This caught my eye :

There is plenty of temptation to crack open the champagne and celebrate the U.K.’s return to economic health, with even cautious Chancellor of the Exchequer George Osborne declaring victory was his.

Yet there are still several important reasons to be cautious about a series of better-than-expected economic indicators.

(Read more: U.K.’s economic recovery )

One of the most concerning is the prospect of another house price bubble forming. Interest rates have remained at a historic low for four and a half years, and the government has introduced measures like the Help to Buy scheme, where it guarantees mortgages for first-time buyers with relatively small deposits.

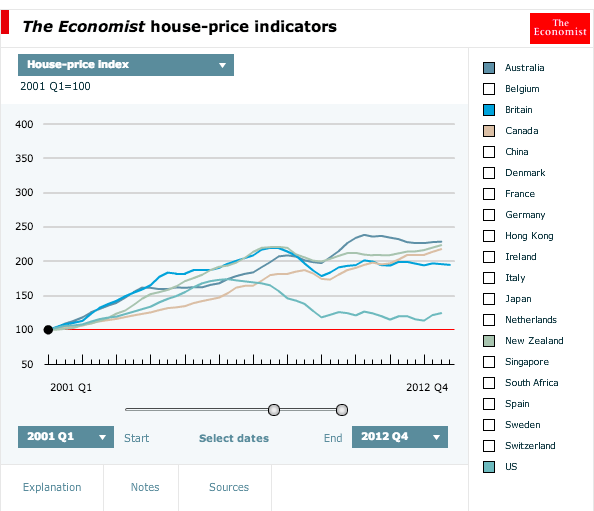

I wonder what they mean by “another house price bubble?” If it had been a US newspaper, I would have understood the comment. Many think the US had a housing bubble in 2006, although I don’t agree. But Britain? Here are house prices in 5 English speaking economies:

As you can see, the US pattern does look like a bubble, but the other four countries all show steep increases (in Britain’s case even steeper than the US), but then a leveling off, as if markets correctly saw that there were good fundamental reasons for house prices to soar in the early 2000s.

When the US index peaked at around 175 in 2006, the UK index was at around 195. It still is, even as the US index dropped back to 120. Yes, there was a small decline in UK prices during the steep 2009 recession, but what would you expect a rational, non-bubblicious market to do in the face of such an economic disaster?

So back in 2006 pundits in 5 English speaking countries cried “Bubble!!!” In 4 out of 5 of the countries they were wrong. But in 5 out of 5 cases they insist they were right, as we see from self-congratulatory advertisements in The Economist.

Unless one wants to argue that any small decline in a highly volatile asset market that had previously risen sharply is a “bubble,” there is obviously no evidence of bubbles in the four non-US cases shown above. And if you do insist that any decline in a highly volatile asset market that had previously risen is prima facie evidence of bubbles, . . . well, then I hardly know what to say.

PS. Here’s an article describing how the Chinese are snapping up a lot of properties in Sydney. Aussie labor is employed building houses. The houses are traded for Chinese goods. The only special feature is that the houses don’t physically leave Australia. Chalk up one more reason why current account deficits are an utterly meaningless number.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply