A quick chart-of-the-day post motivated by some articles I was reading today about differences in country performances during the global financial crisis. Which economic policies worked best? How bad (or good) membership in the Euro area was to fight back the crisis? These are important questions to understand the effectiveness of different economic policies (monetary, fiscal, exchange rate).

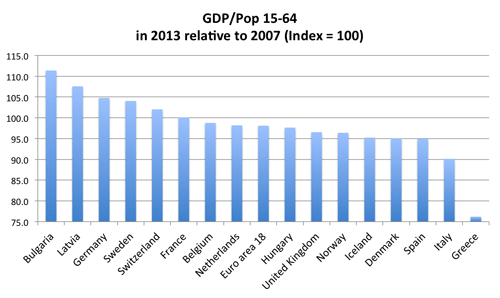

When comparing performance across countries it is quite common to use a variety of indicators: GDP growth, unemployment, productivity,… They all tend to move together but they can sometimes provide a quite different view of the economic performance during a number of years. I decided to look at GDP growth but adjusting is by changes in demographics: GDP divided by working-age population (between 15 and 64 years old, as it is measured by the OECD). What I do is to compare the 2013 number with the 2007 number (which I use as the beginning of the crisis).

What I find interesting (and surprising) is the similarities across countries, despite the differences in policies. With the exception of Greece (and possibly Italy) all the other countries are very close to each other. The three countries that originally opted out of the Euro do not look too different from the Euro countries. Yes, Sweden has done great but so has Germany. The UK has grown less than the Euro area (of 18 countries), less than France or the Netherlands and at a rate which is very similar to that of Spain. Same for Denmark. Among the small countries that are still outside of the Euro area some have done quite well, others not so well and, surprisingly, some of these countries manage to do well with a currency pegged to the Euro (Bulgaria and Latvia).

[Note on data: let me stress that I am using GDP divided by working-age population and this makes a difference for some economies. For example, Latvia’s GDP in 2013 is still lower than in 2007 but its working-age population has been declining sharply over these years. Dividing by working-age population allows us to remove potential demographic changes during these years.]So despite the stubbornness of the ECB and the constraints of a common currency, economic performance in the Euro area has not been too different from those of the other European countries that are outside. This might not really be good news. It might simply be the case that the anti-inflation obsession of the Swedish central bank and the fiscal policy austerity of the UK government have helped to make the Euro-area performance look not too bad.