Sometimes simple, direct points are the most powerful. For me, the simplest and most direct points in Chairman Bernanke’s Senate testimony this week were contained in the following one minute and 48 seconds of video (courtesy of Bloomberg):

At about the 1:26 mark, the Chairman says:

So, our accommodative monetary policy has not really traded off one of [the FOMC’s mandated goals] against the other, and it has supported both real growth and employment and kept inflation close to our target.

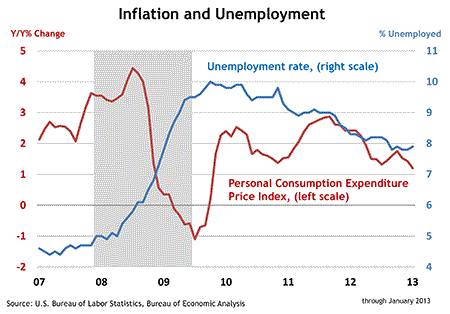

To that point, here is a straightforward picture:

I concede that past results are no guarantee of future performance. And in his testimony, the Chairman was very clear that prudence dictates vigilance with respect to potential unintended consequences:

Highly accommodative monetary policy also has several potential costs and risks, which the committee is monitoring closely. For example, if further expansion of the Federal Reserve’s balance sheet were to undermine public confidence in our ability to exit smoothly from our accommodative policies at the appropriate time, inflation expectations could rise, putting the FOMC’s price stability objective at risk…

Another potential cost that the committee takes very seriously is the possibility that very low interest rates, if maintained for a considerable time, could impair financial stability. For example, portfolio managers dissatisfied with low returns may reach for yield by taking on more credit risk, duration risk, or leverage.

Concerns about such developments are fair and, as Mr. Bernanke makes clear, shared by the FOMC. Furthermore, the language around the Fed’s ultimate decision to end or alter the pace of its current open-ended asset-purchase program is explicitly cast in terms of an ongoing cost-benefit analysis. But anyone who wants to convince me that monetary policy actions have been contrary to our dual mandate is going to have to explain to me why that conclusion isn’t contradicted by the chart above.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply