The Social Security Trust Fund has come out with its annual report. Some have looked at it and concluded that the relatively stable conditions at SS the past year is evidence that all is well. There are many headlines like this these:

I don’t see all the “good news” that folks are writing about. A few examples:

– The 75 year unfunded liability grew to $9.6Tn, from to $8.6Tn a year ago.

– The unfunded liability for the infinite future grew $2.6Tn (+12.6%), to $23.1Tn.

What do these numbers mean? They are large and growing quickly. The calculation is based on the NPV of future liabilities, meaning that these are the numbers to consider today if one wanted to “fix” SS. These present values are an indication of what future generations will have to fork out to support the promises that have been made. As it’s impossible for the USA to write itself a check for these big amounts, the conclusion has to be that at some point in the future, benefits have to be cut, or major tax increases have to be enacted.

– The SSTF calculates that in order to bring SS into balance some combination of benefit cuts or tax increases is required. To address the imbalances that exist one of two things must happen IMMEDIATELY:

- Payroll taxes must go up by 2.66%, or

- Benefits must be cut by 16.5%.

Either of these outcomes (or some combo that equals the same thing) would have a devastating and lasting consequence on the real economy. I see no support today for benefit cuts of this magnitude (or large tax increases), so this problem will have to fester for a few more years before action is taken. Every year that brings us no action will result in higher and higher costs to “fix” the problem.

– The Trustees added a new type of “fix” that should scare the crap out of anyone who is close to retirement age. The solution would be keep benefits as they are today for those who are already getting SS checks, and to reduce them for anyone who reaches retirement after 2013. This would mean that all future beneficiaries would see a cut in their scheduled benefits of 20%. There are 60Mn seniors (and those on disability) who now get checks; and they all vote. The idea that new beneficiaries take this big hit is politically viable. This potential outcome will force more and more people into getting their benefits early in an effort to avoid the proposed cuts.

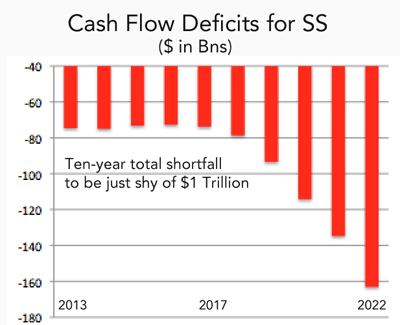

– The following chart tracks the cash flow deficit at SS based on the intermediate (Base Case) analysis. Over the coming decade the cash shortfall is projected to be $950Bn. Every penny of this shortfall must be financed with additional Debt Held By The Public.

– Interest income was revised lower by a lumpy $111Bn over the next decade. SS has woken up to the fact that the Fed has taken actions that will permanently reduced income at SS. I believe that the $111Bn downward adjustment is still understating the consequences of the Fed’s actions.

– The 2021 TF balance is now anticipated to be $2.9Tn. That’s $145Bn less than the expectation of $3.05Tn a year ago. I’m willing to wager that even these results will not be met.

– The TF report relies on a set of economic assumptions to achieve the results that were presented. A few of the key variables:

– There will be no recessions at all over the next decade. In fact, the TF assumes there will no economic downturns between now and 2090. Rubbish!

– Real GDP will be increasing rapidly for the next few years. These are the plug numbers estimates for Real GDP:

- 2013 – 2.2%

- 2014 – 3.4%

- 2015 – 4.0% – Not happening…

- 2016 – 3.8% – Not happening…

- 2017 – 3.4%

- 2018 – 3.0%

- 2019 – 2.6%

- 2020 – 2.3%

- 2021 – 2.2%

- 2022 – 2.1%

– The SSTF assumes that a rapidly rising economy will force a significant increase in interest rates. As SS is a saver, interest income is a big component of it’s total revenue, so high interest rates are essential to keep SS afloat. I don’t think these expectations for ten-year yields have a chance of being realized (if rates get this high, then we’re in for a hell of a recession).

10-Year Interest Rates

- 2013 – 1.2%

- 2014 – 2.4%

- 2015 – 4.6% – Not happening…

- 2016 – 5.6% – Not happening…

- 2017 – 6.2% – Not happening…

- 2018 -2021 – 6.5%% – Not happening…But if it does, there will have to be a recession. The TF forecast is at odds with itself.

– The TF report relies on an optimistic assumption regarding unemployment. In just a few years we will be back to the ‘good old days’ of 5.5% unemployment. We will not see these results:

- 2014 – 7.8%

- 2015 – 7.2%

- 2016 – 6.6%

- 2017 – 6.1%

- 2018 – 5.8%

- 2019 – 5.6%

- 2020 – 2090 – 5.5% Seventy years of perfection??? Using these numbers insures that the SSTF “looks” solvent long-term. But the reality is that this result will not be realized.

A year from now the 2014 SSTF Report will be released. There will be another big downward adjustment in future interest income. I believe those revisions will total at least $60Bn. This will result in the TF reaching its highest balance ($2.85Tn) in 2016. This is a critical milestone for SS, it will come 5-years earlier and $75Bn shy of the data that SS presented in its 2013 report.

So don’t believe those Press headlines that paint a rosy picture for SS. There’s no good news in this report card.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply