Last week I wrote a post about “government debt hysteria” that has gotten a lot of attention because of a link from Paul Krugman. (As Felix Salmon, said, “blogging is a lottery on the individual-blog-entry level.”) The main point of last week’s post was not that it’s wrong to be concerned about the national debt (I think everyone is concerned about it — the question is what to do about it and when), but that it’s irresponsible to title a column “Could America Go Broke?” and talk about hyperinflation without providing some evidence, or at least a logical argument that goes beyond tautology, that hyperinflation is something we should be worrying about it.

Here’s something else that’s irresponsible. In that same column, Robert Samuelson says, “The Congressional Budget Office reckons the Obama administration’s planned budgets would increase the debt-to-GDP ratio from 41 percent in 2008 to 82 percent in 2019″ (emphasis added).

Let’s take a look at that claim. I’m going to work with two versions of the CBO’s Budget and Economic Outlook, published in January 2008 (before we knew we were in a recession) and August 2009, and I’m going to use their baseline numbers, which show debt-to-GDP growing from 40.8% to 67.0% in 2018 and 67.8% in 2019. (I’m guessing Samuelson is citing the CBO’s additional analysis that assumes certain tax cuts will be extended; I’m not using that one because I can’t find the tables in sufficient detail.) I’m not contesting that debt-to-GDP will go up by a lot; I want to see why it’s going up. I’m also only going out through 2018 because the 2008 CBO report only went that far.

According to the 2008 report (Table 1-3), the budget from 2009 through 2018 shows an aggregate surplus of $0.3 trillion. The 2009 report (Table 1-2, PDF page 20) shows an aggregate deficit of $8.0 trillion, for a difference of $8.3 trillion.* Where does that come from?

In the 2008 report, discretionary outlays for 2009-18 are $12.4 trillion. In the 2009 report, that figure is now $13.7 trillion, for a difference of $1.3 trillion; that’s the most you can credibly blame on “the Obama administration’s planned budgets” — and even that includes the stimulus package from earlier this year, which was a response to a severe recession.

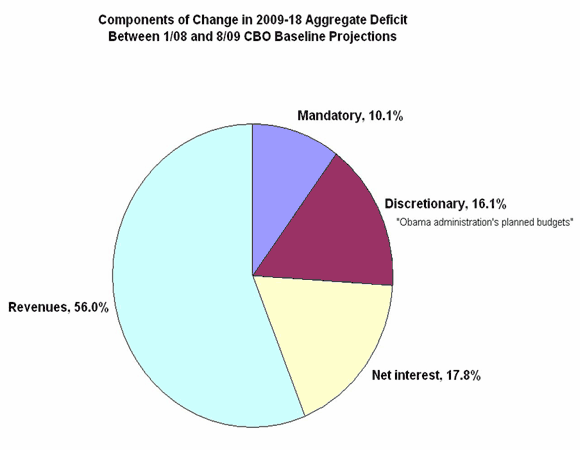

So where do the other $7.0 trillion come from? Increases in mandatory spending are $0.8 trillion. Increases in net interest payments are $1.5 trillion. But the big whopper is on the revenue side, where revenues are projected to be $4.6 trillion lower.** That is, you get a picture like this:

So far, of the $8.3 trillion change in our projected fiscal situation, 16.1% is due to discretionary spending. 56.0% is due to lower revenues caused by … the recession and the financial crisis.

But wait, that’s not all. The increase in the national debt would only be from 40.8% to 60.9% (not 67.0%) of GDP if 2018 GDP remained where it was projected in 2008. However, between the 2008 and 2009 CBO reports, projected 2018 GDP has fallen from $22.4 trillion to $20.3 trillion. That’s also due to the recession and the financial crisis. A smaller denominator means the same debt becomes a larger proportion of GDP.

In short, the problem is that the economy collapsed. Blaming our increasing debt problems on “the Obama administration’s planned budgets,” when they are responsible for one-sixth (or one-fifth, if you read footnotes) of part of the problem (the part not due to a shrinking denominator), is deeply misleading. It also leads to the wrong conclusion: cut spending.

What’s the right conclusion? Simon, my co-author, has been going around saying that the real cost of the financial crisis would be an increase in government debt of 40 percentage points of GDP. I’ve been telling him that I’m nervous about that number, because the long-term debt problem has always been with us, and it’s called Medicare. Well, it turns out Simon was right. The 2008 CBO report projected that by 2018, debt held by the public would be only 22.6% of GDP. The 2009 report projects 67.0%, for an increase of 44.4 percentage points. What happened between those reports? The financial crisis and a severe recession. And if we want to prevent that from happening again, we need to reform our financial system.

* Readers are likely to have noticed that $8.3 trillion is a lot more than 26% of GDP (even in 2018), yet the debt figure only goes up by 26 percentage points. The reason is that the CBO’s debt figure only counts debt held in public hands; the rest of the increase in the debt is absorbed by Social Security and other government accounts. My point here is only to show the proportional contributions to the increase in the debt.

** You could argue that the Obama budgets should be charged a portion of the change in net interest expense. Since discretionary spending is responsible for about 20% of the change other than net interest, it should be charged 3.6 percentage points of the change in net interest, bringing discretionary spending’s total contribution to 19.7% of the $8.3 trillion.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply