils down to productive effort. The law of nature states that all debts get repaid with interest in one way or the other… you can fight that law, but guess who wins?

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply