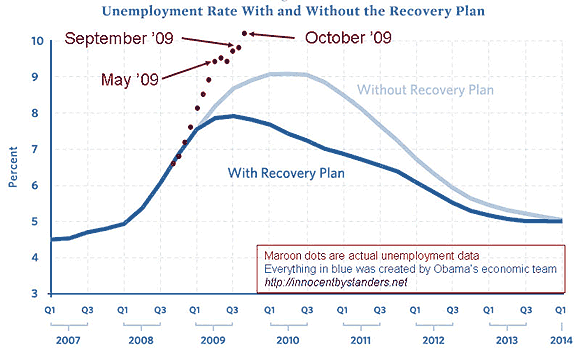

The market is watching unemployment as an indicator of when the Fed will raise rates. In prior recessions the Fed has waited until unemployment has peaked before raising. The first chart shows the beginnings of a plateau over the summer, but the October numbers shot us back up again.

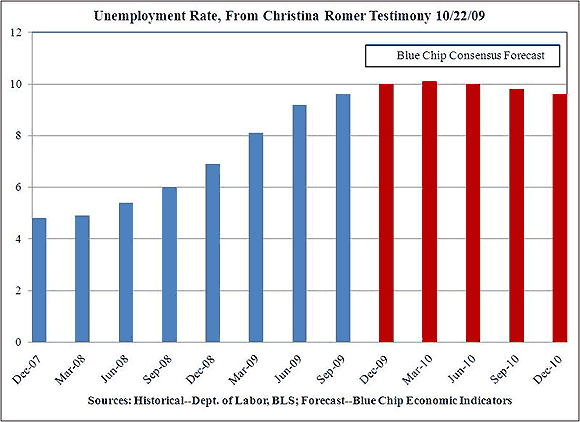

Before the October report, expectations were for a peak in Feb, at 10.2% – which we just hit. After, expectations have shifted out at least Mar. See the third chart. Of course, these are the same guys who thought it wouldn’t get worse than 9%, and advised Obama on those embarrassing projections with/without stimulus in the first chart.

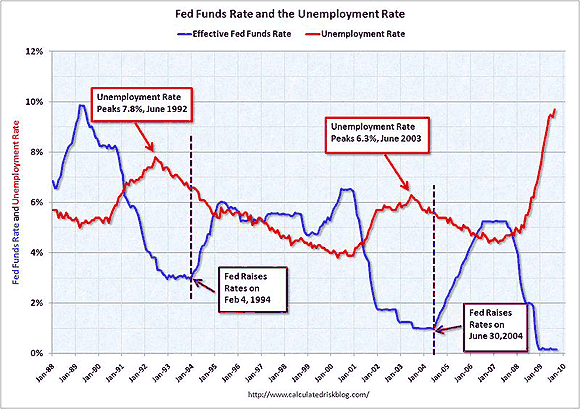

More relevant is that the Fed has much more pessimistic projections. And history says the Fed will wait a year or more after that peak to raise rates. See the second chart, from Calculated Risk. This puts us in a low rate environment for at least 18 months.

Before we get too gloomy, let me argue that this spike may be an artifact, not a trend.

These stats have scads of adjustments. The unemployment rate is unemployed-still-seeking over available-workforce. I have earlier noted the problems with the denominator in that it is adjusted by birth-death estimates that seem too light, making the workforce count larger. This doesn’t specifically affect the unemployment rate but does skew related labor reporting of the government (Mish explains here.) Also the reported rate of unemployed loses those who stop looking. (Not to make too much of a point of this, but about 1M workers will fall off unemployment at the end of this year.) The much higher U6 count (at 17.5%) captures them. So the reported rate has probably been too low.

This time the rate may have spiked too high. The prime seasonal adjustment on October is ramping up temp workers for the holiday sales season. Given all the retail outlets that have been closed, even with a reasonably strong Xmas, and hiring on a per-store basis, the overall number of temp workers would be much lower than expected due to fewer storefronts. In fact, prior to adjustment, unemployment held constant at 9.5%, and the number of jobs actually rose by 80K.

My conclusion is unemployment is worse than the official stats show (at least the most reported U3 rate), but the trend may not be not as bad as this report suggests. For purposes of estimating when the Fed begins to tighten, the trend is more important than the rate.

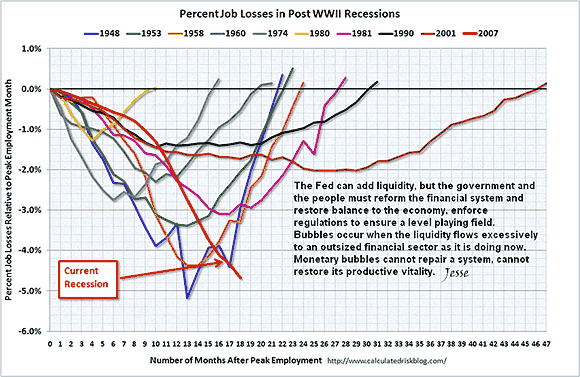

Right now we cannot tell if the trend is flattening. We can say the downward trend, when compared with all other post-war recessions, is making this the longest and soon the deepest fall since the Great Depression. Worse, the percent of long-term unemployed (15 weeks or more) at 5.7% is much higher than in prior post-war recessions. The NYT has a good chart showing this.

The spike up in October, however, has spooked a lot of commentators, and may be driving some poor policy decisions. Here are examples:

1. Bernanke was noticably downbeat in his remarks last week. He singled out “the labor situation” along with bank lending as the two worrisome factors.

2. Dallas Fed President Fisher commented that he thought Q3 GDP would be reduced from 3.5% to 2.5%. (We will find out tomorrow.) Bernanke believes that growth of 2.5% is too slow to bend the unemployment curve.

3. Keynesian economist Brad deLong now thinks there is a chance of falling into a Great Depression. He has pushed for a new stimulus, along with Krugman.

4. Speaker Pelosi claimed the Stimulus created or saved over a million jobs. This spurred investigations of her claims, and instead found 700 (!!) phantom districts, faux claims, and few jobs. Today even the left-leaning SF Chronicle reported Errors Riddle Accounts of Stimulus Spending. They had a hard time finding any jobs created or saved, but they did find the claims had created non-existent districts in California. Future virtual voters with virtual Congressmen?

5. Obama remarked how more deficit could throw us into a double-dip. This is so at odds with the advice he has been following from Krugman et al. it makes you pause to wonder what is up. Most likely he is maneuvering to push a jobs bill that largely retargets the remaining TARP funds and some of the unspent Porkulus Stimulus.

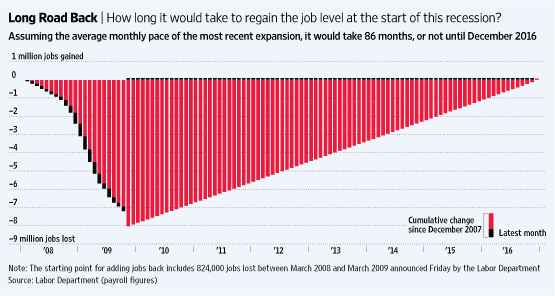

How to make sense of this? Mish has done a series of analysis on how bad this could get, and how long it could last. He started with this gloomy chart from a recent WSJ article, which shows how long it will be to get back the jobs lost already.

Mish went on to estimate peak unemployment across different scenarios. He took Bernanke’s recent remarks to heart, and created a Scenario B which has unemployment peaking about a year out then sliding. Mish’s conclusion:

“unemployment will still be above 10% at the end of 2014 and will not dip below 8% until the end of 2020.”

He isn’t the only gloomy one. Former Merrill Lynch analyst David Rosenberg, whom I think has done a great job assessing the economy, believes we get to 12% or higher, and will continue to creep up for at least a year after the recession ends. One of his key insights is that many of the jobs created post-2000 were credit bubble related, that is, not tied to any real increase in the productive side of our economy, but an illusion created by excess borrowing. They cannot come back until the economy catches up again to the ilusory level of the bubble. This will take a while.

One of my favorite economics bloggers, Edward Harrison at Credit Writedown, sees us in structural high unemployment: even if we are slowly recovering, the many unemployed will be left bereft of employment for a long time. And of course new workers are coming into the workforce all the time as well, compounding the problem.

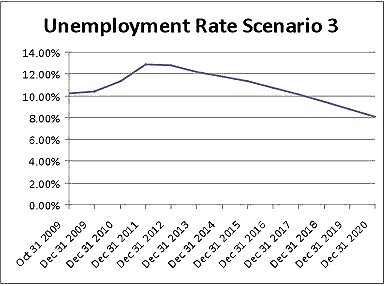

John Mauldin has been on this theme for a while. beginning with his New Normal article in Sept. He commented on Mish’s scenarios and Rosenberg’s analysis in If This Is a Recovery … He has become a believer in the double-dip scenario, Scenario 3 (see last chart), which puts unemployment over 13% and staying above 10% for eight years (!!). Gloomy indeed.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply