“And let’s be honest about it. Hybrid ARMs were never made based on the assumption that the borrowers would be able to make the payment once the loan reset. They were designed as two or three year ‘bullets’ … with the assumption that home appreciation would allow the borrower to refinance at, or before, reset. Given current conditions in the housing market, this business model is no longer viable, which should come as no shock to anyone.”

FDIC Chairwoman Sheila Bair, October 2007

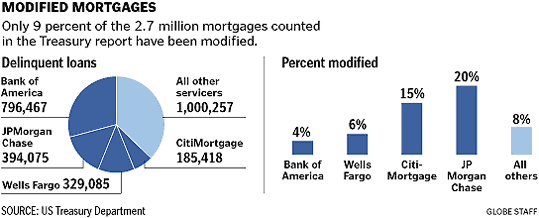

As a result, moving into 2010, a fresh round of mortgage losses should come as no shock to anyone either. I’ve noted that we are facing a predictable second wave of defaults, based on a mountain of scheduled resets for Alt-A and Option-ARM mortgages, which began in recent weeks and will continue through 2010 and 2011. One of the counter-arguments against such concerns is the assertion that “the majority of these mortgages have already been modified.” Unfortunately, this assertion is not true.

Moreover, the 2.7 million delinquent mortgages counted above were those that were already distressed early in the third quarter of this year. Moreover, many of these modifications are simply term extensions that reset the clock. A recent Fed study pointed out that only about 3% of delinquent mortgages have received modifications that would reduce their monthly payments in the first year. As noted a few weeks ago, “coupling state-by-state delinquency rates and foreclosure starts (as reported by the Mortgage Bankers Association) with other data, the Center for Responsible Lending [which correctly predicted, but slightly underestimated the size of the first wave of defaults] projects that for most states, foreclosure totals will more than triple over the coming 4 years, for a total of 8.1 million foreclosures.”

As for the small percentage of mortgages that receive modifications, the outlook is not very encouraging either. Several months ago, John Dugan, head of the U.S. Office of the Comptroller of the Currency, noted “over half of mortgage modifications seemed not to be working after six months.” Dugan reported that after three months, nearly 36 percent of borrowers who received restructured mortgages re-defaulted. The rate of re-default jumped to about 53 percent after six months and 58 percent after eight months.

Meanwhile, Bloomberg reported last week that “Citigroup (C) and J.P. Morgan Chase & Co. (JPM) are hoarding cash as if another crisis were on the way.” Notably, a week after CIT and Advanta filed for bankruptcy, Citigroup has sent letters raising the finance charge on some of its credit cards to 23.99% annually – even for creditworthy customers who pay their balances in full on a monthly basis. This is a bit of deja vu, given that Advanta did virtually the same thing in August of 2008, raising rates to 25% on its cards. This is not the type of development that encourages debt-financed economic activity (which has historically been the primary driver of early economic expansions).

Since June of this year, outstanding bank credit (loans and leases) has plunged at the steepest rate observed in the available post-war history, while at the same time, bank cash reserves have soared (Prieur du Plessis offers a good overview here). This surge in reserves is a mirror image of the Fed’s balance sheet, which has taken on over a trillion dollars in new assets – primarily mortgage backed securities. The problem here is that the underlying quality of agency paper continues to deteriorate, which means that Fannie Mae (FNM), Freddie Mac (FRE) and other agencies will likely sustain major additional losses – eventually footed by the public – because they accepted a negligible fee from mortgage lenders in return for slapping the government’s Good Housekeeping Seal of Approval on these garbage loans.

The Wall Street Journal reported last week that “Fannie Mae and Freddie Mac, already reeling in red ink, are warning they could face additional losses from the weakening condition of mortgage-insurance companies.” The trouble for the GSEs goes beyond deteriorating loan quality and their inability to recover insured losses – their huge “off balance sheet” portfolios have thus far been excused from proper loss reporting. As we learned last week from a little note in Freddie Mac’s most recent quarterly report, this is about to change (italics mine):

“In June 2009, the Financial Accounting Standards Board issued an amendment to the accounting standards for transfers of financial assets (SFAS 166) and an amendment to the accounting standards on consolidation of variable interest entities (SFAS 167). Both amendments are effective and will be applied prospectively by the company on January 1, 2010 … Under these accounting standards, the company will record the underlying mortgage loans in these single-family PC trusts and some of its Structured Transactions on its balance sheet. These mortgage loans have an outstanding unpaid principal balance of approximately $1.8 trillion as of September 30, 2009… While Freddie Mac continues to evaluate the impacts of adoption, the company expects that the adoption could have a significant negative impact on its net worth.”

The big picture is this. There is most probably a second wave of mortgage defaults in the immediate future as a result of Alt-A and Option-ARM resets. Yet our capacity to deal with these losses has already been strained by the first round that largely ended in March. The Federal Reserve has taken a massive amount of mortgage-backed securities onto a balance sheet that used to be restricted to Treasury securities. The purchase of these securities is reflected by a surge in cash reserves held by banks. Not only are the banks not lending these funds, they are contracting their loan portfolios rapidly. Ultimately, in order to unwind the Fed’s position in these securities, it will have to sell them back to the public and absorb those excess reserves, so to some extent, the banking system can count on losing the deposits created by the Fed’s actions, and can’t make long-term loans with these funds anyway.

Increasingly, the Fed has decided to forgo the idea of repurchase agreements (which require the seller to repurchase the security at a later date), and is instead making outright purchases of the debt of government sponsored enterprises (GSEs such as Fannie Mae and Freddie Mac). Again, the Fed used to purchase only Treasuries outright, but it is purchasing agency securities with the excuse that these securities are implicitly backed by the U.S. government.

This strikes me as a huge mistake, because it effectively impairs the Fed’s ability to get rid of the securities at the price it paid for them, should Congress change its approach toward the GSEs. It simultaneously complicates Congress’ ability to address the problem because Bernanke has tied the integrity of our monetary base to these assets. The policy of the Fed and Treasury amounts to little more than obligating the public to defend the bondholders of mismanaged financial companies, and to absorb losses that should have been borne by irresponsible lenders. From my perspective, this is nothing short of an unconstitutional abuse of power, as the actions of the Fed (not to mention some of Geithner’s actions at the Treasury) ultimately have the effect of diverting public funds to reimburse private losses, even though spending is the specifically enumerated power of the Congress alone.

Needless to say, I emphatically support recent Congressional proposals to vastly rein in the power (both statutory and newly usurped) of the Federal Reserve. Starting with the Bear Stearns deal, the Fed under Ben Bernanke has made a sharp and distinct departure from its historical role, in violation of its charter. As I noted when the bondholders of Bear Stearns were rescued, “The troubling aspect of the Fed’s action was not that it lent to a non-bank entity. That ability is clearly authorized by Section 13(3) of the Federal Reserve Act. The problem is that it made its “loans” as “non-recourse” funding – meaning that it would not stand to be repaid if the collateral itself was to fail.” This is still what the Fed seems determined to accomplish.

In my view, deeper loan losses are ahead, and if we deal with the next round the same way that we dealt with the last, we will ultimately succeed in debasing the U.S. dollar. There’s little inflationary pressure at present, and chances are that fresh credit concerns will create enough demand for government liabilities to forestall inflationary pressures for several years more. But we cannot reimburse the losses of irresponsible lenders with trillions freshly issued government liabilities without those liabilities ultimately eroding in value. The probable real, after inflation return on stocks and bonds over the coming decade is likely to be very unsatisfactory.

Market Climate

As of last week, the Market Climate for stocks was characterized by unfavorable valuations and mixed market action. Based on our standard methodology (which somewhat assumes that S&P 500 earnings will maintain their historical peak-to-peak growth path, with no sustained impact from the recent downturn) the S&P 500 is currently priced to deliver nominal total returns averaging about 6.1% annually over the coming decade.

Even with the optimistic earnings assumption, this is a rate of return that has historically been associated with major market peaks, including 1987, and one that has never been followed by durable market returns. On the bright side, the prospective total return on stocks was even lower during much of the late 1990’s market bubble, and stocks were certainly able to mount temporary gains well in excess of 6.1% annually while the bubble lasted. On the negative side, those returns were ultimately met by massive losses. Indeed, even including the recent market advance, the S&P 500 has achieved an average annual total return of just 6.1% in the 14 years since 1995. Returns are significantly lower when measured from later dates in the 1990’s.

That said, the “two data sets” issue is still with us. If we assume that the recent downturn was a standard, run-of-the-mill post-war recession, then at points where stocks are not strenuously overbought, it may be reasonable to accept some amount of market exposure (despite strained valuations) based on various trend-following components of market action. On the other hand, a strong defense is warranted if we allow for the likelihood that market conditions are better characterized by “post crash” dynamics (where prices are vulnerable to abrupt reversals, and the ultimate adjustment period for the market and the economy is more extended). I don’t believe that we can rule out the “post-crash” data set, because it is a strong match to what we observe – particularly in light of continuing employment and mortgage debt concerns.

In practice, we have moved incrementally toward a convex combination of these possibilities – accepting a modest amount of exposure on selloffs (provided that we don’t observe too many internal breakdowns), and clipping our exposure on overbought conditions. I believe that this strikes a reasonable balance between the two possible states of the world.

In bonds, the Market Climate last week was characterized by modestly unfavorable yield levels and moderately favorable yield pressures. Last week, we observed a spike in the prices of Treasury Inflation Protected Securities, reflecting a move to negative real yields on many of these issues.

While I do expect that we will observe longer-term inflation problems beginning several years out, the problem with negative real yields on TIPS is that in the event that inflation does not present itself near-term, TIPS holders are forced to accept negative current returns as the price of longer-term inflation protection.

Generally speaking, market participants do not sit with this sort of “negative carry” trade for very long once price momentum eases. For that reason, we shifted a significant portion of assets in Strategic Total Return out of TIPS and into medium-term nominal Treasury securities last week. The overall duration of the Fund continues to be moderate, at just over 3 years. We also exited our foreign currency holdings last week on strength. The Fund continues to hold about 1% of assets in precious metals shares, and about 4% of assets in utility shares.

Hussman Funds Disclosure.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply